OTP Morning Brief: The technology sector led the charge on US stock markets

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

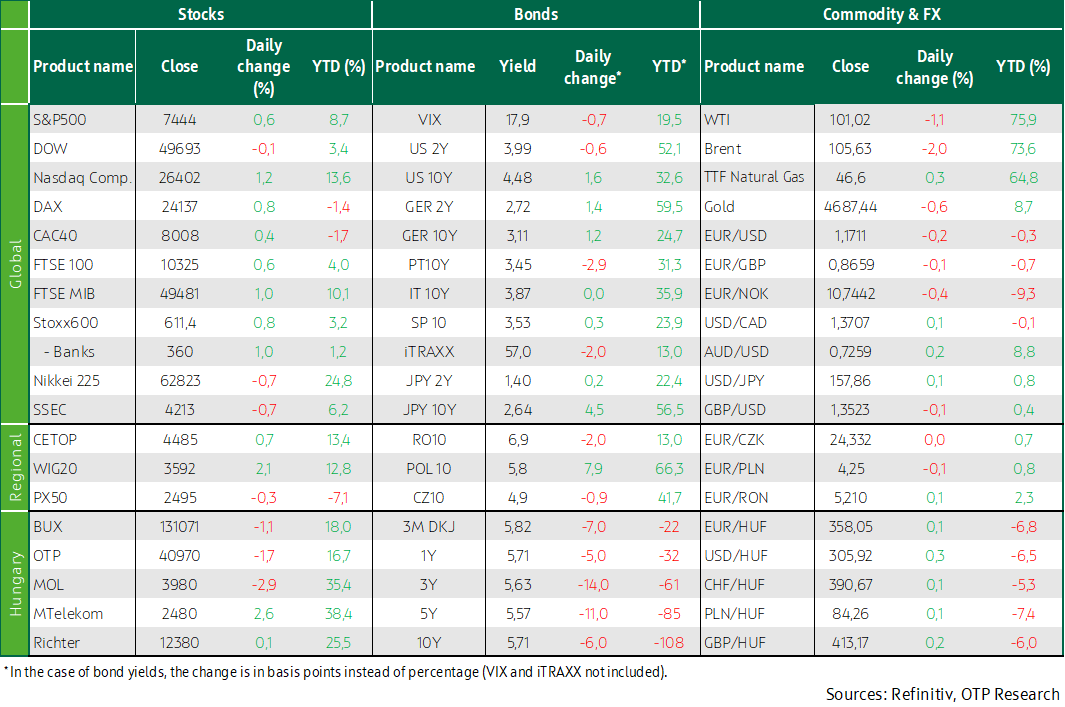

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

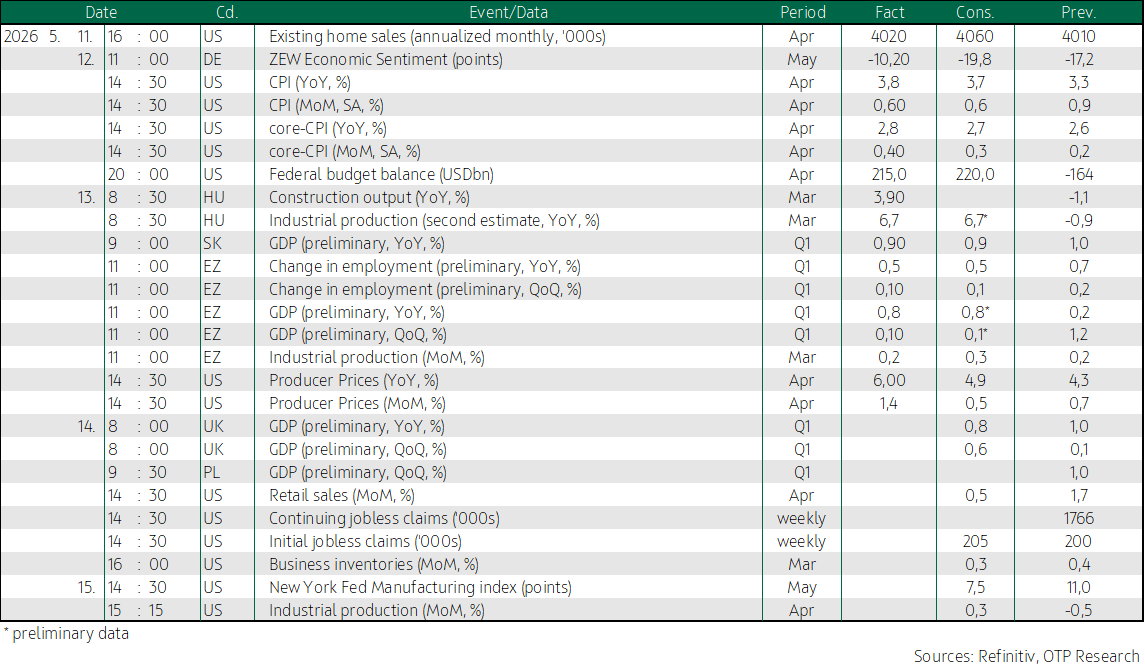

Western European markets rose, while no resolution is in sight to the US–Iran conflict; euro area industrial production came in below expectations, GDP growth was in line with the preliminary reading, and employment slowed as expected. US indices closed mixed, with the technology sector performing the best; US producer prices rose more than expected. Developed market long-term yields were mixed; the dollar strengthened against the euro, the forint weakened following the MNB’s decision, and domestic bond yields fell. Today, UK and Polish GDP data will be released. In the United States, alongside the usual weekly initial jobless claims figures due on Thursday, retail sales and business inventory data will also be published.

Western European markets rose, while no resolution is in sight to the US–Iran conflict; euro area industrial production came in below expectations, GDP growth was in line with the preliminary reading, and employment slowed as expected

Leading European equity indices rose on Wednesday: the Stoxx 600 index climbed by around 0.8%, with most sectors trading in positive territory. The UK government bond market was initially reassured after Prime Minister Keir Starmer signaled he would remain in office despite pressure to resign; however, uncertainty increased again during the day following press reports suggesting he may soon face an internal party challenger. Siemens announced that it delivered better-than-expected profit in Q1 and will launch a 6 billion euro multi-year share buyback program; its share price rose by 0.8%. Market sentiment continued to be shaped by the lack of a quick resolution to the US-Iran conflict, while the focus gradually shifted toward the upcoming Trump- Hszi Csin-ping meeting, where alongside trade issues, the situation regarding Iran could also be on the agenda.

