OTP Morning Brief: Oil prices continued to rise as talks between the US and Iran stalled

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

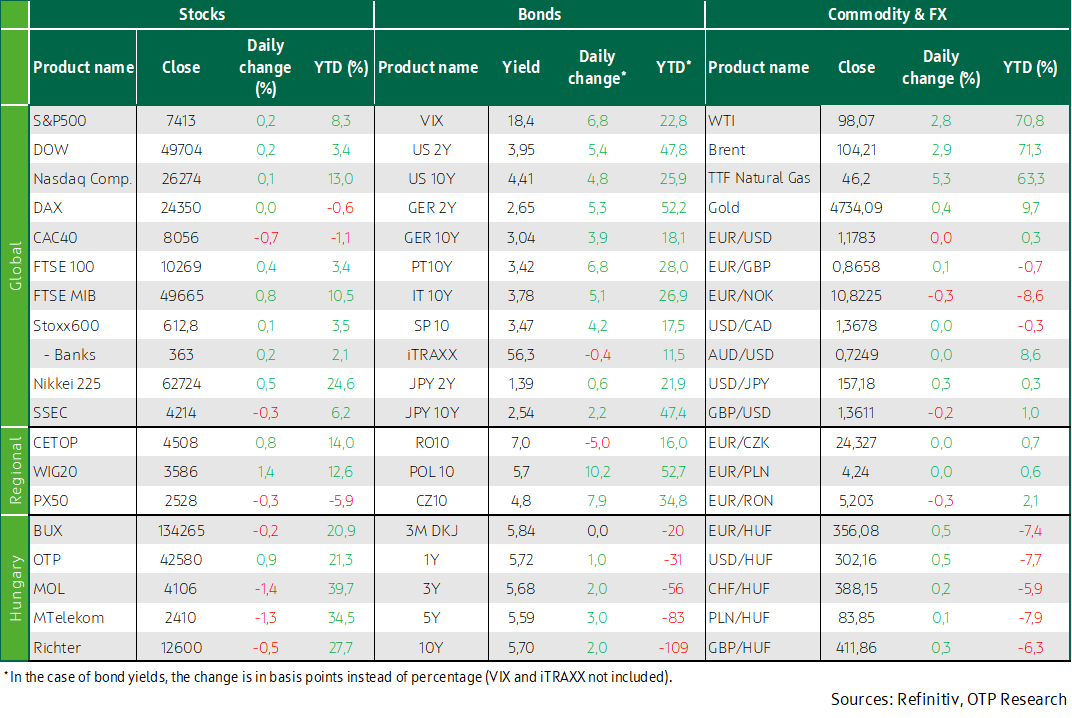

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

On Monday, crude oil prices rose by nearly 3%, while European benchmark natural gas prices gained 5%, after President Donald Trump rejected Iran’s response to the US peace proposal, pushing the talks into a stalemate. The Strait of Hormuz remains closed. Concerns over a prolonged conflict, combined with rising oil prices, are further reinforcing CPI-related fears. Nevertheless, major European and overseas equity indices closed slightly higher on Monday. The S&P 500 and the Nasdaq reached fresh all-time highs, with the AI-driven rise partially offsetting geopolitical uncertainty. In parallel with the rise in oil prices, bond market yields also rose. EUR/USD closed at 1.178. Hungarian long-term yields also rose slightly, while the forint weakened by 0.5%. In today’s trading, the Japanese 10-year yield rose to 2.54%—a level not seen since 1997—following the release of a hawkish summary from the BoJ’s latest meeting. Today, attention will be on Germany’s ZEW economic sentiment index, while in the US the focus will be on CPI data.

Major Western European indices closed near their Friday levels on Monday, as neither progress toward Middle East peace nor the reopening of the Strait moved closer

European equity markets were characterized by a cautious tone, as investors assessed geopolitical developments in the Middle East and the stalling of US–Iran negotiations. The Stoxx 600 index rose by 0.1% compared to the previous close, although sector performance was mixed. Defense stocks underperformed notably, as peace talks seen by markets as more constructive appeared to lose momentum and dismissive statements from the US administration increased uncertainty. Rheinmetall, Renk, Leonardo, and Hensoldt all posted marked declines, while investor sentiment was also affected by mixed signals regarding a potential end to the war in Ukraine.

