OTP Morning Brief: Oil prices rose again after a breakthrough on a potential US–Iran agreement failed to materialize

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Leading Western European indices declined on Trump’s tariff threats. Regional stock markets, including the BUX, also closed in negative territory. Domestically, the new parliament was sworn in on Saturday, and Péter Magyar was elected prime minister. Earlier, on Friday, the forint strengthened sharply and yields continued to decline. Sentiment was positive in overseas markets, with the S&P and the Nasdaq closing at new highs, supported by favorable earnings reports and strong labor market data. Trump rejected Iran’s response to the US framework agreement over the weekend, pushing oil prices back into sharp gains by Monday morning. This week, attention in Hungary will focus on construction and industrial output data, while from the euro area GDP, employment, and industrial production figures are due. From overseas, CPI and monthly activity indicators will be in focus.

Leading Western European indices fell on Trump’s tariff threats; the BUX also ended the day in negative territory

Western European equity markets fell on Friday after concerns resurfaced over tariff threats from US President Donald Trump. The pan-European STOXX 600 index declined by 0.7%, with most sectors posting losses. Major markets in London, Paris, Frankfurt, and Milan all retreated. Trump criticized the European Union for what he described as a failure to comply with a previous trade agreement and warned that if the EU does not accept the agreement by July 4, 2026, the US would significantly raise tariffs imposed on the bloc.

Among individual stocks, Deutsche Bank fell 3.9% despite reporting operating profit of EUR 1.36 billion in Q1. Market sentiment was weighed down by uncertainty surrounding banks, linked to UniCredit’s acquisition plans. Defense stocks also underperformed: Rheinmetall declined 9.2%, while Leonardo slid 3.2%, amid geopolitical tensions and comments from Trump. At the sector level, only information technology and telecommunications managed to post gains, while all other sectors closed in negative territory.

Most Western European markets ended the week close to flat, with only the Italian stock market managing to rise by more than 2%, while the UK’s FTSE closed the week down 1.3%.

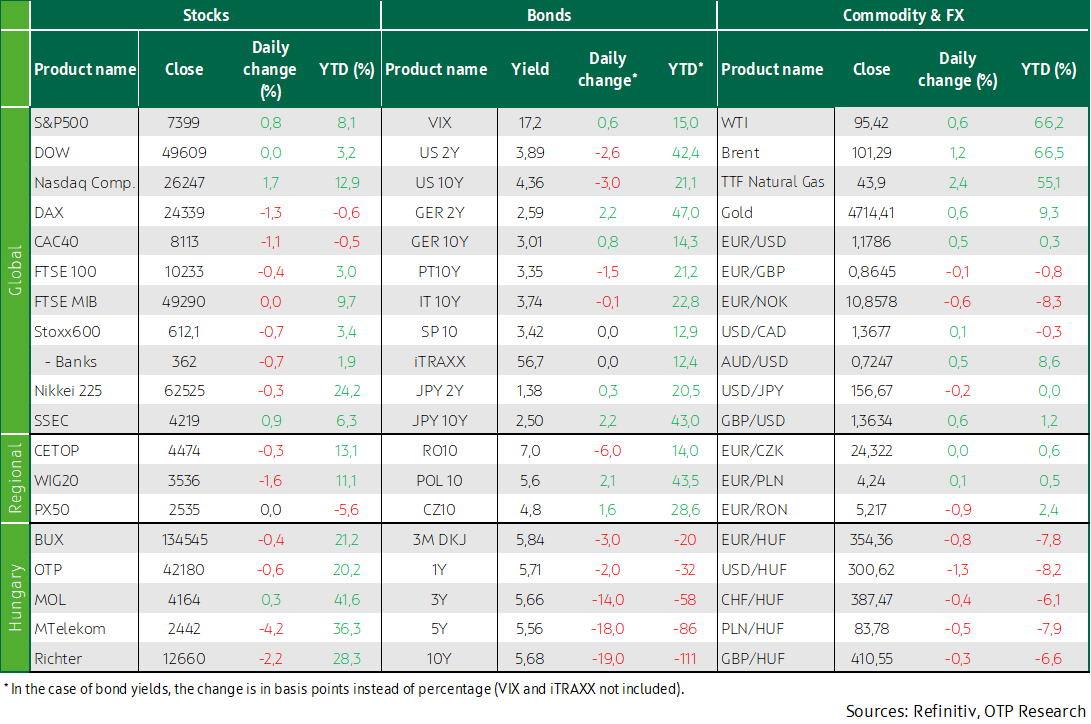

Among Hungarian blue chips, only MOL managed to post gains on Friday, edging 0.3% higher after two days of sharp declines. The day’s biggest loser was Magyar Telekom, which fell 4.2% for technical reasons, as Thursday was the last day the stock traded with dividend entitlement. Richter closed the session down 2.2%, while OTP declined 0.6%, leaving the BUX 0.4% lower on the day. Over the week as a whole, the domestic stock market ended with a modest 0.6% gain, led by OTP and MOL. Regional stock markets also closed in negative territory on Friday: the CETOP fell 0.3%, the WIG20 dropped 1.6%, while the Czech market was closed.

