OTP Morning Brief: Markets rose and oil prices fell on news of a near US–Iran framework agreement

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

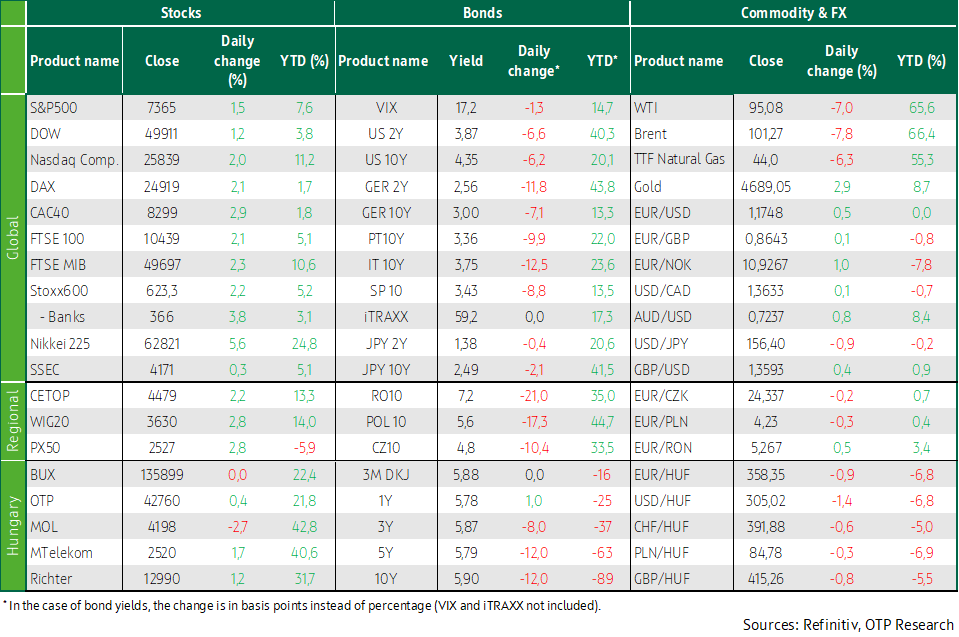

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Western European markets rallied on news of a potential near-term US–Iran agreement, while the BUX was flat due to a sharp decline in Mol shares. Brent crude finished trading down around 7% on news that the US and Iran are close to reaching a 14-point framework agreement aimed at ending the war. In the US, both the Nasdaq and the S&P closed at new highs, supported by developments related to Iran as well as a favorable earnings report from AMD. According to ADP, employment growth in April was stronger than expected, while one Fed policymaker emphasized CPI risks yesterday, a message consistent with keeping interest rates at restrictive levels for longer. Expectations for central bank tightening eased in response to the drop in oil prices. Domestically, the forint closed below 360, while the 10-year reference yield fell back below 6%. Today, attention will be focused on German industrial orders, domestic and euro-area retail sales data, the Czech rate decision, and productivity and labor market data from the US, while the earnings season continues to gather pace.

Western European markets rallied on news of a potential near-term US–Iran agreement, while the BUX was flat due to a sharp decline in Mol shares

Western European stock markets rose sharply on Wednesday after reports of a potential peace agreement between Washington and Tehran boosted risk appetite and drove oil prices sharply lower, while positive corporate earnings also added to optimism.

The pan-European STOXX 600 index closed up 2.2% at 623.25 points, its strongest level since April 17. Major regional markets followed the rally as well: France’s CAC 40 led the gains, soaring 2.9%, while the Italian benchmark index rose 2.3%, approaching its highest level since 2000.

Iran said it is seriously reviewing a new US proposal after reports emerged that the parties are close to signing a single-page agreement aimed at ending the conflict in the Persian Gulf. Brent prices fell by nearly 7%, making the energy sector the only major STOXX sector to decline, down 2.5%.

