OTP Morning Brief: Significant uncertainty lingers around the imminent end of the war against Iran and the reopening of the Strait of Hormuz

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

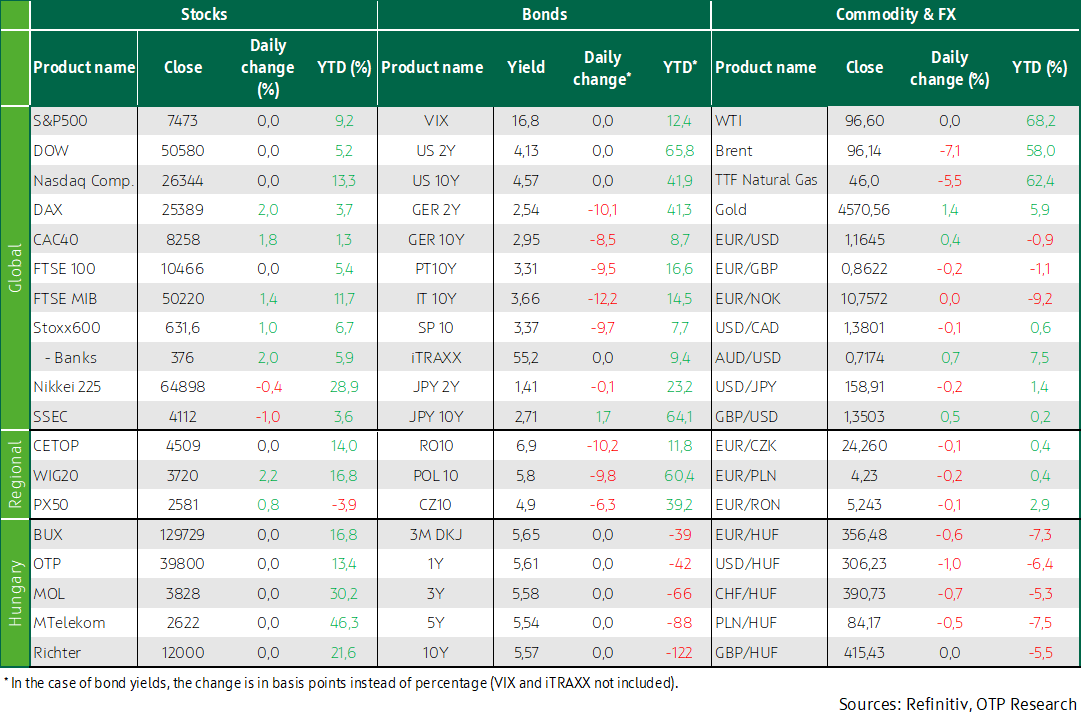

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Over the long weekend, optimistic expectations surrounding an imminent US–Iran agreement further strengthened, but these were tempered by US Secretary of State Marco Rubio’s statement today, indicating that finalizing the deal could take several more days, thereby dampening hopes for a near-term reopening of the Strait of Hormuz. Crude oil prices regained strength on Tuesday morning after Brent fell by 7% on Monday, while the two most closely watched oil benchmarks declined by 5–8% over the past week. On Monday, stock exchanges in Budapest, London, and New York were closed due to a public holiday, while European equity indices continued their gradual upward move, approaching their previous highs. Last week, the S&P 500 closed in positive territory for the eighth consecutive week, while the Dow finished at a new all-time high on Friday. Long-term bond yields in developed markets have turned lower from their previous multi-year highs, while the dollar weakened on Monday following a modest strengthening last week, with EUR/USD closing above 1.164. CEE currencies mostly strengthened over the past week, with EUR/HUF falling below 356.5 on Monday. Today, attention will be on the MNB’s rate decision, with the benchmark rate expected to remain at 6.25%. Later this week, core PCE Price Index from the US (Thursday) and fresh CPIs from the euro area (Friday) are this week's highlights.

Following an eventful week, European equity markets closed the past week with notable gains. The upward momentum continued on Monday, driven by optimistic expectations surrounding a US–Iran agreement, with both the Stoxx 600 and the DAX finishing near their record highs

The week started with gains in Western European equity markets, with the Stoxx 600 Europe closing 1% higher on Monday, reaching a near three-month high and recouping losses since the onset of the war against Iran; the pan-European index is now less than 0.5% below its all-time high recorded at the end of February, as investors remain highly optimistic about a potential agreement between the US and Iran and the reopening of the Strait of Hormuz. Investor sentiment was supported by US President Donald Trump’s statement on Saturday that a framework agreement on reopening the Strait of Hormuz has "largely been worked out," while Iranian officials were engaged in talks with Qatar’s prime minister over a possible deal. The DAX also closed near record levels after rising 2%, the CAC 40 advanced by 1.8%, and the IBEX 35 jumped 2.2%, while the London Stock Exchange and US markets were closed on Monday due to a public holiday, resulting in lighter-than-usual trading volumes.