Among the major Western European indices, the FTSE 100 rose by 0.3%, supported in part by global market optimism and rising oil prices. The DAX was broadly flat. By contrast, the CAC 40 declined by 0.6%, underperforming its regional peers. The divergent performances were driven primarily by sectoral differences and moves in individual stocks, while geopolitical news remained a key factor shaping investor decisions.

In the Central and Eastern European region, performance was mixed: Poland’s WIG20 rose by 1.4%, standing out among regional indices, while the BUX and the Czech PX50 both declined by 0.2%. The moves were driven partly by the international market backdrop and partly by stock-specific factors. Overall, domestic blue chips tilted the market in a more negative direction: although OTP rose by 0.9%, this was offset by a 1.3% decline in MOL and Magyar Telekom, as well as a 0.4% drop in Richter, together putting downward pressure on the BUX’s performance.

On Monday, the S&P 500 and the Nasdaq closed at fresh highs, although the deterioration in the geopolitical situation curbed the rise

US equity indices kicked off the week with modest gains, with the S&P 500 and the Nasdaq Composite reaching fresh all-time highs, although the advance was capped by worsening geopolitical conditions. The Dow and the S&P 500 both closed up 0.2%, while the Nasdaq rose by 0.1%. Despite the gains, overall sentiment remained subdued, as the likelihood of a US–Iran peace deal diminished after the two sides failed to move closer. The rise in crude oil prices continued to fuel CPI fears, while enthusiasm surrounding corporate profitability also faded as the earnings season nears its end. At the same time, optimism linked to artificial intelligence remained intact, providing some support amid elevated geopolitical uncertainty. Technology stocks, particularly chipmakers, once again outperformed, with the Philadelphia Semiconductor Index rising by 2.6%. Intel gained 3.6%, following its 14% surge on Friday on news of a preliminary chip manufacturing agreement with Apple, while rival Qualcomm jumped 8.4%, soaring to a record high. Among S&P 500 sector indices, energy posted the strongest rise (+2.6%), followed by materials (+1.4%), as well as industrials, IT, and utilities, each up around 1%. The biggest losers were communication services (-2.6%), with Netflix and Meta falling by 2%, Alphabet and Disney dropping by 3%, and AT&T, Comcast, and T-Mobile US each losing around 1%. Consumer staples also underperformed ahead of Tuesday’s CPI release and Thursday’s retail sales data: Walmart slipped 2%, Target and Dollar Tree declined by around 5%, Dollar General plunged nearly 8%, while Procter & Gamble and PepsiCo fell by 2% and 3%, respectively. Rising oil prices kept airline stocks under pressure, with shares falling by 3–4%.

The Q1 earnings season is nearing its end, with 440 S&P 500 companies having reported results so far. According to LSEG IBES data, 83% of these companies have beaten expectations. As of Friday, analysts estimate overall Q1 earnings growth for the S&P 500 at 28.6% year on year, nearly double the 14.4% Q1 growth estimate recorded on April 1.

Crude oil prices rose by 3–4% on Monday after President Donald Trump said that the ceasefire between the United States and Iran was “on life support” after rejecting Tehran’s latest peace proposal, further heightening concerns that the Strait of Hormuz could remain effectively closed for an extended period. According to reports, Iran has called on the United States to lift the maritime blockade and ease sanctions, while seeking to maintain control over the strategically important shipping route.

Crude oil prices continued to advance on Monday, while bond yields also moved higher. EUR/HUF closed at 356

After Donald Trump rejected the latest Iranian peace proposal, energy prices and bond yields rose again, while the dollar strengthened. Both WTI and Brent rose by nearly 3%, moving close to USD 98 and USD 105, respectively, while European gas prices rose by 5% to around EUR 47. US and European bond yields rose by 5 basis points, with the 10-year US Treasury yield once again exceeding 4.4% and the 10-year German yield rising to 3.05%. The dollar strengthened marginally against the euro, with EUR/USD continuing to fluctuate below 1.18.

