OTP Morning Brief: Stock markets fell on Tuesday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

According to Trump, the Iran ceasefire has been put on life support, making investors skeptical about the swift success of peace negotiations. This triggered a broad-based fall across Western Europe, the CEE region, and overseas markets alike. U.S. sentiment was further weakened by higher-than-expected CPI, which also contributed to a rise in bond yields.The forint weakened back to the 357 level. Asian markets rose. Today, attention will be on the eurozone GDP release.

European stocks fell on Tuesday, while economic sentiment in Germany improved significantly

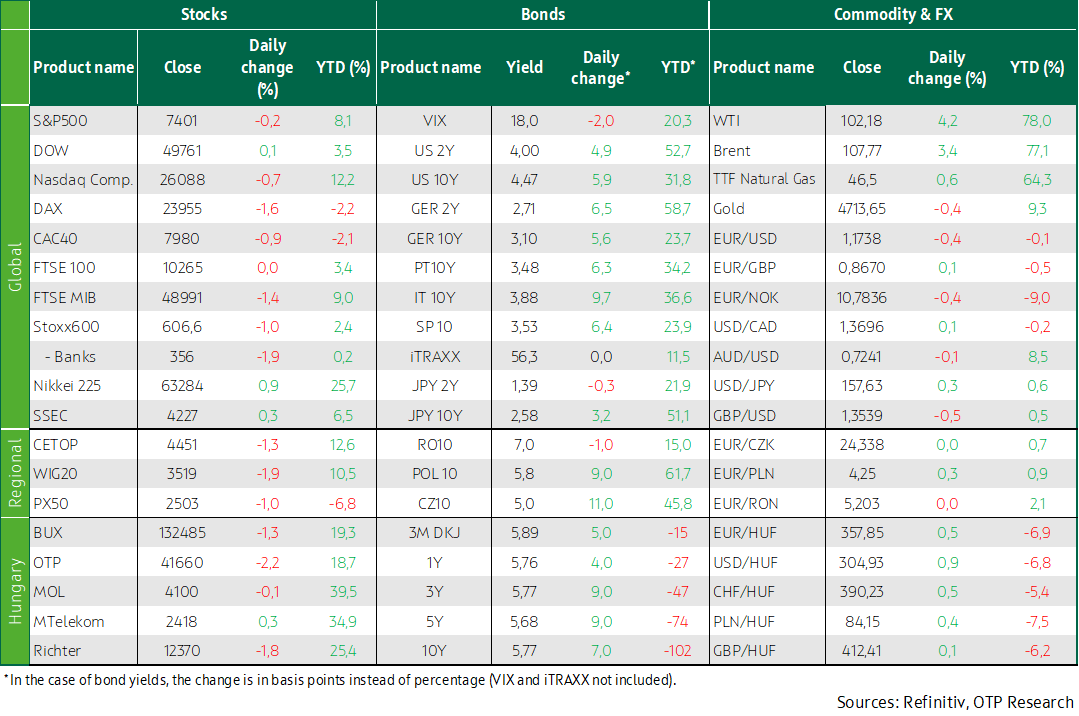

European equity markets closed broadly in the red on Tuesday: the STOXX 600 fell 1%, as fading hopes for a peace agreement between the United States and Iran pushed oil prices higher and weighed on risk sentiment, with all major regional indices ending lower; the Frankfurt DAX led the decline with a 1.6% fall, the CAC 40 dropped 0.9%, while the UK’s FTSE 100 remained flat, as ongoing disruptions to energy shipments through the Strait of Hormuz continue to keep European equities under pressure, leaving them below pre-war levels amid concerns over the economic impact of elevated crude oil prices; technology stocks led the losses with a 3.1% drop, tracking the sharp sell-off seen on Wall Street in AI-related stocks and chipmakers, while household goods rose 1.1%, outperforming other sectors, major UK banks including Barclays and Lloyds fell by 3% and 4% respectively, and Bayer shares climbed 3.6% after the German company reported better-than-expected quarterly operating results.

Germany’s ZEW Economic Sentiment Index rose by seven points to -10.2 in May 2026, surpassing market expectations of -19.8. Although the improvement signals a recovery in outlook, the index remains in negative territory, indicating that investors are still hoping for a swift resolution to the Iran conflict. At the same time, weak industrial production, rising energy prices, and CPI above 2% continue to weigh on the outlook.

Weak performance was also observed across the Central and Eastern European region, with the Czech index falling 1%, the Hungarian index declining 1.3%, and the Polish index dropping 1.9%. Among Hungarian blue chips, all except Magyar Telekom closed lower, with OTP leading the losses, falling 2.2%.

Middle East negotiations have stalled, while CPI is gradually rising due to the impact of the conflict

The S&P 500 and the Nasdaq closed lower on Tuesday, declining by 0.2% and 0.7% respectively, pulling back from near-record levels as higher-than-previous-month CPI data and growing uncertainty around the US–Iran ceasefire prompted investors to take profits as the exceptionally strong Q1 earnings season nears its end; weakness in technology stocks weighed most heavily on the Nasdaq, with the semiconductor index falling 3%, while healthcare stocks helped the Dow remain in slightly positive territory, supported by a 7.7% surge in Humana shares; GameStop shares fell 3.5% after eBay rejected the $56 billion takeover bid from the meme stock pioneer, meanwhile Under Armour shares dropped more than 17% after the sportswear company’s quarterly results and outlook disappointed investors.