In addition to optimism surrounding a resolution to the Middle Eastern conflict, enthusiasm for artificial intelligence companies also provided momentum to European stock markets on Monday: chipmaker ASML closed 1.5% higher, while AI equipment producer Schneider Electric jumped by more than 3%. Banks performed well, and airlines also rallied thanks to an roughly 5% decline in oil prices, with Lufthansa rising 3% and Air France-KLM soaring 6%. Most sector indices within the Stoxx 600 ended in positive territory, while the energy and telecommunications sectors posted slight declines.

Similar factors drove equity markets last week, with momentum supported by AI investment and hopes for a US–Iran agreement, although valuation concerns stemming from elevated yield levels constrained the advance, while volatile oil prices also weighed on markets, at times triggering multiple directional shifts. On a weekly basis, Western European equity markets posted broad-based gains: the Stoxx 600 Europe index rose 3%, the DAX climbed nearly 4%, and the FTSE 100 advanced 2.7%, supported by improving risk appetite. Easing tensions between the US and Iran and declining oil prices helped cyclical and rate-sensitive sectors recover from earlier weakness, even as bond markets remained cautious. In terms of sector performance within the Stoxx 600, technology, retail, travel and leisure, and telecommunications recorded the strongest gains during the week, while the energy sector and automakers saw more modest advances, with all sector indices of the pan-European benchmark closing the week in positive territory.

In parallel with last week’s decline in oil prices, European natural gas prices also trended lower, with futures falling by around 2% on Friday and by 3–4% over the course of the week; the downward move continued on Monday, as the one-month futures contract dropped 5.5% to below EUR 46/MWh.

In the CEE region, the BUX, which was closed on Monday due to a public holiday, missed out on the European upswing, while the WIG20 rose by more than 2% and the PX climbed 0.8%. Over the past week, regional equity markets—excluding the BUX—also delivered solid performance, with the Polish benchmark gaining 2.7% and the Czech index rising 1%. The BUX, however, fell by 1.8% over the week. Among domestic blue chips, only Magyar Telekom closed in positive territory (+4.5%), in line with the strengthening telecommunications sector across Europe. MOL posted significant day-by-day declines, tracking the slide in oil prices, which was exacerbated by Friday’s explosion at its Olefin-1 plant in Tiszaújváros, raising concerns about domestic plastic feedstock supply.

In a statement released late Friday, Moody’s announced that it had affirmed Hungary’s sovereign rating at Baa2, while maintaining a negative outlook.

The S&P 500 closed Friday in positive territory for the eighth consecutive week, with the technology sector remaining in focus

US markets were closed on Monday due to a public holiday, but the past week also developed favorably in the US. The S&P 500 and the Nasdaq Composite fluctuated near record levels, while the Dow closed at an all-time high on Friday, as equity markets were marked by notable volatility during the week amid oil price swings and geopolitical developments. The S&P 500 posted a 0.9% weekly gain, marking its eighth consecutive week in positive territory, while the Nasdaq rose 0.5% and the Dow advanced 2.1% over the same period. The Nasdaq delivered strong performance at the beginning of the week, supported by the continued rise of the AI-driven technology sector, although higher long-term yields capped broader gains. Corporate developments also remained in focus as the earnings season neared its end: Nvidia reported strong results and a favorable outlook, reinforcing elevated expectations related to AI, while Walmart disappointed with its guidance, putting pressure on the retail sector; results among consumer-focused companies were otherwise mixed, with TJX outperforming expectations, while Target and Lowe’s posted weaker figures. Among S&P 500 sectors, real estate, healthcare and utilities led the gains, while telecommunications, consumer staples and energy ended the week in negative territory.

On Friday, chipmakers returned to the spotlight, with the Philadelphia Semiconductor Index rising 2%, driven primarily by Qualcomm’s 12% surge, while Nvidia slipped 1.9%. Computer manufacturers also performed well after China’s Lenovo reported stronger-than-expected quarterly revenue growth of 27%; as a result, Dell’s share price skyrocketed by 17% to a record high, while HP rallied 15%. Cosmetics producer Estée Lauder jumped 12% after ending acquisition talks with Spanish perfume maker Puig.

Crude oil prices edged slightly higher into the close on Friday, but over the past week WTI fell 8% and Brent declined by more than 5% amid expectations of a favorable turn in geopolitical developments.

Eurozone bond yields fell sharply on Monday, following last week’s significant decline in both European and US yields. EUR/HUF closed below 356.5 on Monday after a notable strengthening over the previous week