The S&P and the Nasdaq closed at new highs, supported by favorable earnings reports and strong labor market data

The S&P 500 and the Nasdaq once again reached record highs on Friday, driven by gains in Nvidia, SanDisk, and other AI-related stocks, while on the macro front a stronger-than-expected employment report pointed to the resilience of the labor market.

Nvidia gained 1.8%, while memory and data-storage solution providers Micron Technology and SanDisk both soared more than 15%, supported by expectations of strong demand driven by the rapid build-out of AI data centers. The Philadelphia SE Semiconductor index also posted sharp gains and is now up 55% so far in the second quarter. The S&P 500 rose 0.8%, the Nasdaq advanced 1.7%, while the Dow Jones Industrial Average was flat. The S&P 500 technology sector surged 2.7%, while utilities declined 0.9%. The S&P 500 and the Nasdaq have now risen for six consecutive weeks, marking their longest winning streak since October 2024. The Dow recorded its second consecutive weekly gain. Year to date, the S&P 500 is up 8% in 2026, while the Nasdaq has posted a 13% rally.

According to LSEG, 83% of the 440 S&P 500 companies that have reported Q1 results so far have beaten analysts’ earnings expectations, compared with a long-term average of around 67%.

There were also some disappointing results. Cloudflare shares plunged 24% after the cloud services provider announced plans to cut around 20% of its workforce and guided Q2 revenue slightly below Wall Street expectations. Advertising company The Trade Desk slipped 1.8% after forecasting Q2 revenue below the analyst consensus. Online travel platform Expedia weakened 9% after warning that the Middle East conflict is dampening demand.

Optimism surrounding earnings expectations helped investors look past renewed attacks escalating between US and Iranian forces in the Persian Gulf. Brent crude prices rose back above USD 100 per barrel as hopes for a swift resolution of the Middle East conflict faded, along with expectations for the gradual reopening of the key oil and liquefied natural gas shipping route, the Strait of Hormuz. The US said it expects a response from Tehran later on Friday to its latest proposal.

Domestic yields continued to fall and the forint advanced; the new parliament was formed and the new prime minister was sworn in; meanwhile, there was no material movement in international bond yields on Friday

Investors also focused on the Middle East last week, as confidence in a near-term peace deal drove energy prices, rate expectations, and bond yields. While the Strait of Hormuz remains closed, confidence in a potential near-term settlement strengthened again around mid-week after reports suggested that a US–Iran agreement could be reached with Pakistani mediation. As a result, oil prices—having reached rarely seen highs on Monday—fell by nearly 15% on Tuesday and Wednesday and, despite a rebound toward the end of the week, ultimately closed almost 10% lower than the previous week. Among last week’s economic releases, US labor market data were the most important, with most indicators—including non-farm payrolls, the unemployment rate, wage dynamics, and initial jobless claims—painting a stable picture; however, labor costs and productivity increased less than expected in Q1. In Europe, retail sales expanded by a stronger-than-expected 1.2%. Over the course of the week, policy-rate paths for both the dollar and the euro shifted slightly lower, with markets continuing to expect unchanged rates from the Fed this year, while pricing in at least two—and potentially three—rate hikes from the ECB. Bond yields largely tracked oil prices: the US 10-year yield rose from 4.38% at the start of the week to 4.45%, before easing back to 4.39%, while the German 10-year yield rose to 3.1% before retreating to the top of its post-pandemic trading range around 3.0%. The dollar ultimately weakened, with EURUSD strengthening by 0.5% both on Friday and over the week, approaching the 1.178 level.

In regional and domestic markets, currencies strengthened, with the Czech koruna appreciating marginally, while the forint rose by more than 2% over the week—more than 0.5% of that on Friday—pushing EUR/HUF down to around 354, a level not seen since 2021. Following previously strong industrial production data, March retail sales figures also pointed to a meaningful pickup in activity. In addition, Bloomberg reported comments from Zoltán Kurali, Deputy Governor of the NBH, saying that a strong forint increases the central bank’s room for maneuver and that a rate cut could be put on the Monetary Council’s agenda as early as June, alongside the new CPI forecast. As a result, rate-cut expectations strengthened, with markets pricing in one cut this year and two next year, implying policy rates of roughly 6.0% and 5.5%, respectively. April CPI, published on Friday, increased to 2.1% from 1.8% previously—broadly in line with our expectations but slightly above market consensus—while underlying CPI dynamics remained subdued. Against this backdrop, the bond market rally driven by the change of government and expectations surrounding euro adoption continued, with ÁKK reference yields falling to their lowest levels since 2024 after dropping 15–20 basis points on Friday and 35–40 basis points over the week as a whole, bringing the 10-year yield below 5.7%. Domestically, the new parliament was formed on Saturday, and Péter Magyar was elected prime minister.

