OTP Morning Brief: Winds blowing from the Strait of Hormuz shaped the sentiment on developed stock and bond markets

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

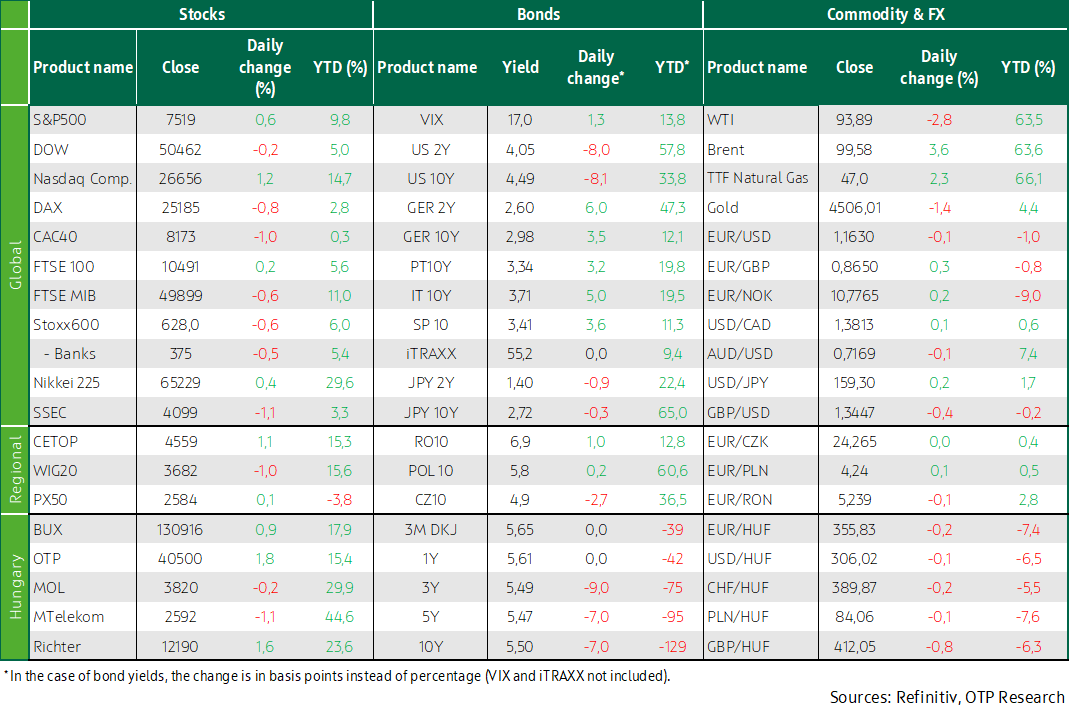

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The Islamic Revolutionary Guard Corps threatened to retaliate after the US carried out what it described as “self-defense strikes” on Iranian missile launch sites and boats around the Strait of Hormuz. Tuesday's session was dominated by a negative sentiment on the leading European stock markets, as all major indices fell except the FTSE100. In the CEE region, the BUX was the best performer, while the Hungarian blue-chips closed mixed. The S&P and NASDAQ closed at new highs, as a favorable earnings season and optimism surrounding AI offset concerns over the unresolved conflict in the Middle East. Brent oil rose by more than 3%. Long-term yields rose inEurope and fell overseas. In line with expectations, the MNB Monetary Councilleft the key interest rate unchanged at its yesterday's meeting. Hungary'slong-term yields fell. News of the Middle East conflict could move marketsagain today. Donald Trump is holding a cabinet meeting at the White House today.

Trading on Tuesday unfolded in a negative mood across major European stock exchanges, while the BUX rose

Major European stock markets mostly closed Tuesday in negative territory, overshadowed by the still unproductive US–Iran talks. The Islamic Revolutionary Guard Corps threatened retaliation after the United States carried out what it described as “self-defense strikes” against Iranian missile launch sites and vessels near the Strait of Hormuz—actions the Iranian foreign ministry said demonstrate the US administration’s “malice and hypocrisy” toward Iran. Meanwhile, intense fighting continues between Israel and Lebanon, the other two key parties to the conflict, with Israel pushing ever deeper into Lebanese territory. Alongside concerns over global oil supply, expectations of European rate hikes were further reinforced by ECB Governing Council member Isabel Schnabel, who stated that the central bank should raise rates in June even if an Iranian peace agreement is reached.

The Stoxx 600 fell by 0.6% after hopes tied to a potential peace had previously driven the pan-European index close to record highs. Apart from the slightly higher UK FTSE 100, major European indices moved lower. Among largely declining sectors, carmakers underperformed, as Ferrari’s 8.4% drop dragged the sector; investors reacted negatively to the unveiling of the company’s first fully electric model. It is also worth noting BP’s 4% decline after the firm dismissed its chairman with immediate effect.

Among CEE markets, the BUX delivered the strongest performance, rising by 0.9%. Hungary’s blue chips closed mixed, with OTP and Richter managing to post gains.

The decline in European natural gas prices seen last week extended into Monday, but Tuesday’s pessimistic trading brought a rise, with prices climbing by more than 2% to 47 EUR/MWh.

