OTP Morning Brief: Fears of inflation and interest rate hikes have intensified

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Major European indices fell on Friday and over the week due to growing inflation fears. Trading on Wall Street was also gloomy on Friday, and on weekly basis, only the S&P was able to avoid a drop. Stock markets in the CEE region closed mixed on Friday; the BUX fell, ending the past week in negative territory. The Strait of Hormuz remains closed, Brent and WTI prices rose. Interest rate hike expectations strengthened and yields rose in developed bond markets. The dollar strengthened. The forint weakened. Domestic bond yields showed a correction on Friday from levels not seen since the Russia-Ukraine war. The meeting between Donald Trump and Xi Jinping did not bring significant tangible results. There will be no lack of important macroeconomic data this week. The Hungarian Central Statistical Office (KSH) will publish March wage data and Q1 investment statistics. The eurozone will release May PMIs and Q1 labor cost and wage statistics. In the US, the May PMIs will be published.

Rising CPI concerns; leading European indices declined both on Friday and over the week; the BUX closed in the red both on the last trading day and on a weekly basis

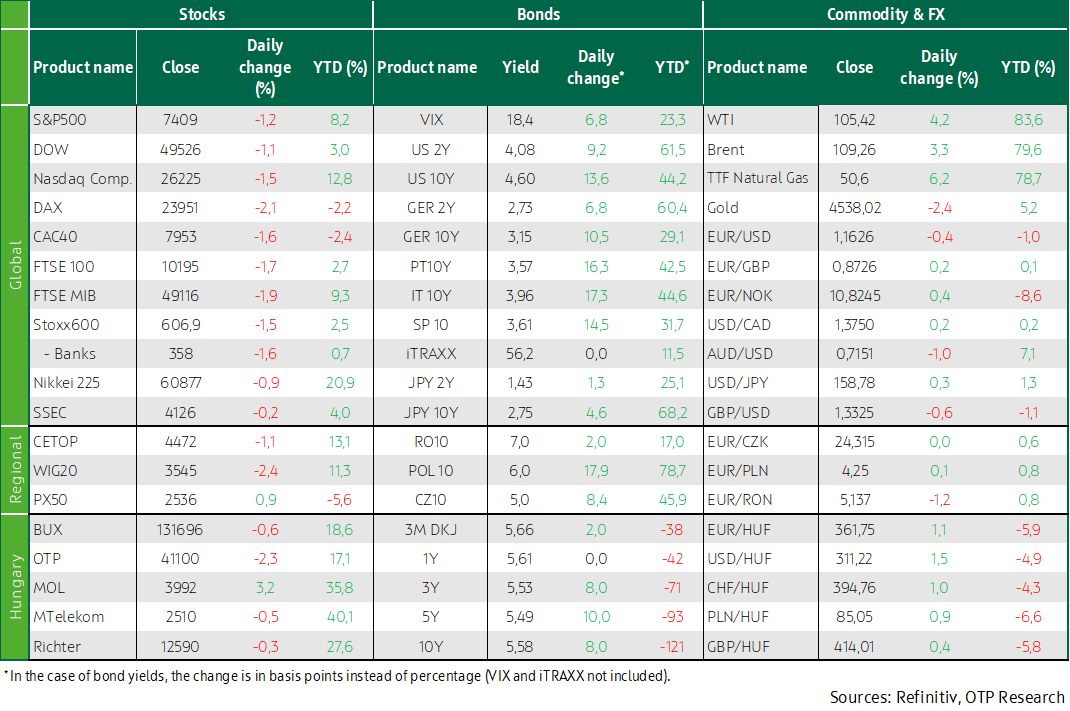

Leading European indices closed in negative territory on Friday. The pan-European Stoxx 600 slipped 1.5% after gains on Wednesday and Thursday. Among major indices, Germany’s DAX was the day’s worst performer, falling 2.1%. At the sector level, materials saw the sharpest decline (-5.1%) amid falling metal prices, while banks and other cyclical stocks also came under pressure. The recent momentum of semiconductor stocks faded, with profit-taking emerging in the tech sector—ASML dropped 4.4% and Aixtron fell 6%. There was, however, one standout semiconductor company; Italy’s Technoprobe surged 32.3% after the company revised up its 2026 outlook. Stellantis declined 3.5% after the company signed an agreement worth around EUR 1 billion with China’s Dongfeng to manufacture Peugeot- and Jeep-branded vehicles. LVMH fell 1.1% after the luxury goods conglomerate agreed to sell the Marc Jacobs brand.

