OTP Morning Brief: There was extraordinary demand for Hungarian government bonds yesterday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

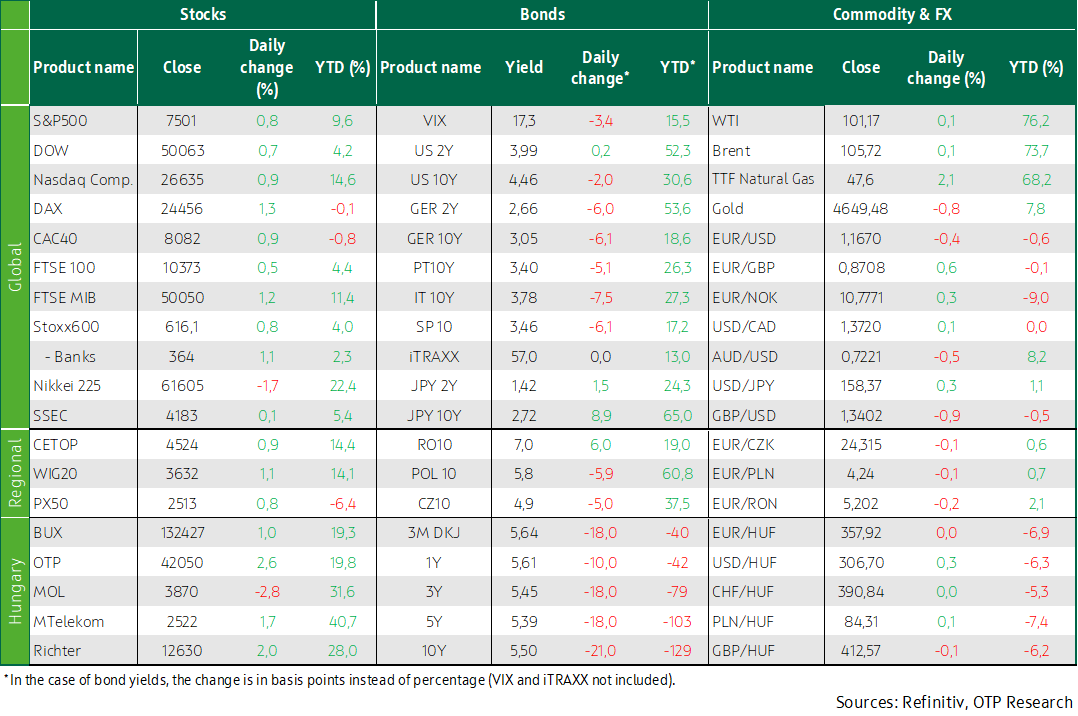

The rise continued in Western European stock markets. In the United States, stock indices also moved higher; on both sides of the Atlantic, the technology sector drove the rise. Investors are focusing on the two-day Trump–Xi meeting. In Hungary, the GKI consumer confidence index skyrocketed in May. In Q1 2026, the OTP Group continued its outstanding financial performance. US yields did not move significantly, while they fell in Europe. In Japan, the 10-year yield rose to 2.64% on Thursday, then surged by nearly another 10 basis points on Friday. Demand was outstanding at the Government Debt Management Agency’s bond auction. Domestic bond yields fell by 15–20 basis points to 5.5%. Markets have already priced in three cuts from the MNB for this year. In the morning hours, Japanese and Korean markets are falling sharply.

The rise continued in Western European stock markets

The rise seen on Wednesday continued on Thursday in Western Europe. The STOXX 600 closed 0.8% higher, the DAX rose 1.3%, the CAC 40 gained 0.9%, and the FTSE 100 edged up 0.5%. The technology sector surged by 2.6%, led by semiconductor manufacturers: STMicroelectronics climbed 5.4%, BE Semiconductor advanced 3.3%, and Infineon increased by 5.7%. Shares of SAP rose 3.6% after Bank of America issued a favorable assessment of the German software giant’s growth prospects. Luxury player Burberry fell 6.8% after fourth-quarter sales met expectations. Watches of Switzerland, known as a retailer of luxury goods, soared by 19.2% after forecasting full-year operating profit above expectations.

According to preliminary data, the United Kingdom’s economy expanded by 1.1% year-on-year in Q1, exceeding expectations of 0.8%. Despite the positive data, the pound weakened by 0.95% against the dollar amid a domestic political crisis. UK Prime Minister Keir Starmer is facing a serious challenge following a significant defeat in last week’s regional elections. Health Secretary Wes Streeting—considered a potential successor—announced his resignation, stating that he had lost confidence in Starmer. Poland’s economic growth slowed to 3.4% year-on-year from 4.1% in Q4.

Ahead of the summer peak tourist season, Europe’s jet fuel supply is becoming an increasingly pressing issue. Under normal circumstances, the Persian Gulf provides around one-quarter of the continent’s aviation fuel. Tour operators and airlines are urging calm, partly because physical kerosene supply remains secured for now—albeit at a significant premium—and partly to avoid panic-driven cancellations. According to the IEA and market analysts, European commercial jet fuel inventories were sufficient for about six weeks at the end of April. By summer 2026, inventories across several European countries could fall close to the critical 20–25 day level if the Strait of Hormuz is not reopened.