Hungarian markets, the strong rally of recent weeks was followed by a mild correction. Amid a weaker global backdrop, the forint depreciated by 0.5% against the euro from its strongest level of the past four years, slipping to 356, while the Czech koruna and the Polish zloty remained broadly stable. Bond yields rose by 2–3 basis points, with the 10-year yield at 5.7%, still hovering around its lowest level of the past two and a half years.

Today's highlights

Sentiment was mixed across Asian equity markets early Tuesday: Japanese indices continued to rise, with the Nikkei up 0.6%, while the Hang Seng also strengthened. By contrast, Chinese and Korean benchmarks traded in negative territory, with the Kospi plunging by 2.6% amid a sell-off in AI-related stocks. JPMorgan nonetheless expects further strong upside in the Kospi after the index has already rallied by 80% this year. In Asian bond markets, the Japanese 10-year yield rose to 2.54%, a level not seen in 29 years, following the release of a hawkish summary from the BoJ’s latest meeting. According to the minutes from last month’s meeting published today, several policymakers in April saw the need for an earlier rate hike, while one member indicated that the pace of tightening could accelerate should CPI risks intensify.

Equity index futures point to a negative open today for both major European and US indices.

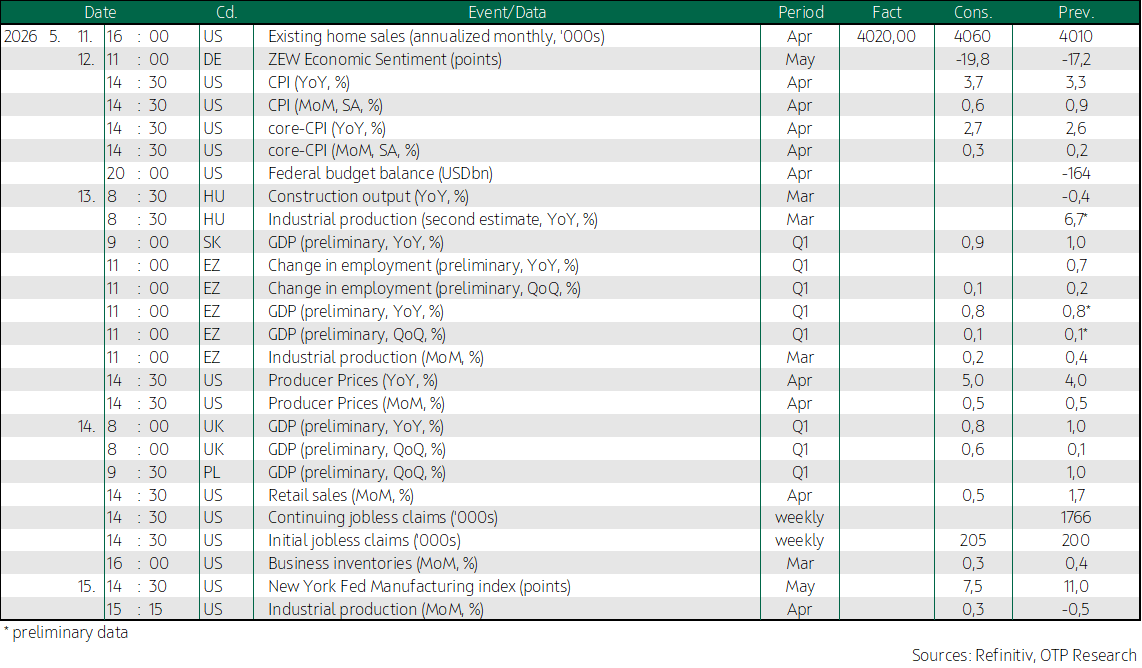

Today, attention will be on US CPI data for April, which is expected to point to stronger price pressures. In March, the pace of price increases accelerated at its fastest rate in nearly four years (+0.9% m/m), driven primarily by surging energy prices following the outbreak of the Iran-related conflict.

In Germany, the ZEW economic sentiment index will be released today and is expected to have deteriorated further. In Europe, companies reporting today include Munich Re, KBC, Bayer, and Thyssenkrupp.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more