Recent data from the euro area paint a subdued and slightly weaker-than-expected economic picture. Industrial output in March grew by 0.2% month-on-month, matching the February reading but falling short of the 0.3% increase expected by the market. There is significant divergence across countries: Germany recorded a 1.2% decline compared to the previous month, while France (+1.0%), Italy (+0.7%) and especially Spain (+2.4%) posted growth. On an annual basis, industrial production fell by 2.1%, coming in worse than the market expectation of -1.7%.

Euro area GDP growth in Q1 came in at 0.1%, in line with the preliminary estimate, marking the weakest pace since Q2 2025. The slowdown was primarily driven by energy supply disruptions, as the Middle East conflict disrupted oil and LNG shipments, resulting in rising CPI risks and more restrictive monetary policy expectations. Performance across major economies was also mixed: France stagnated quarter-on-quarter, the Netherlands and Italy posted modest growth (0.1% and 0.2%, respectively), Germany saw a slight acceleration (+0.3%), while Spain continued to outperform (+0.6%). On an annual basis, GDP growth slowed to 0.8% from 1.3% in the previous quarter.

Euro area employment increased by 0.1% quarter-on-quarter in Q1, in line with market expectations, but marking a slowdown from 0.2% in the previous quarter. This represents the 20th consecutive quarter of growth, continuing to signal the resilience of the labor market, albeit with moderating momentum. At the country level, employment growth remained strong in Spain (+0.3%, though slowing from 0.8% in the previous quarter), while in Germany it declined for the third consecutive quarter (-0.1%). On an annual basis, employment growth slowed to 0.5%, the weakest pace since 2021, indicating that higher energy prices and the weak growth environment are beginning to weigh on labor market expansion as well.