Markets in developed economies continued to be driven by developments related to the war against Iran and news surrounding the Strait of Hormuz. At the start of the week, tensions escalated further, bringing the risk of global oil shortages closer and pushing sovereign bond yields of major currencies to multi-year or even multi-decade highs. However, by the end of last week and into yesterday, more favorable news emerged, as the US announced that a deal with Iran had largely been negotiated; oil prices dropped sharply, expectations for further rate hikes eased, and bond markets corrected. At the beginning of last week, oil prices were still trading near the upper end of the range established since the outbreak of the conflict with Iran, with Brent above USD 110 per barrel, but by Friday evening it had fallen to around USD 104 and dropped further to USD 94 yesterday. Macroeconomic data once again had a limited impact on markets, with PMI figures remaining strong in the US but coming in weaker than expected in Europe, while euro area wage data showed a gradual slowdown to a pace consistent with the inflation target (CPI). In the US, the rate expected by year-end has moved back to the current 3.5–3.75% target range instead of the previously priced-in hike. The 10-year US Treasury yield corrected from a one-and-a-half-year high near 4.7%, falling to 4.55% by Friday and below 4.5% yesterday. In Europe, markets are now pricing in only 2–3 rate hikes from the ECB instead of 3–4, while the 10-year German yield reversed from a one-and-a-half-decade high of 3.2% and fell back below both the upper end of the post-pandemic trading range and the psychologically important 3% level by yesterday. The dollar strengthened to around 1.16 against the euro by mid-last week, supported by high oil prices and rising risk aversion, but trading on Friday and yesterday brought a correction to around the 1.165 level.

Regional currencies regained strength from the second half of last week, with the Hungarian forint outperforming, appreciating from around 363 against the euro midweek to 356 by yesterday. Regional bond yields also declined, while domestic yields continued to fluctuate around 5.5%, near a two-and-a-half-year low, with the 10-year reference yield falling below 5.6% again on Friday, still not reflecting the impact of improving global sentiment related to the Strait of Hormuz.

Today's highlights

Asian equity indices are mostly trading in negative territory this morning, although the South Korean market remains an exception, posting gains of over 3%. Crude oil prices have started to rise again on Tuesday (around +1%) after the US carried out what Washington described as defensive strikes in southern Iran on Monday, while US Secretary of State Marco Rubio stated on Tuesday that finalizing an agreement with Iran could take “several more days,” thereby damping hopes for a near-term resolution of the conflict.

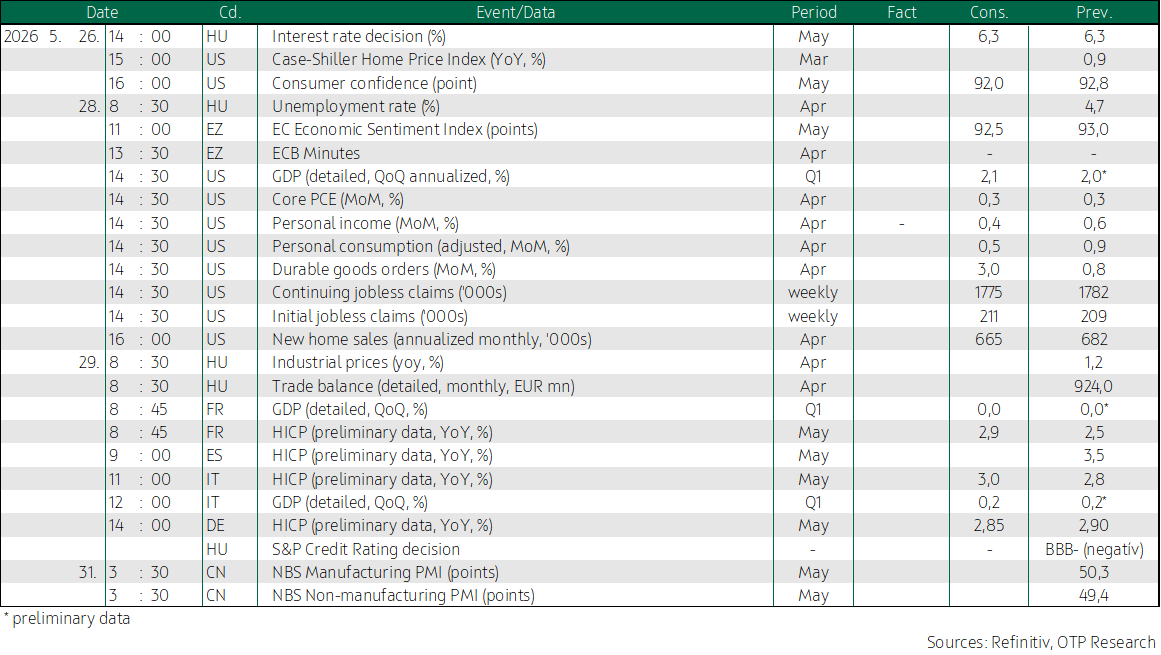

The MNB will hold a rate-setting meeting today, where the base rate is expected to remain unchanged at 6.25%; however, the central bank’s press conference will be worth close attention, as policymakers are likely to provide further insight into how they assess the impact of elevated oil prices and the strong forint on inflation (CPI) prospects, as well as the increasingly firm expectations for rate cuts.

Today, the Case-Shiller house price index and the consumer confidence index will be released in the US.

This week, inflation data will be in focus on the global stage alongside developments related to a potential US–Iran agreement. On Thursday, the core PCE figure for April—currently the Fed’s preferred inflation gauge—will be released, having shown a month-on-month pace exceeding more than twice the level consistent with the 2% annual target every month since last December. In the euro area, flash estimates for May CPI from the major economies, due on Friday, will take center stage, providing a fairly accurate preview of the aggregate inflation data to be published the following week.

Today, the Government Debt Management Agency (ÁKK) will offer three-month treasury bills worth HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more