In Hungary, the GKI consumer confidence index skyrocketed by an unprecedented 16.1 points in May. A more favorable reading had last been seen in 2019. The sharp rise in the confidence index may reflect expectations related to the new government’s economic policy. Yesterday, the Hungarian government decided to release 575 million liters of fuel from strategic fuel reserves.

In the region, the BUX rose by 1%, led by OTP. The Polish WIG20 closed 1.1% higher, while the Czech PX50 gained 0.8%.

OTP Group 1Q 2026 Results

In the first quarter of 2026, the OTP Group continued its outstanding financial performance. Profit after tax amounted to HUF 324 billion, while the annualised return on equity (ROE) reached 23.5%. These indicators were calculated taking into account the pro-rata effect of special items recognised upfront for the full year.

Consolidated net interest income improved by 13% y-o-y, driven primarily by the continued dynamic expansion of business volumes. In addition, the net interest margin increased by 32 bps y-o-y to 4.59%. The Group’s risk profile remained favourable: the ratio of Stage 3 loans declined by 0.1 pps q-o-q, standing at 3.5% at the end of March.

Performing (Stage 1+2) loan volumes increased by 3% FX-adjusted during the first quarter, resulting in annual growth of 16%. Retail portfolios remained the main growth driver: mortgage loan volumes rose by 22% y-o-y, while consumer loan volumes increased by 16%. Under the government-supported Home Start Loan Program launched in September 2024, the OTP Bank received total loan applications amounting to HUF 588 billion by the end of 1Q 2026, of which loan agreements were concluded for HUF 502 billion, corresponding to a 43% market share.

Consolidated corporate (including MSE) loan volumes expanded by 4% q-o-q, resulting in 13% growth on an annual basis with most of the Group members recording a y-o-y loan growth above 10%.

Consolidated deposits increased by 11% y-o-y FX-adjusted. Within this, Hungarian retail deposits grew by 9% q-o-q, while in Bulgaria retail deposits increased by a further 2%, following the significant inflows recorded towards year-end in connection with the introduction of the euro. The net loan-to-deposit ratio stood at 77% at the end of 1Q 2026.

The outstanding issued securities increased by 16% during the first quarter of 2026. As part of this, the OTP Bank issued a EUR 500 million Senior Preferred unsecured bond with a value date of 3 February 2026, followed by the issuance of a EUR 500 million mortgage bond by OTP Mortgage Bank with a settlement date of 12 February 2026.

The OTP Group’s IFRS consolidated CET1 ratio declined by 51 bps q-o-q and stood at 17.6% at the end of March, in line with the Tier 1 ratio. The Bank continues to comfortably comply with the supervisory MREL requirement applicable to the OTP resolution group: the MREL ratio reached 25.6% at the end of March 2026, compared with the 24.2% minimum requirement.

Management does not consider it necessary to revise its expectations for the Group’s performance in 2026.

In the United States, the technology sector also led the rise

The positive sentiment seen on Wednesday continued on Wall Street. The S&P 500 and the Nasdaq both reached new record closing highs. The major indices rose by 0.8–0.9%, driven primarily by the technology sector. Tesla CEO Elon Musk and Nvidia CEO Jensen Huang were also part of the delegation that visited China with President Trump. Nvidia shares rose 4.4% after the United States approved the sale of the company’s H200 chips to Chinese firms. At the same time, shares of other AI-related companies, including Qualcomm, Intel, Sandisk, and Micron, fell by more than 3%. Cisco shares soared by 13.4% after the company announced a workforce reduction of nearly 4,000 employees and raised its full-year revenue outlook. According to Trump, China agreed to purchase 200 Boeing aircraft; nevertheless, the aircraft manufacturer’s shares fell by 4.7%.

Retail sales in April expanded by 0.5% month-on-month, in line with expectations. A notable feature of the US retail data is that it is not adjusted for price effects, meaning it does not reflect pure volume growth. It is therefore not surprising that amid the ongoing Iranian conflict, fuel sales showed the strongest increase (+2.8%) due to higher prices. Elevated fuel prices may pose a risk to the economic outlook if they begin to crowd out spending in other areas of consumption over time. Higher tax refunds this year could temporarily offset this effect. Initial jobless claims last week (211,000), while slightly above expectations, remain more favorable than in the same period last year and continue to reflect the stability of the labor market.

In recent days, investors’ attention has turned to the two-day Trump–Xi meeting. The Chinese president warned his American counterpart that disagreements over Taiwan could lead to conflict between the two countries. US statements regarding the meeting highlighted a shared intention to reopen the Strait of Hormuz, as well as the possibility of China purchasing US oil. In addition to oil, the US side aims to secure sales of Boeing aircraft and agricultural products, while the Chinese side is seeking an easing of US export restrictions on chips.