Today's highlights

Iran’s response to the US framework agreement proposal arrived over the weekend, which Trump described as completely unacceptable. As a result, oil prices rose further by this morning, with WTI moving into a nearly 5% gain. Asian equity markets are mixed: the Nikkei is down 0.3%, while the SSEC is up 0.9%. European equity futures are trading slightly higher, while their US counterparts are showing losses of one to two tenths of a percent.

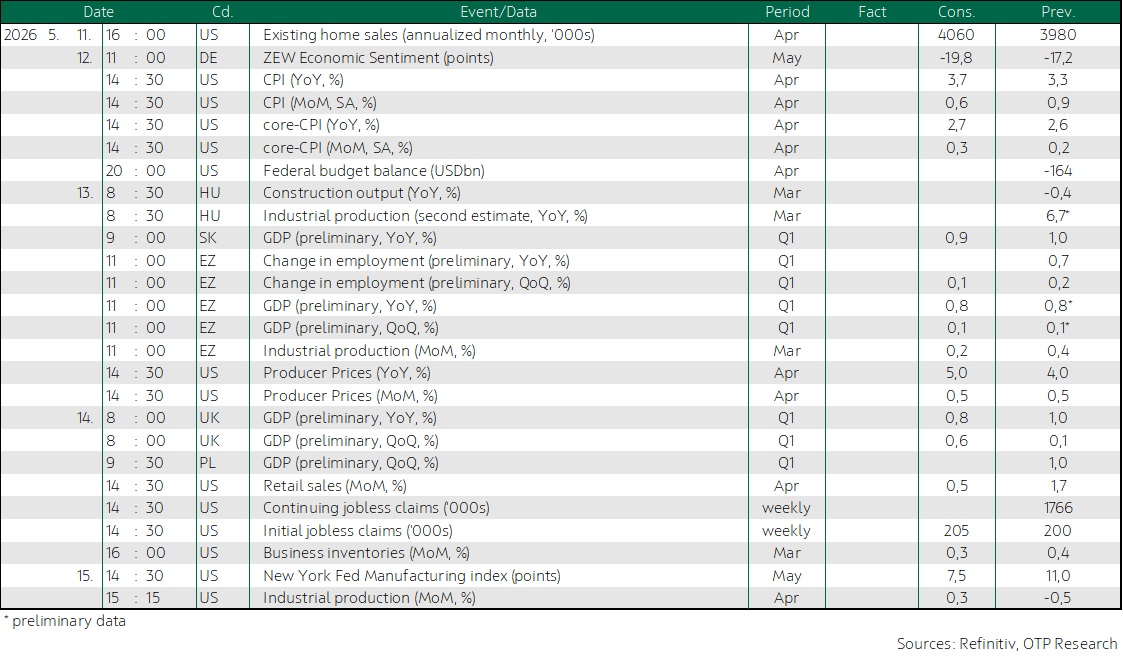

This week, the euro area will release its second GDP estimate, along with employment and industrial production data. Based on information available so far, we do not expect a material revision to GDP; however, it is worth noting that the reported 0.1% growth rate was rounded from 0.147%, meaning a slight upward revision could produce a marginally more favorable figure. It is also important to highlight that, based on a more detailed breakdown, the flash estimate was overall less adverse than it may have appeared at first glance. Excluding Ireland’s typically highly volatile GDP reading (-2%), euro-area growth amounts to 0.2% quarter on quarter and 1.1% year on year. Employment growth continues to appear stable—at least insofar as the very low unemployment rate observed through March genuinely reflects a tight labor market rather than data being distorted by a contraction in labor supply during Q1. In this context, the Q1 employment statistics to be published next week will be of particular importance.

The US April CPI report will be released on Tuesday and is almost certain to show stronger price pressures. In March, the pace of price increases accelerated at the fastest rate in nearly four years (+0.9% month on month), driven primarily by surging energy prices following the Iran war. Beyond CPI, a range of April activity indicators will also be published, shedding light on how the US economy started Q2, at a time when the Iran war had already been ongoing for a month, CPI pressures were intensifying, and uncertainty was increasing.

In Hungary, construction output data will be released on Tuesday, and the detailed industrial production figures will shed light on what drove the 3.1% month-on-month rise in industrial output.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more