US consumer prices rose 0.6% month-on-month in April (after 0.9% in March), while annual CPI accelerated to 3.8%, marking a three-year high, with the increase driven primarily by surging energy prices following the Iran conflict (accounting for more than 40% of the monthly CPI rise) and a pickup in food inflation; elevated price pressures pose a political risk for President Trump and Republicans ahead of the November midterm elections and reinforce market expectations that the Fed may keep interest rates unchanged through 2027.

Hopes for an Iran peace agreement faded further on Tuesday after Donald Trump stated that the ceasefire with Iran is “on life support,” following Tehran’s rejection of the US proposal to end the conflict and its insistence on demands that were firmly rejected by the US president; Iran is calling for an end to the war on all fronts, including Lebanon, where US ally Israel is fighting Iran-backed Hezbollah militants, while also asserting its sovereignty over the Strait of Hormuz, demanding compensation for war damages, and setting the lifting of the US naval blockade as a condition, among other demands; according to Trump, Iran’s response jeopardizes the sustainability of the ceasefire announced on April 7, which further pushed oil prices higher, with Brent crude rising 3% and WTI soaring 4.2%, leaving the former at $107.3 and the latter at $102.2 by Tuesday evening.

Bond yields rose, the dollar strengthened, and the forint weakened to the 357 level

Sentiment remained gloomy in developed bond markets yesterday as there has been no progress regarding the Iran war and the negative effects of tight oil supply are increasingly being felt; moreover, US CPI data came in 0.1 percentage points above expectations across the board, pushing US and European bond yields up by another 5 basis points, with the 10-year Treasury yield rising to 4.45%, the 10-year German yield climbing to 3.1%, and the Japanese yield soaring to 2.54%, close to a 30-year high, while the dollar strengthened by nearly half a percent against the euro, with EURUSD approaching the 1.175 level.

On the regional FX market, the Czech koruna remained flat against the euro, while the zloty weakened by 0.3% and the forint fell 0.5%, with the latter reaching the 357 level again; bond yields rose by 5–10 basis points from previous lows, with the 10-year yield at 5.8%, while, amid solid demand, the Government Debt Management Agency sold nearly 50% more three-month T-bills than the planned HUF 30 bn.

Today's highlights

Although Asian markets also opened lower, they managed to pare losses by the end of the day, with Japan’s Nikkei rising 0.9%, China’s SSEC gaining 0.3%, and South Korea’s Kospi climbing 2.0%.

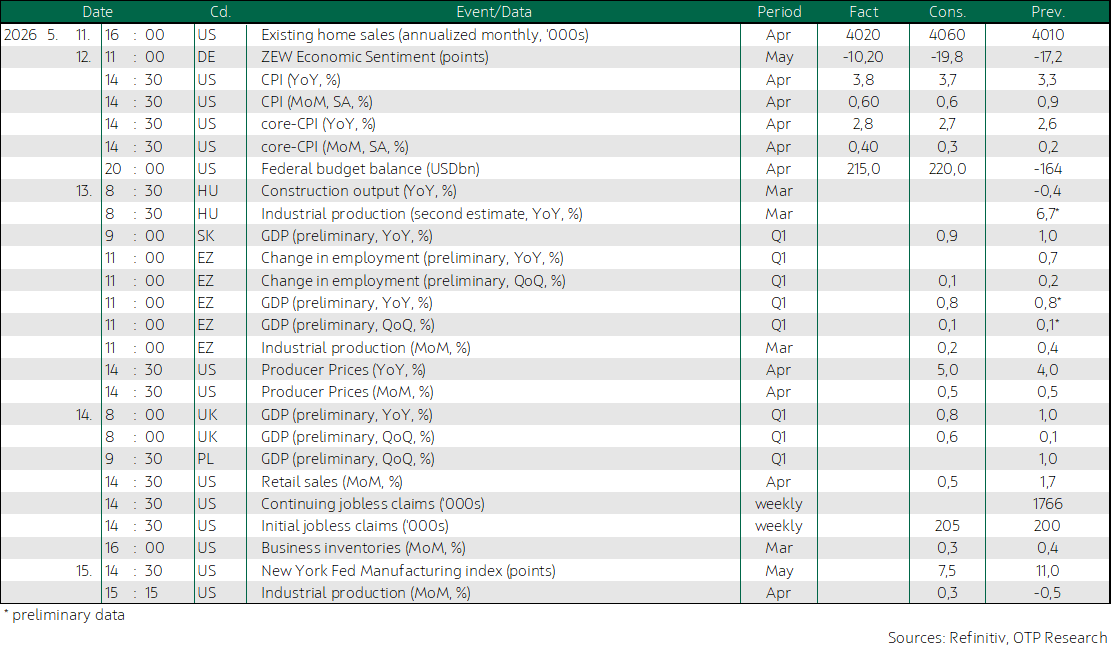

Today, eurozone GDP and industrial production data will be released, alongside domestic construction and industrial output figures, as well as US producer price index data; additionally, companies including Cisco, Siemens, and Allianz are set to report.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more