OTP Morning Brief: Trump adopts a more conciliatory tone, crude oil prices are falling on Tuesday morning

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

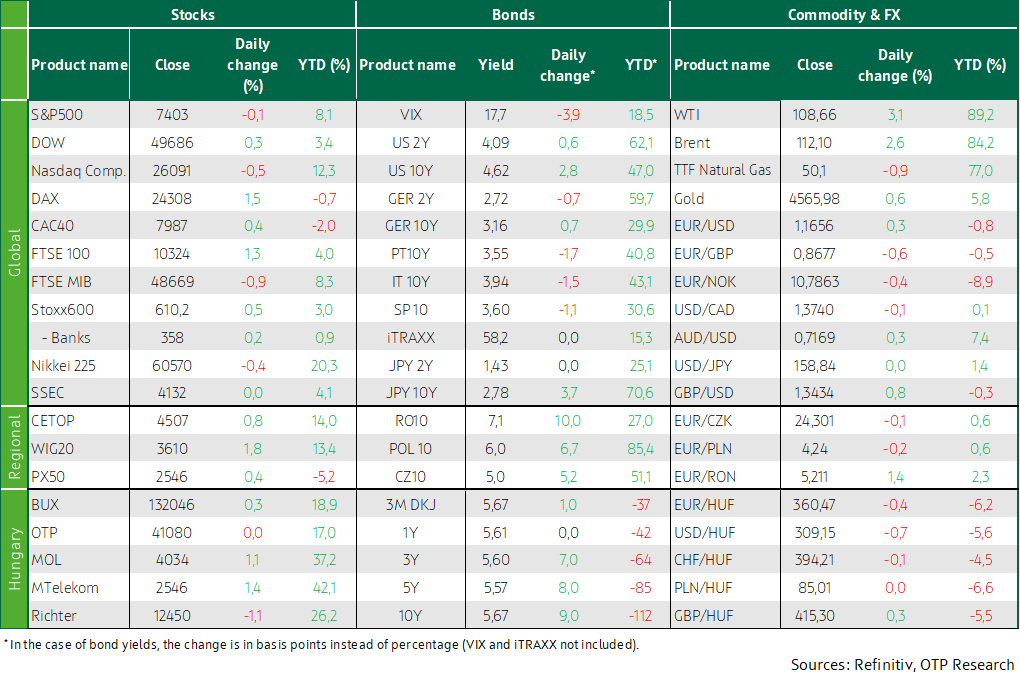

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

After Monday’s volatile trading, crude oil prices are falling this morning. President Trump announced on Monday evening that he has suspended the planned strike against Iran to create an opportunity for negotiations on ending the war, after Tehran sent a new peace proposal to Washington. Trump also stated that there is a “very good chance” of reaching a nuclear agreement. The fact that the situation in the Middle East did not escalate further created a positive sentiment on Western European equity markets on Monday, with major indices seeing a rise after last Friday’s decline. In the US, the situation was mixed, as valuation concerns due to the rise in long-term yields and profit-taking following the AI-driven rally in April weighed the technology sector down. Long-term yields in Western Europe declined or saw only a slight rise, while the US 10-year yield closed at 4.62%. The week started with a correction in the EUR/USD market following last week’s dollar rise, while EUR/HUF is approaching 360. Better-than-expected Q1 GDP growth data were released this morning in Japan. UK unemployment data and US home sales statistics will be released today. Home Depot reports earnings in the US today.

The week started on a positive note in European stock markets

After Friday’s decline, the week started with a modest rise on major Western European equity markets: the Stoxx 600 edged up 0.5%, the DAX gained 1.3%, the FTSE 100 rose 1.0%, and the CAC 40 closed 0.6% higher following volatile trading on Monday, while the Italian benchmark was the outlier, underperforming with a 0.9% decline. At the same time, market participants had little reason for stronger optimism, as there was no progress in resolving the Middle East conflict, global oil inventories are declining, and crude prices continued to rise after last week’s increase, keeping CPI concerns in focus, while long-term yields showed little movement following last week’s notable rise. Among Stoxx 600 sector indices, media delivered the strongest performance, supported by Publicis after the advertising company announced it will acquire US-based LiveRamp for USD 2.2 billion, while the energy, utilities, and travel sectors also performed well. Ryanair soared nearly 5% after reporting record annual profit and stating that the risk of jet fuel shortages has effectively disappeared, Sonova surged almost 8% after the world’s largest hearing aid manufacturer forecast higher annual revenue and profit, Commerzbank lost 1.5% after rejecting UniCredit’s takeover bid, and Deutsche Börse gained nearly 5%.

Meanwhile, CEE equity markets all started the week with a rise: the WIG20 closed up 1.8%, the BUX gained 0.3%, and the PX edged 0.4% higher. Among Hungarian blue chips, 4iG surged 4%, while Magyar Telekom and Mol supported the BUX with gains exceeding 1%, Richter lost 1.1% of its value, and OTP slipped by 0.05%.

The price of European TTF natural gas fell by more than 1% on Monday, returning to the EUR 50/MWh level.