The S&P 500 and the NASDAQ closed at new highs; semiconductor manufacturers performed strongly, while Brent crude prices rose

The S&P 500 and the NASDAQ closed at new record highs on Tuesday, the first trading session after the long weekend, as optimism around artificial intelligence, a strong earnings season, and robust profit outlooks offset concerns related to the Middle East conflict. Gains were led by semiconductor manufacturers, with Micron standing out as it soared 19%, lifting its market capitalization above $1 trillion for the first time after UBS raised its price target from $535 to $1,625. Aerospace stocks also performed well after Elon Musk-owned SpaceX announced last week its planned IPO, which could take place as early as June. Qualcomm shares rose 4.5% following a Bloomberg report that the company had reached an agreement with TikTok owner ByteDance to supply chips, while the Philadelphia Semiconductor Index climbed 5.5% to an all-time high.

Brent crude rose by more than 3%, returning close to the $100 per barrel mark as recent optimism about Middle East peace faded. In contrast, WTI declined by nearly 3% compared to last Friday’s level.

Long-term yields declined in the US while risingin Europe; in line with expectations, the MNB’s Monetary Council left thepolicy rate unchanged at yesterday’s meeting; domestic long-term yields fell

The 10-year US Treasury yield declined from last week’s near one-and-a-half-year peak of around 4.7% to below 4.5% by yesterday. In Europe, despite some rise, yields remained well below earlier highs, with the 10-year German Bund yield holding below 3%. The dollar retained its strength, with EUR/USD closing just above 1.16.

There was no meaningful movement in CEE region currencies, with the forint remaining below 356 against the euro. Domestic benchmark yields declined by close to 10 basis points to around 5.5%. At its policy meeting yesterday, the MNB’s Monetary Council left the base rate unchanged at 6.25%, in line with expectations. At the same time, the tone of both the statement and the press conference was more dovish than previously, suggesting that low CPI, a declining country risk premium, and a strong forint have increased the central bank’s room to cut rates. As a result, government bond yields dropped by a further nearly 10 basis points during the press conference. Demand was subdued at the three-month T-bill auction, where the announced HUF 30 billion was sold at an average yield of 5.68%.

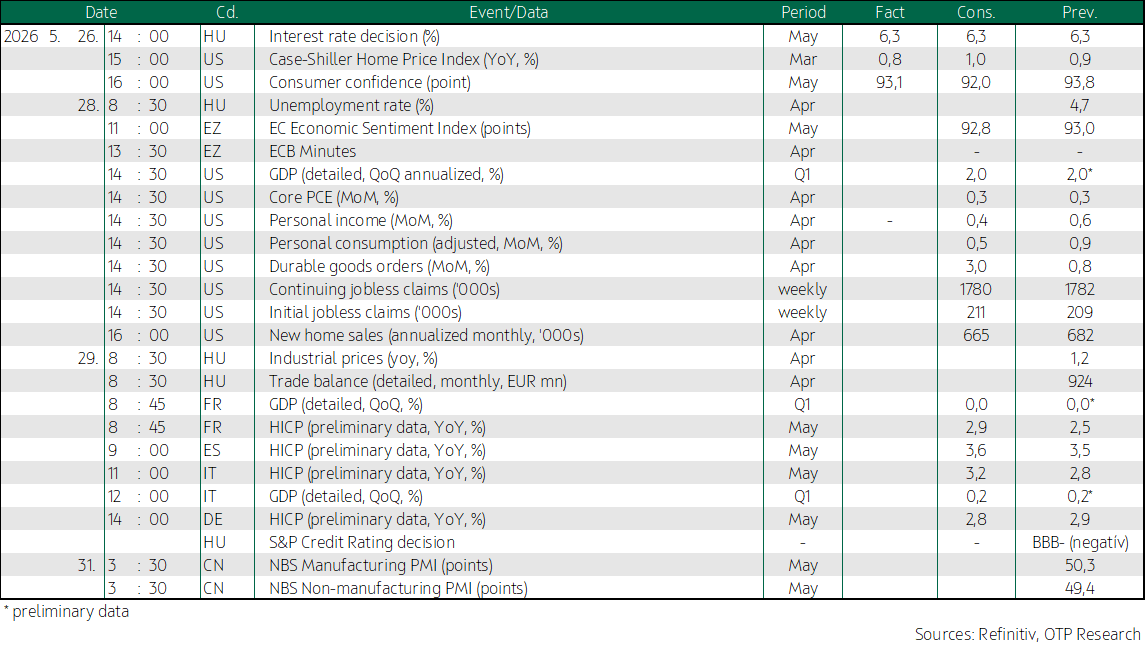

Today's highlights

Mixed movements were seen this morning across Asia-Pacific stock markets, as investors weighed news related to the Middle East conflict that had driven European and Wall Street trading the previous day. South Korea’s KOSPI and Japan’s Nikkei 225 climbed to new highs, while the Hang Seng and the Shanghai Composite remained in negative territory heading into the close.

Futures point to a mixed opening in Europe, while indicating a positive start in the US.

News related to the Middle East conflict may continue to drive markets today. The US and Iran are currently working on a declaration of intent, but disagreements over wording related to Iran’s nuclear program and sanctions have stalled progress toward a memorandum of understanding. According to US Secretary of State Marco Rubio, drafting the agreement could still take several days. Iranian state media has described the ongoing talks in Qatar as broadly positive. Meanwhile, Donald Trump is holding a cabinet meeting at the White House today.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more