Exceptional demand at yesterday’s auction, with domestic bond yields falling by 15–20 basis points to 5.5%

No market-moving information emerged from the US–China talks; oil prices rose slightly by 0.5%, while U.S. retail sales data came in marginally stronger than expected. U.S. bond yields did not move significantly, with the 10-year yield still approaching 4.5%. In Europe, bond yields fell: the German 10-year declined by 5 basis points, while French and Italian yields dropped by nearly 10 basis points, though they remained close to 15–20 year highs, with the German yield at 3.06%. The situation is even more pronounced in Japan, where the 10-year yield rose to 2.64% on Thursday—close to a 30-year high—driven by strengthening rate hike expectations. On Friday, Japanese yields continued to rise more steeply, with the 10-year yield soaring by nearly another 10 basis points based on morning data. The dollar strengthened by 0.3% against the euro, reaching 1.167.

There was no meaningful movement in regional currencies, with the zloty, the koruna, and the forint all strengthening slightly against the euro; EUR/HUF closed below 358. The rally in the bond market continued, gaining further momentum yesterday after the TISZA party’s two-thirds victory, as rate cut expectations strengthened following the MNB’s decision on Wednesday to lower the yield on its FX swap tender providing foreign currency liquidity from 5.75% to 5.25%—the lower bound of the forint overnight interest rate corridor. Markets are now pricing in three rate cuts by year-end. At yesterday’s three-, five-, and ten-year bond auctions held by the Government Debt Management Agency (ÁKK), demand was exceptionally strong—surpassing even eurobond auctions—with around HUF 700bn (!!!!) in bids submitted for the three instruments. The ÁKK issued HUF 310bn worth of bonds at average yields of around 5.5%, 15–20 basis points below Wednesday’s reference yields. As a result, reference yields fixed in the early afternoon also fell to around 5.5%, levels not seen since Q1 2022.

Today's highlights

As the close approaches, Japanese and Korean stock indices are falling sharply. In Japan, producer price index-type data released early in the morning came in higher than expected, and strengthening inflationary pressure is also reinforcing rate hike expectations. The Nikkei is down 1.7%, while the KOSPI is plunging by 4.9%. Elsewhere in Asia, the SSEC is rising by 0.1%, while the Hang Seng is down 0.9%.

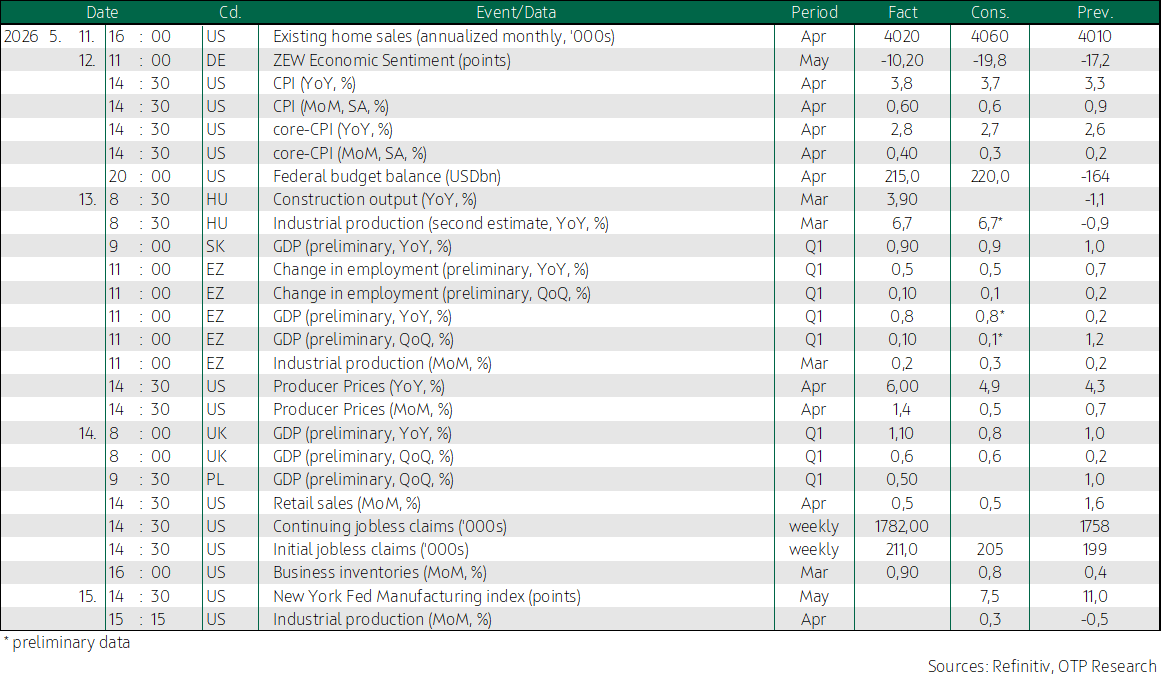

From a macro perspective, we expect a relatively quiet day. From the United States, the New York Fed’s May manufacturing index and April industrial production data are due.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more