OTP Morning Brief: Investors hoped for a diplomatic solution to the war in Iran

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

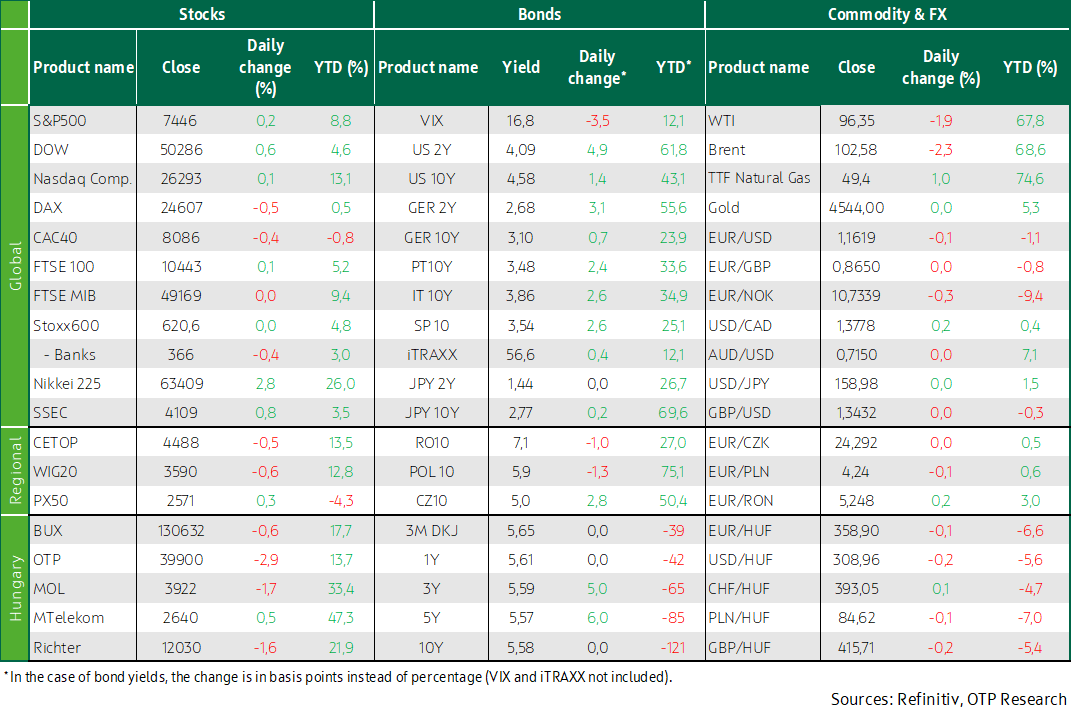

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

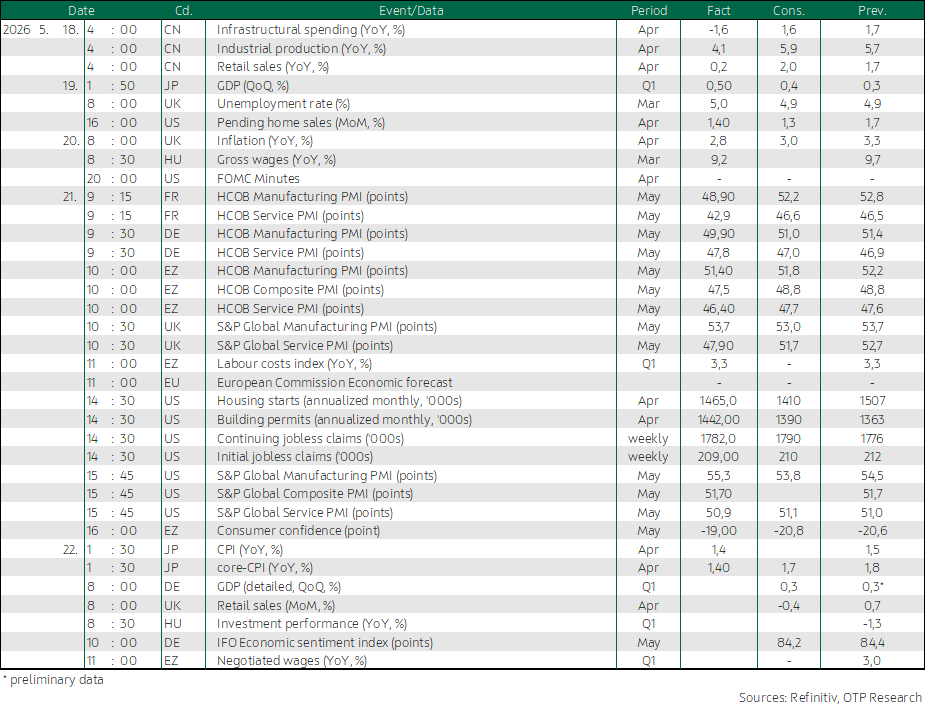

Western European indices closed mixed, while uncertainty surrounding the resolution of the Iranian conflict persisted; purchasing managers’ indices released yesterday painted a mixed picture of the European economy; in its spring forecast, the European Commission downgraded both this year’s and next year’s growth outlook for the EU, while consumer confidence improved slightly; overseas indices moved higher; oil prices declined by the end of the session; Nvidia’s earnings exceeded expectations; US labor market data continue to signal resilience; the US manufacturing PMI also came in stronger than expected. Long-term yields in developed markets edged lower; regional currencies strengthened slightly. Today, wage data from the euro area will be released, while in Germany detailed Q1 GDP figures and the IFO Institute’s economic sentiment index will be published; additionally, April retail sales data from the United Kingdom and domestic investment figures will also be released.

Western European indices closed mixed, while uncertainty surrounding the resolution of the Iranian conflict persisted; purchasing managers’ indices released yesterday provided a mixed assessment of the European economy; in its spring forecast, the European Commission downgraded both this year’s and next year’s growth outlook for the EU, while consumer confidence improved slightly

European equity markets closed a volatile session yesterday after Iran’s Supreme Leader signaled that the country does not intend to transfer its near weapons-grade uranium stockpiles abroad, potentially complicating negotiations with the US; the pan-European Stoxx 600 index ultimately posted a slight rise, having shifted direction multiple times during trading; market sentiment was partly supported by earlier remarks from the US president indicating that talks between Washington and Tehran are in their final stage, while the postponement of military measures is providing more time for diplomacy.