Regional indices closed mixed yesterday: the Warsaw index rose, while the Budapest and Prague indices declined. Among Hungarian blue chips, MTelekom and Richter advanced, while the other two stocks fell. Incoming data from the Hungarian economy for March painted a mixed picture. Construction output grew by 3.9% year-on-year, marking a meaningful rebound after the 1.1% decline in February; growth was supported by both buildings (+4.4% after +1.7%) and civil engineering works (+3.0% after -7.7%). At the same time, for Q1 as a whole, the sector’s performance was still 4.2% below the level seen a year earlier. In contrast, industrial production showed a notably strong picture: adjusted for working days, it expanded by 3.7% year-on-year, representing a meaningful turnaround after the 0.9% decline in February. For Q1 as a whole, industrial output increased by 1% year-on-year.

US indices closed mixed, with the technology sector performing the best; US producer prices rose more than expected

US indices delivered a mixed performance on Wednesday, as strength in the technology sector offset data showing higher-than-expected producer inflation: the S&P 500 and Nasdaq rose, while the Dow Jones declined. Market moves were clearly dominated by technology and semiconductor stocks, supported by persistent growth expectations linked to AI and their role as a perceived safe haven amid geopolitical uncertainty. Tech stocks were also supported by news that the head of Nvidia attended the Trump-Hszi meeting, boosting hopes for potential positive developments regarding access to the Chinese market, while investors continued to closely monitor geopolitical events and their impact on CPI.

US producer prices surged by 1.4% month-on-month in April, marking the largest increase since March 2022, following a 0.7% rise in March and significantly exceeding the 0.5% market expectation; the increase was primarily driven by a 2% rise in goods prices, with gasoline prices soaring by 15.6% due to higher oil prices related to the Iran conflict, while prices for jet fuel, diesel, vegetables, and industrial chemicals also increased; service prices also rose significantly by 1.2% (the fastest pace since March 2022), mainly due to a 3.5% increase in wholesale margins for machinery and equipment, while transportation, retail, and legal service costs also moved higher; on an annual basis, producer prices rose by 6.0%, the highest level since the end of 2022, exceeding the 4.9% market expectation and accelerating from the upwardly revised 4.3% in March.

Developed market long-term yields were mixed; the dollar strengthened against the euro, the forint weakened following the MNB decision, and domestic bond yields fell

Although the situation in the Middle East did not improve and the strait remains closed, oil prices corrected lower by 1-2% yesterday after several days of gains; despite this, bond markets closed mixed after the April increase in producer prices exceeded expectations by around 1 percentage point in both Germany (6.3% year-on-year versus 5.3%) and the US (6.3% year-on-year versus 4.3%); other macroeconomic data, including euro area Q1 GDP and employment figures, did not deliver surprises; the German 10-year yield edged down slightly but still remains nearly 10 basis points above the 3% psychological level, while the US 10-year yield rose by 2 basis points and is approaching 4.5%; the dollar strengthened by a quarter percent against the euro, with EURUSD moving toward 1.17.

In the regional FX market, the Czech koruna was flat against the euro, the zloty strengthened by 0.2%, while the forint weakened by 0.6% to around the 358.5 level after the MNB lowered the yield on its FX swap tender providing FX liquidity from 5.75% to 5.25% in the morning, down to the lower bound of the forint overnight interest rate corridor; instruments reflecting the expected policy rate path, including interest rate swaps and government bond yields, also fell, typically by around 10-15 basis points; reference yields published by the Government Debt Management Agency declined by 5-10 basis points, with the 10-year yield falling to 5.75%.

Today, the Government Debt Management Agency will offer three-, five-, and ten-year bonds in amounts of HUF 15 billion, HUF 20 billion, and HUF 20 billion, respectively.

Today's highlights

Asian indices were mixed this morning ahead of the meeting between the US and Chinese presidents, where discussions are expected to focus primarily on trade issues; Donald Trump arrived in Beijing accompanied by executives from major technology companies; Samsung’s share price rose after previously declining due to strike threats.

Today, UK and Polish GDP data will be released; in the United States, alongside the usual weekly initial jobless claims figures due on Thursday, retail sales and business inventory data will also be published.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more