OTP Morning Brief: Declining oil prices and the strong performance of the technology sector provided momentum to the markets on Tuesday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

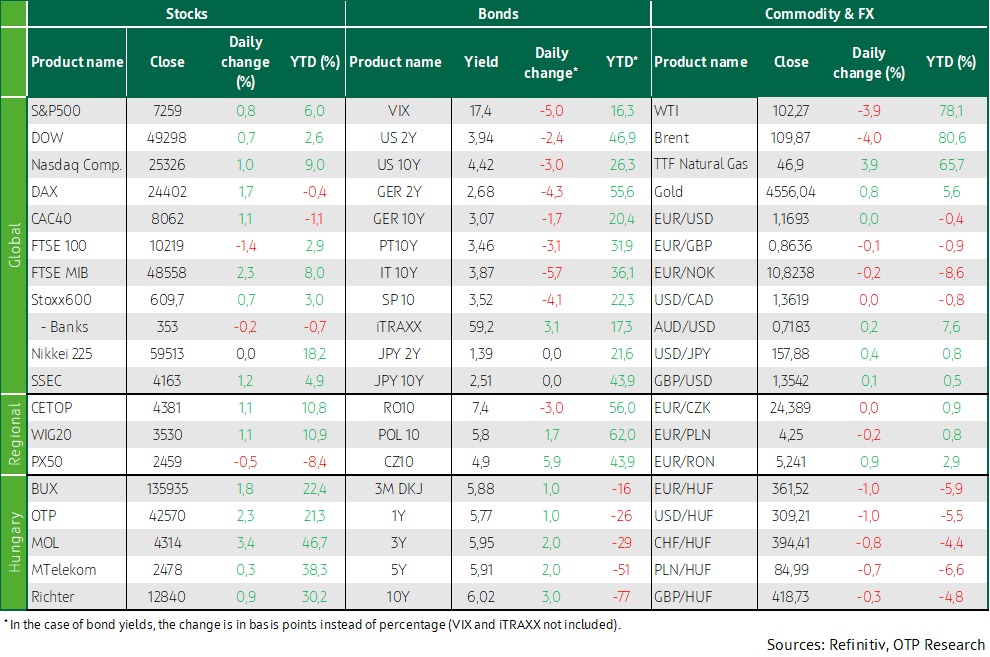

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Except for the FTSE100 in the UK, the leading European indices rose. Stock markets in the CEE region closed mixed, while the BUX went up. The NASDAQ and the S&P 500 closed at new all-time highs, driven by the tech sector’s rally. The US-led escort of ships stranded in the Strait of Hormuz has begun, but the operation is paused today. The United States confirmed that the previously reached Middle East ceasefire remains in place. Crude oil prices fell. Yields in developed markets moderated, and the euro strengthened slightly against the dollar. Domestic bond yields rose by a few basis points. The forint continued to strengthen against the euro. Today, we are focusing on domestic and French industrial production data, the eurozone PPI, the ADP Institute’s labor market data, and the Polish central bank’s interest rate decision meeting, while the earnings season continues in full swing.

Except the FTSE100, major European stock markets rose; the BUX closed higher

After Monday's losses, most major European indices rose on Tuesday; the gains were driven by earnings season results and falling oil prices. The pan-European Stoxx 600 rose by 0.7%, with technology proving to be the clear frontrunner among its mostly rising sector indices, riding on the sector’s strong performance on Wall Street. Chipmakers such as ASML and ASMI contributed most to the technology sector’s 2.4% gain. Among corporate news, HSBC’s (-5.9%) plunge is worth noting, which dragged the British FTSE 100 (-1.4%) into the red; the bank’s stock fell after it reported an unexpected $400 million loss related to a British fraud case, resulting in first-quarter earnings falling below expectations. Among the flash reports, UniCredit’s is worth highlighting, as it climbed 5.9% to a record close following record-high profits and an upward revision to its annual forecast; the bank also made a takeover offer for Commerzbank. Rheinmetall rose 3.4% despite preliminary results showing that quarterly revenue missed expectations. Translated with DeepL.com (free version)

Equity markets in the CEE region closed mixed yesterday; the Czech PX 50 fell for a second consecutive day after Monday, while Poland’s WIG20 and Hungary’s BUX were able to rise. Among domestic blue chips, OTP posted the strongest performance, closing more than 2% higher.

Péter Magyar, the incoming prime minister, posted on social media that he had learned that, according to the Orbán government’s own projections, the budget deficit would rise to 6.8% of GDP this year.

European TTF natural gas prices rose to around EUR 47/MWh.

The technology sector rallied, with the S&P 500 and the NASDAQ closing at all-time highs

The S&P 500 and the NASDAQ closed at new all-time highs amid a surge led by companies linked to artificial intelligence and chipmakers. All S&P sector indices were able to rise. Although there has been no progress toward resolving the Middle East conflict and tensions remain high in the Hormuz Strait, the United States reaffirmed that it still considers the previous ceasefire agreement to be in force, easing concerns over potential escalation around the strait. Among individual stocks, Intel jumped 12.9% on news of a chip manufacturing cooperation linked to Apple, while AMD rose 4% ahead of its earnings report, where the market expects significant revenue growth. The PHLX Semiconductor Index rose 4.2% to a new record, bringing its year-to-date gain to 55%. In addition to technology stocks, several individual names – including DuPont and Pinterest – also soared on the back of better-than-expected outlooks and results.