Over the week as a whole, major European equity indices also moved lower, with the biggest losers being the DAX (-1.6%) and the CAC 40 (-2.0%). Although favorable corporate earnings reports and strength in semiconductor stocks supported equity markets at the beginning of the week, these gains were ultimately offset by concerns over accelerating CPI. Meanwhile, political tensions remain elevated in the United Kingdom; Prime Minister Keir Starmer is fighting to retain his position following a significant defeat in regional elections.

CEE equity markets delivered mixed performance on Friday, with the PX managing to rise while both the WIG20 and the BUX declined. Among Hungarian blue chips, only MOL managed to move higher. On a weekly basis, the BUX was the only index in the region to close in negative territory (-2.1%), while among domestic large caps, Magyar Telekom was the only stock to post gains.

The price of European TTF natural gas rose by more than 15% over the week, climbing above EUR 50/MWh.

Wall Street closed Friday in negative territory; over the week as a whole, only the S&P managed to rise; Brent and WTI prices continued to rise

Leading Wall Street indices closed lower on Friday: the Dow Jones fell 1.1%, the S&P 500 declined 1.2%, while the NASDAQ dropped 1.5%. Among the S&P sector indices, only energy managed to rise (+2.3%), while the largest losses were recorded in the materials and utilities sectors. The Philadelphia SE semiconductor index fell 4% as indices began to pull back from the AI-driven surge, with investors taking profits.

Among individual stocks, a few names also stood out. Microsoft shares rose 3.1% after it was announced that Bill Ackman’s hedge fund had taken a new position in the company. Dexcom, the medical device manufacturer, surged 6.6% following the announcement of corporate governance changes. Ford fell 7.5% after a rally over the previous two days.

Despite Friday’s performance, the S&P 500 posted its seventh consecutive weekly gain. The NASDAQ and the Dow both closed the week in negative territory, with the former snapping a six-week winning streak.

Friday marked Jerome Powell’s final day as Fed Chair, with Kevin Warsh—who has promised a sharp shift in monetary policy—taking over the role. The two-day meeting between Donald Trump and Xi Jinping also concluded on Friday, delivering little in terms of tangible results. Donald Trump is increasingly eager to bring the Middle East conflict to a close and has been communicating more forcefully that his patience with Iran is wearing thin, as involvement in the conflict is unpopular among US voters and the midterm elections are only months away.

Over the past week, crude oil prices edged higher on every day except Wednesday, with WTI rising 10.5% and Brent crude rising 7.9%.

Rate hike expectations strengthened and yields roseacross developed bond markets; the US dollar strengthened; the forint weakened;Hungarian bond yields corrected on Friday from levels not seen since theoutbreak of the Russia–Ukraine war

US–China talks failed to deliver meaningful progress regarding the war involving Iran, the Strait of Hormuz remains closed, oil demand significantly exceeds supply, global inventories are declining, and an increasing number of countries are being forced to introduce restrictions. As a result, oil prices rose gradually last week. Moreover, in April, US CPI increased to 3.8% and core CPI rose to 2.8%, both exceeding expectations. Inflation and rate hike concerns intensified, pushing yields to critical levels across developed bond markets. While the most likely scenario for US interest rate expectations remains that the Fed will leave the current 3.5–3.75% policy rate unchanged until year-end, the previously symmetric distribution has shifted, with markets now assigning a 50% probability to a hike, and pricing in a policy rate 25 basis points higher by the end of 2027. The 10-year US yield rose by 10 basis points on Friday and by 25 basis points over the week, reaching 4.6%, a one-year high and close to the upper end of the post-pandemic trading range. In Europe, rate hike expectations also strengthened, with markets pricing in at least three 25 basis point hikes by year-end. Germany’s 10-year yield rose by more than 10 basis points on Friday and by over 15 basis points over the week, surpassing 3.15%, a level not seen in one and a half decades. In Japan, a weakening currency and rising inflationary pressure drove rate hike expectations higher, pushing bond yields to near four-decade highs, with the 10-year reaching 2.7%. Amid the negative sentiment, the US dollar strengthened by nearly 0.5% on Friday and by 1.5% over the week, while EUR/USD fell from 1.178 to 1.163.