Lower oil prices also supported the oil-price-sensitive travel sector, which rose 5.8%, marking the strongest sectoral gain within the index. The banking sector and industrial stocks posted gains of 3.8% and 3.2%, respectively, and were the largest contributors to Wednesday’s performance of the European benchmark index. Defense stocks rose 4.7%. Italy’s Leonardo gained 5% after reporting stronger Q1 results, while Norway’s Kongsberg also soared 5% after its quarterly order intake more than doubled. Demant skyrocketed 13.3%, its largest one-day gain since October 2008, after the Danish hearing-aid maker beat expectations for quarterly revenue growth. Novo Nordisk rose 2.5% after the Wegovy maker raised its full-year outlook and reported better-than-expected Q1 profit. BMW advanced 5.4% after the German automaker maintained its full-year guidance despite a sharp decline in quarterly pre-tax earnings. The automotive index rose 4.2%. Diageo jumped 6.4% after the world’s largest spirits producer delivered unexpected growth in quarterly organic revenue. On the macro front, final euro-area PMI data showed that the services sector contracted in April for the first time in nearly a year, reflecting weakening demand linked to the Middle East war.

The positive sentiment spilled over to the region as well, with the CETOP up 2.2%, while both the WIG20 and the PX50 rose 2.8%. The BUX, however, underperformed and was flat: although shares of Magyar Telekom, Richter, and OTP gained among the blue chips, a 2.7% decline in Mol weighed on the index. The latter tracked the broader decline in the European energy sector.

US stock markets also pushed higher, with the S&P 500 and the Nasdaq closing at record highs

US markets also posted strong gains. The S&P 500 and the Nasdaq climbed to record highs on Wednesday, as signs pointing to a potential easing of the Middle East conflict, together with strong results from Advanced Micro Devices, triggered a rally in chipmakers and other AI-related stocks. AMD shares soared nearly 19% to a record high after the company issued better-than-expected quarterly revenue guidance, driven by strong demand for data-center chips. Rival Intel’s shares rose 4.5%, while the PHLX semiconductor index also rose 4.5%, lifting its 2026 year-to-date performance to a gain of around 62%.

Meanwhile, S&P 500 companies are on track for their strongest profit growth in more than four years. According to LSEG data, more than 80% of S&P 500 companies that had reported by May 1 beat analysts’ earnings expectations. The S&P 500 rose 1.5%, the Nasdaq rose 2.0%, while the Dow Jones Industrial Average gained 1.2%. Nine of the S&P 500’s eleven sector indices advanced, led by industrials, which rose 2.6%, followed by the information technology sector with a 2.56% increase.

According to ADP, US private-sector employment expanded by the largest amount in 15 months in April, suggesting that the labor market has remained resilient even as the conflict involving Iran weighs on the economic outlook. St. Louis Fed President Alberto Musalem said that the risks to monetary policy have shifted toward higher CPI, which could warrant keeping interest rates unchanged for some time, alongside what appears to be a stable labor market.

Among corporate news, Corning stood out, soaring 12% after announcing that it will expand US manufacturing of optical connectivity products used in AI data centers in cooperation with Nvidia. Nvidia shares rose nearly 6%. Hut 8 skyrocketed 35% after the AI data-center developer signed a 15-year, USD 9.8 billion lease agreement for its Beacon Point data-center campus in Texas. Walt Disney gained 7.5% after the entertainment group beat Q2 expectations and investors received insight into CEO Josh D’Amaro’s growth strategy. Uber Technologies advanced 8.5% after the ride-hailing and delivery platform guided to strong Q2 bookings. Super Micro surged 24.5% after issuing stronger-than-expected guidance for Q4 revenue and adjusted earnings.

Developed-market and domestic long-term yields eased further, while the forint strengthened below 360against the euro

Following Tuesday’s 4% drop in oil prices, an additional decline of around 7% was recorded yesterday. Against this more optimistic backdrop, expectations regarding the policy rate paths of major central banks were pushed lower, and long-term yields fell by close to 6–7 basis points. The 10-year US Treasury yield declined to 4.35%, while the German 10-year yield eased to 3.0%. The dollar weakened, with the euro strengthening by around 0.5% to 1.175.