The Nasdaq continues to fall, with significant pressure on the technology sector amid rising yields, while investors are awaiting Nvidia’s earnings report on Wednesday

There was no progress regarding the situation in Iran, and following Friday’s pullback, sentiment remained mostly subdued on US equity markets. The Dow rose 0.3%, the S&P 500 lost a few points, while the Nasdaq Composite closed 0.5% lower. Since the late-March low following the strike against Iran, the S&P has surged 18% and the Nasdaq 28%, with the rise driven by enthusiasm around artificial intelligence and the quarterly performance of the technology sector. This now appears to have come to an end, as market analysts point to the arrival of profit-taking, partly due to long-term yields at over one-year highs weighing on valuations. Fed funds futures are now pricing in a 36% probability of a 25bp Fed rate hike by the end of this year. It is therefore not surprising that technology was the weakest performer among S&P sector indices on Monday, with the Philadelphia Semiconductor Index falling 3.3%. The energy sector posted the strongest gains, followed by consumer staples and financials. Several notable corporate developments also emerged: Dominion Energy surged more than 9% after NextEra Energy announced it would acquire the utility company for USD 66.8 billion, while NextEra fell 4.6%. Pharmaceutical company Regeneron plunged nearly 10% after news that its experimental drug failed to meet targets in a late-stage clinical trial.

Crude oil prices continued to edge higher during Monday trading and closed the day with a 3% surge.

Rate hike expectations did not strengthen further significantly, with long-term yields in developed bond markets remaining close to their Friday levels; the euro strengthened against the dollar, while EUR/HUF slipped close to 360

Oil prices started Monday with a significant surge, although trading in the crude market was marked by notable volatility. As the situation in the Middle East did not escalate further, rate hike expectations in developed bond markets stopped strengthening, and the rise in yields slowed. The US 10-year yield closed near 4.6%, while the German yield ended at 3.16%. Last week’s significant dollar surge was followed by a correction, with the euro appreciating by a quarter of a percent against the dollar to the 1.165 level.

Regional currencies strengthened slightly, with the Czech koruna gaining 0.1%, the Polish zloty 0.2%, and the forint 0.4%, while EUR/HUF once again approached the 360 level. Reference yields set by the Government Debt Management Agency (ÁKK) early in the afternoon moved higher again by 5–10 basis points, with the 10-year yield rising to around 6.7%, but by the evening selling pressure eased and yields slipped a few basis points lower. The ÁKK also announced that it will cut interest rates on retail government bonds by 50 basis points.

Today's highlights

Asia-Pacific equity markets show a mixed picture ahead of this morning’s close: Japanese indices are mostly in positive territory, although the Nikkei is down 0.6%. In Japan, sentiment was supported by stronger-than-expected Q1 GDP data, with annualized year-on-year growth at 2.1% versus the expected 1.7%, although the fourth-quarter figure was revised down (from 1.3% to 0.8%). The Shanghai Composite is flat, the CSI 300 has declined by 0.5%, while the Hang Seng has risen 0.4%. South Korean indices are down 4% on Tuesday morning due to a sell-off in the technology sector.

Futures equity indices point to a mostly negative opening today in both Europe and the US.

Crude oil futures are falling this morning after President Trump announced on Monday that he has suspended the planned strike against Iran to create an opportunity for negotiations on ending the war, following a new peace proposal sent by Tehran to Washington. Trump also stated that there is a “very good chance” that the US will reach an agreement with Iran to prevent Tehran from obtaining nuclear weapons.

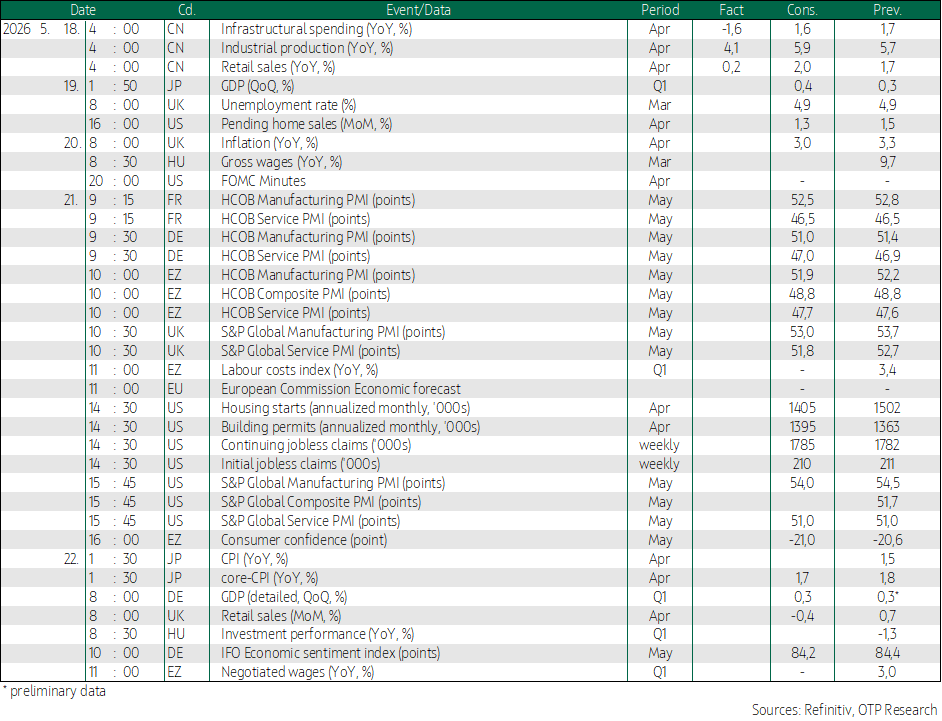

Aside from UK unemployment data and US pending home sales figures, no major releases are expected today. Home Depot reports earnings today, although investors are likely to be more focused on Nvidia’s earnings release after Wednesday’s close and Walmart’s report on Thursday.

The debt management agency will auction three-month T-bills today in a total amount of HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more