The dumping of US labor market data has begun, with the latest figures reflecting a slower-than-expected cooling of the labor market; the number of job openings fell less than expected, while the number of workers voluntarily leaving their jobs—typically for higher pay—rose.

Brent crude fell by 4% and WTI by 3% on the first day of the rescue operation for ships stranded in the Strait of Hormuz, but prices for both remained above $100 per barrel. Although conflicting reports have emerged from the strait, it has been confirmed that some ships have already left the strait without incident, accompanied by a U.S. escort. However, Donald Trump has since announced the pause of the operation, named "Project Freedom," citing progress in diplomatic negotiations.

Long-term developed market yields declined, while the forint continued to strengthen against the euro

Alongside falling oil prices, bond yields edged lower and the euro strengthened marginally. The US ten-year yield fell by 2 basis points to a still near one-year high of 4.4%, while the ten-year German yield declined by a similar magnitude to around 3.05%. The euro strengthened slightly against the US dollar, trading near 1.17.

In a positive market environment, regional currencies strengthened, with the Czech koruna rising marginally, the zloty up 0.2%, and the forint rising by 1% against the euro to the 361 level. Domestic bond yields increased by 2–3 basis points, reacting with some delay to Monday’s rise in developed market yields. At yesterday’s three-month T-bill auction, the Debt Management Agency sold one-third more than the planned HUF 30bn of three-month T-bills amid solid demand, at an average yield of 5.94%.

Today's highlights

Sentiment across Asia-Pacific equity markets was broadly positive, with South Korea’s Kospi climbing to another record high as it rode the wave generated by Wall Street the previous day. Samsung jumped more than 15% to reach a new all-time high, pushing its market capitalization above USD 1 trillion. Japanese equity markets remained closed due to a public holiday.

Equity index futures are mostly pointing to a positive open in both Europe and overseas markets.

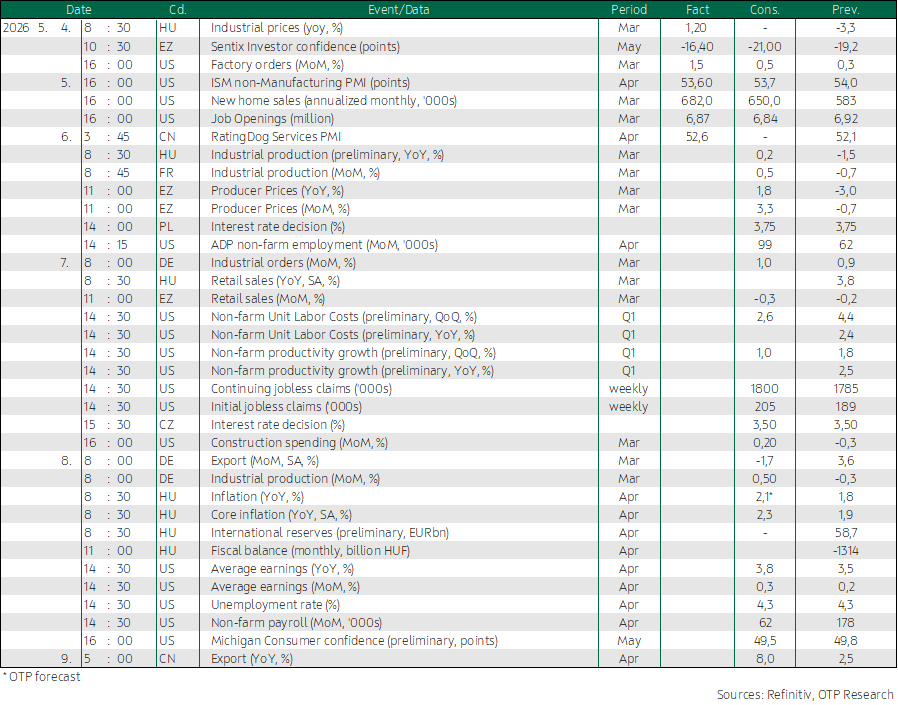

Today, the Debt Management Agency is offering six-month T-bills, with an announced volume of HUF 30bn. In addition, at the switch auction, investors can acquire HUF 15bn each of the 2033/C and 2034/A bonds in exchange for securities maturing this year and next year.

The Hungarian Central Statistical Office (KSH) will publish March industrial production data today, shedding light on how much domestic industry may have contributed to the better-than-expected Q1 GDP performance.

Industrial production data will also be released from France, which is expected to show a meaningful rebound after the sharp decline seen in February. Based on purchasing managers’ indices, the expansion in output is partly due to manufacturing firms already beginning to produce for inventories in March, amid concerns over rising and tight energy prices.

Eurostat will publish the March producer price index, which is expected to already show a marked impact from rising energy prices.

In the United States, the ADP institute will release its April labor market data ahead of the official statistics due on Friday.

The National Bank of Poland is holding a rate-setting meeting, at which rates are expected to remain unchanged at the current 3.75%.

The earnings season continues, with results due from Uber, Walt Disney and CVS, among others.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more