Among individual stocks, Eutelsat stood out, with its share price soaring 22%, partly driven by expectations surrounding SpaceX’s upcoming IPO; however, the gap between the two global players remains significant, as SpaceX’s valuation could reach as much as $1.75 trillion during the listing, while Eutelsat’s market capitalization stands at around €4 billion; in the aviation sector, EasyJet shares rose modestly by 0.9% despite the company reporting that the Middle Eastern conflict is slowing bookings and driving up costs; moreover, according to data released yesterday, the firm’s pre-tax loss for the half-year widened to L552 million from L394 million a year earlier.

The euro area composite purchasing managers’ index fell to 47.5 in May from 48.8 in April, significantly below the 48.8 market expectation, marking the sharpest contraction in private sector activity since October 2023; the decline was primarily driven by the services sector, where the indicator dropped to 46.4 (April: 47.6), partly reflecting price increases linked to the Middle Eastern conflict ongoing since March; manufacturing remained in expansion territory but slowed, easing to 51.4 from 52.2 in April; new orders declined markedly across both sectors, while input costs rose near a three-year high, which firms passed on to consumers; amid weakening demand and deteriorating outlooks, employment fell for a fifth consecutive month; while the euro area manufacturing PMI stayed in expansion, Germany’s reading declined to 49.9 from 51.4 in April, missing the 51.0 consensus, and the French figure also slipped below the 50 threshold into contraction at 48.9 from 52.8, representing both a notable deterioration and a significant shortfall relative to the 52.2 expectation; meanwhile, hourly labor costs in the euro area increased by 3.3% year-on-year in Q1 2026, matching the pace recorded in the previous quarter.

Consumer confidence in the euro area improved in May, with the indicator rising to -19 from -20.6 in April and coming in above the market expectation of -20.8; nevertheless, sentiment remained firmly in negative territory, still significantly below its long-term average and below levels seen prior to the outbreak of the Middle Eastern conflict; subdued confidence continues to be driven by rising CPI risks, fueled by intensifying price pressures linked to the war in the region.