Domestic markets moved with a different dynamic than global trends, but by Friday the deterioration in the external environment was also felt locally. Driven by post-election optimism, the forint opened Monday’s trading below 355 against the euro, a level not seen since 2021. The depreciation was further accelerated by the weakening external backdrop and by the MNB’s decision on Wednesday to cut the rate on its FX swap tender providing FX liquidity from 5.75% to 5.25%—the lower bound of the forint overnight interest rate corridor—effectively redirecting demand from the forint toward the bond market. Market expectations for rate cuts strengthened, with markets pricing in two to three 25 basis point cuts instead of a hold, while bond yields fell by another 20–30 basis points to around 5.5%, levels not seen since the start of the war in Ukraine. At Thursday’s government bond auction, demand was exceptionally strong, with bids of around HUF 700bn (!!!), while the Debt Management Agency issued HUF 310bn worth of bonds. On Friday, however, the deteriorating external environment and the rise in developed market yields spilled over into the domestic market, with benchmark yields increasing by 5–10 basis points and the 10-year yield correcting to 5.6%.

Today's highlights

Asia-Pacific equity markets were in negative territory heading into the final hour of trading this morning. Concerns over an escalation of the Middle East conflict intensified over the weekend, while crude oil prices continued to rise. Weaker-than-expected April activity indicators were released from China this morning; growth in industrial production and retail sales fell short of expectations, while investment momentum declined on a year-on-year basis.

Futures on equity indices point to a negative open this morning in both Europe and the United States.

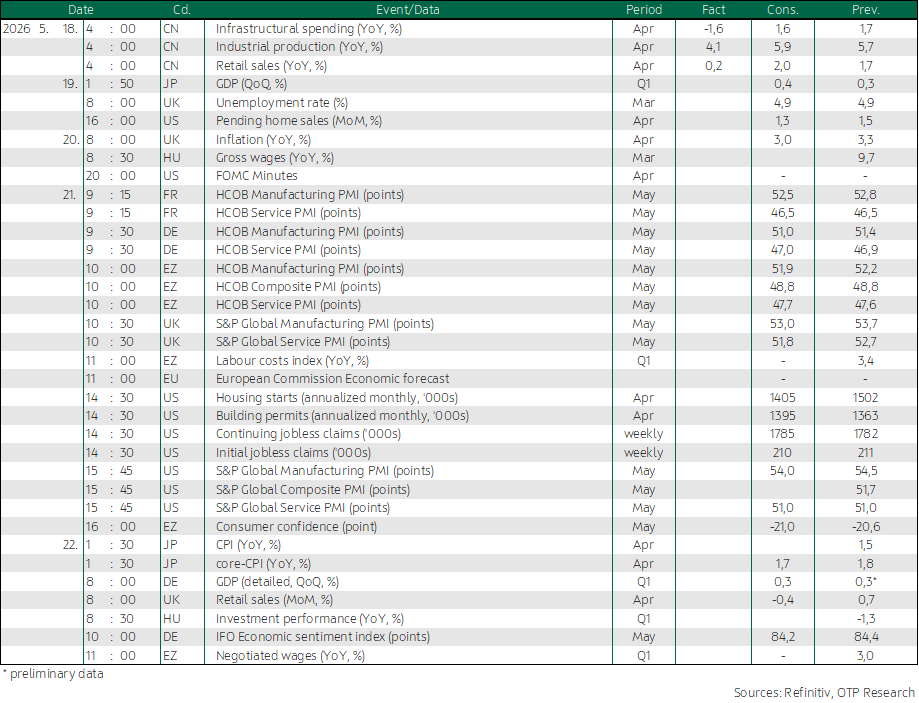

There will be no shortage of important macro data this week. The Hungarian Central Statistical Office will release March wage data as well as Q1 investment statistics. From the euro area, May purchasing managers’ indices and Q1 labour cost and wage data are due. In the United States, May purchasing managers’ indices will also be published.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more