Regional currencies continued to strengthen: the Czech koruna appreciated by 0.2%, the zloty by 0.43%, while the forint gained nearly 1% further against the euro, with EUR/HUF closing near 358, a level not seen since early 2022. Following a temporary correction on Tuesday, domestic bond yields dropped sharply again, declining by 10–15 basis points, with the 10-year benchmark yield falling to around 5.9%. The yield curve remains extremely flat, with reference yields clustering broadly between 5.8% and 6.0%.

At the Government Debt Management Agency’s (ÁKK) six-month Treasury bill (DKJ) auction, demand was moderate, yet the debt manager sold roughly one-third more than the planned HUF 30 billion, at an average yield of 5.92%. Interest was strong at the switch auction, where investors could exchange bonds maturing this year and next for the 2033/C and 2034/A series—each offered in amounts of HUF 15 billion. In total, HUF 75 billion worth of the two bonds was swapped at yield levels below 5.9%.

Today's highlights

Asian equity markets also climbed to record highs on Thursday, while the US dollar weakened and oil prices attempted to recover from the steep losses recorded over the previous two days.

Japan’s Nikkei, returning after an extended holiday break, crossed the 62,000-point level for the first time, catching up with the AI-driven rally fueled by strong corporate earnings that has also propelled South Korean and Taiwanese equity markets to record highs.

The MSCI Asia-Pacific equity index excluding Japan rose 1%, reaching another all-time high. The index has gained a cumulative 7% so far this week. China’s SSEC was modestly higher, up 0.3%.

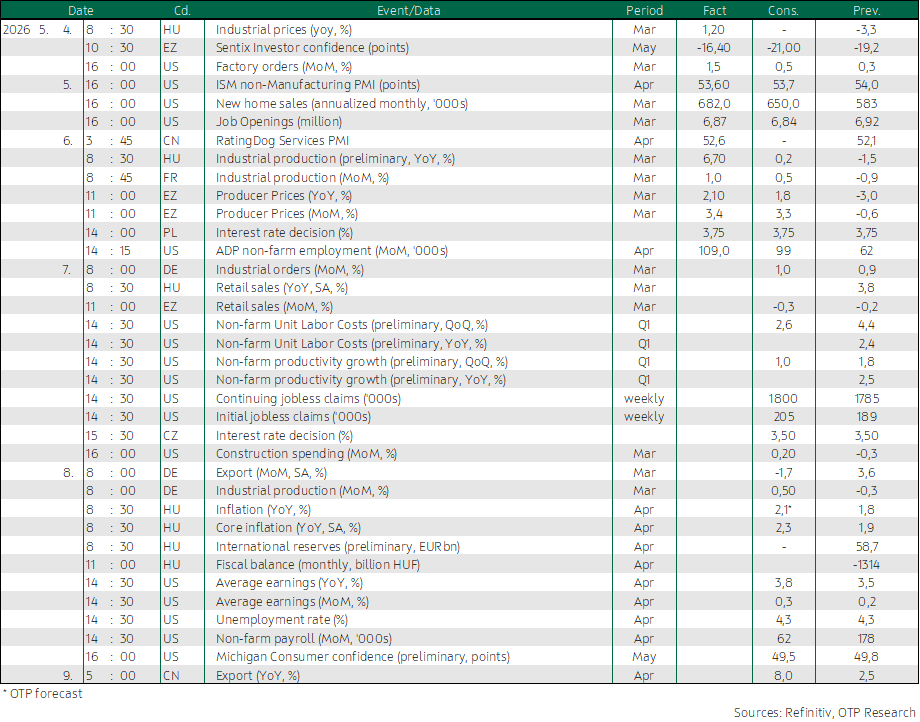

Today, German industrial orders and domestic as well as euro-area retail sales data are due, while Q1 productivity and unit labor cost figures from the US could be market-moving. In the region, the Czech central bank’s rate decision may also draw attention. The earnings season continues to gather momentum, with companies such as Shell, McDonald’s, and Rheinmetall reporting today.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more