The European Commission today released its spring economic forecast, in which it downgraded its EU GDP growth projections by 0.3 percentage points to 1.1% for this year and by 0.1 percentage points to 1.4% for next year.

Regional indices closed mixed yesterday: the Prague index rose, while the Budapest and Warsaw indices declined; among domestic blue chips, only Magyar Telekom posted a rise, while the other three stocks fell.

Overseas indices moved higher; oil prices declined by the end of the session; Nvidia’s earnings exceeded expectations; US labor market data continue to present a favorable picture; the US manufacturing PMI also came in stronger than expected

US equity markets closed higher yesterday, while a notable reversal was seen in oil markets: prices initially rose following reports that Iran does not intend to ship enriched uranium abroad, but by the end of the session they corrected as investors expressed hope that the coming days could bring a diplomatic breakthrough between Iran and the US; among corporate developments, Nvidia’s earnings report was in focus, as the chipmaker delivered results and guidance above expectations and announced a dividend increase, yet its shares fell by around 1.8%, reflecting elevated market expectations toward leading companies in the AI sector.

Recent data from the US labor market continue to point to stability; initial jobless claims fell by 3,000 to 209,000 in the second week of May, broadly in line with expectations (210,000); the figures continue to reflect the resilience of the labor market and allow for the maintenance of a restrictive monetary policy stance; the composite purchasing managers’ index, measuring business activity, held steady at 51.7 in May, signaling moderate but stable expansion in the private sector; industrial performance was particularly strong, with the manufacturing PMI rising to 55.3 from 54.5 in the previous month, marking a near four-year high; by contrast, the services PMI edged down from 51 to 50.9; however, the manufacturing growth picture is partly overshadowed by the fact that it was again supported by temporary inventory build-up, while input costs increased sharply due to rising energy prices and ongoing supply chain disruptions.

In the US, the number of building permits rose by 5.8% month-on-month in April to an annualized rate of 1.442 million, up from 1.363 million in March, exceeding the market expectation of 1.39 million; in contrast, housing starts declined by 2.8% on a monthly basis to an annualized 1.465 million, down from 1.507 million in March, which had marked the highest level since December 2024, although the figure still came in above the 1.41 million consensus.

Long-term yields in developed markets edged lower; regional currencies strengthened slightly

Oil prices, after an initial rise, ultimately declined slightly yesterday, as US Secretary of State Marco Rubio also struck an optimistic tone regarding negotiations with Iran; in the euro area, purchasing managers’ indices came in worse than expected due to the oil price shock, with both services and the overall economy slipping deeper into contraction territory than anticipated; preliminary Q1 labor cost data were also released, remaining at 3.3%, a level that is not yet fully reassuring from a CPI perspective; US purchasing managers’ indices broadly met expectations and remained in a range consistent with ongoing economic expansion, supported by the continued low number of new jobless claims last week; developed market bond yields also edged lower yesterday following Wednesday’s notable decline from previous peaks, with the US 10-year yield falling below 4.6% and the German 10-year below 3.1%; the EURUSD pair was broadly unchanged, holding above the 1.16 level.

Regional currencies strengthened slightly by 0.1–0.2% against the euro, with the forint once again reaching the 358.5 level; demand was strong at yesterday’s Government Debt Management Agency (ÁKK) auctions for both the one-year treasury bills and the 10-year fixed-rate bonds, with bids totaling HUF 120 billion and nearly HUF 200 billion, respectively; the ÁKK responded by issuing more than HUF 50 billion of the one-year bills and HUF 100 billion of the 10-year bonds at average yields of 5.66% and 5.49%; however, demand for the 10-year floating-rate bond was weak, with only two-thirds of the announced HUF 15 billion finding buyers; benchmark yields increased by around 5 basis points, with the 10-year yield hovering near 5.6%.

Today's highlights

Asian indices were higher this morning; core inflation in Japan declined more than expected, supporting gains in the Japanese equity market as it reduced the likelihood of an early rate hike.

Today, wage data from the euro area will be released, while in Germany detailed Q1 GDP figures and the IFO Institute’s economic sentiment index will be published; additionally, April retail sales data from the United Kingdom and domestic investment figures will also be released.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more