OTP Morning Brief: The Middle East conflict continued to escalate, deteriorating investor sentiment

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

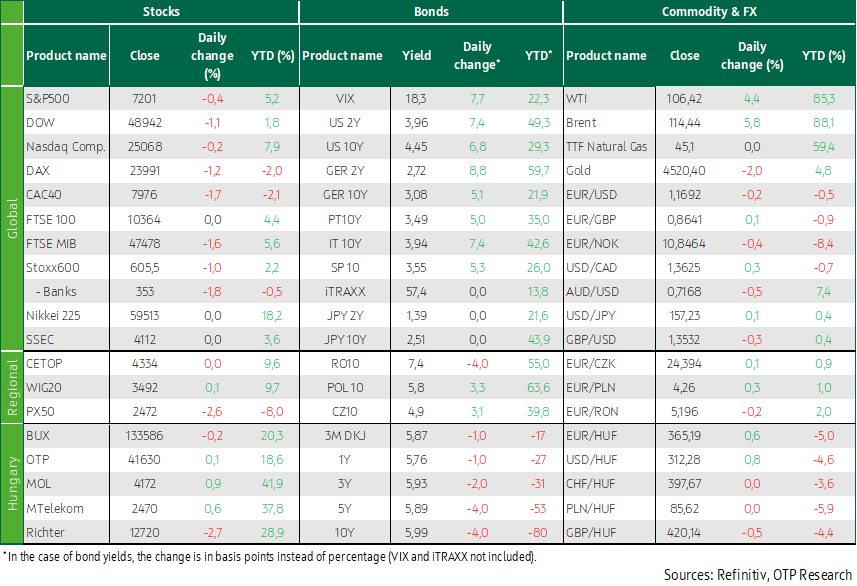

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Risk aversion intensified across global markets after the conflict in the Middle East escalated again, oil prices surged, and Donald Trump once more threatened tariff hikes against European automakers, triggering broad-based declines in European equities. At the same time, the Sentix sentiment index came in stronger than expected in May. US equity markets were also under pressure, bond yields edged higher, the dollar strengthened, and regional currencies weakened (with EUR/HUF moving above 365). Asian markets also declined.

Today, attention will be focused on US economic data.

European markets declined amid Middle East uncertainties, while European automakers once again came under pressure due to Trump’s tariffs

European equities fell again on Monday as fighting in the Middle East intensified once more, pushing oil prices sharply higher, while investors assessed the prospect of consecutive ECB rate hikes this year. Among the major indices, the CAC 40 declined 1.7%, the DAX fell 1.6%, while the FTSE slipped just 0.1%. As a result, the pan-European STOXX 600 index closed 1.0% lower, with most sectors ending in negative territory. Euro-area bank stocks suffered particularly heavy losses, dropping 2.7%, marking their largest one-day decline in more than six weeks. Automaker shares weakened 2.1% after US President Donald Trump announced late on Friday that tariffs on cars and trucks imported from the European Union would be raised to 25% this week from the previously agreed 15%, citing the EU’s alleged failure to meet its commitments. The EU has rejected the US accusations, while a majority of member states—particularly Germany—are urging the bloc to swiftly finalize and implement its own legislative measures, namely cutting US industrial import tariffs, in order to avoid further punitive actions. On the back of the news, shares of major manufacturers were sold off, including Mercedes (-3.4%), Volkswagen (-2.8%), and BMW (-2.4%). Among individual stocks, Thyssenkrupp fell 1.8% after the German industrial group suspended talks on the sale of its steel business to India’s Jindal Steel.

The Sentix euro-area investor sentiment index improved more than expected in May (-16.4 points versus -21.0 expected, after -19.2 in April), suggesting that markets are pricing in fewer adverse effects from the Iranian conflict. At the same time, Germany remained particularly weak (-30.9 points after -27.7 in April), and although both the euro area expectations and current conditions indices rose, they remain in negative territory, indicating that recession risks persist.

CEE equity indices painted a mixed picture: the PX 50 plunged 2.6%, the BUX posted a more modest 0.2% decline, while the WIG 20 edged slightly higher. Among Hungarian blue chips, Richter’s 2.7% drop and Mol’s 0.9% gain stood out, the latter supported by higher oil prices. According to data from the Hungarian Central Statistical Office (KSH), industrial producer prices in March 2026 were 1.2% higher on average than a year earlier and 3.9% higher than in the previous month.

The Middle East conflict escalated once again after Trump launched his “Project Freedom” military operation, leading to declines in US stock markets

The balance in the Middle East war tilted once again toward escalation after Donald Trump announced a naval operation dubbed “Project Freedom” on Monday, aimed at reopening the Strait of Hormuz. The operation, however, failed to deliver an immediate improvement in maritime traffic and instead triggered Iranian military retaliation: several commercial vessels were hit by drone and missile strikes, an oil terminal caught fire in the United Arab Emirates, and Iran expanded its maritime control zone, according to a statement by the Islamic Revolutionary Guard Corps. At the same time, Washington reported the destruction of six Iranian fast attack boats and the successful passage of two cargo ships, claims that were denied by Iran.

Rising tensions pushed major indices lower, with the Nasdaq down 0.2%, the S&P falling 0.4%, and the Dow declining 1.1%, meaning both the Nasdaq and the S&P retreated from their record highs set on Friday. Ten of the S&P 500’s eleven sector indices closed lower, led by the materials sector with a 1.6% decline, followed by a 1.2% drop in industrials. In contrast, the energy sector rose 0.9%. Shares of GameStop fell 10%, while eBay climbed roughly 5% after the video game retailer proposed acquiring the online marketplace for around USD 56 billion in a cash-and-stock deal. FedEx shares dropped 9.1%, and United Parcel Service fell 10.5%, after Amazon announced the launch of “Amazon Supply Chain Services,” opening up its logistics network to other companies. Palantir shares rose 1.4% ahead of the release of its quarterly earnings report after the market close.

Brent crude oil futures surged 5% on Monday to USD 114 per barrel, the highest level since mid-2022, as tensions in the Middle East escalated sharply. Meanwhile, WTI prices rose 4.4% to above USD 106 per barrel.

Global risk aversion pushed bond yields higher and weighed on regional currencies

Bond yields edged higher again, with 10-year yields rising by around 5 basis points in both the US and Europe. The US 10-year yield approached 4.45%, while the German 10-year moved close to 3.1%. The dollar strengthened by a quarter of a percent against the euro, with EURUSD slipping below 1.17.

Heightened risk aversion driven by rising oil prices weighed on regional currencies: the Czech koruna weakened by 0.1%, the zloty by 0.3%, and the forint by 0.6% against the euro, with EUR/HUF moving above the 365 level. In the domestic government bond market, reference yields—set in the early afternoon—declined compared to Thursday’s levels by 1–2 basis points in the segment up to three years and by around 5 basis points at longer maturities, reflecting further yield declines on Thursday followed by a modest rebound yesterday. The 10-year yield fell below 6%. Demand was strong at the DKJ switch auction, where the Government Debt Management Agency (ÁKK) accepted more than HUF 50 billion out of bids totaling close to HUF 70 billion.

Today's highlights

Asian equities declined on Tuesday as oil prices eased, although they remained above USD 100 per barrel. Investors also paid close attention to the yen after the Japanese currency briefly surged in the previous session, fueling renewed speculation about fresh FX market intervention by Tokyo. The MSCI’s broadest index of Asia-Pacific equities excluding Japan fell 0.3%.

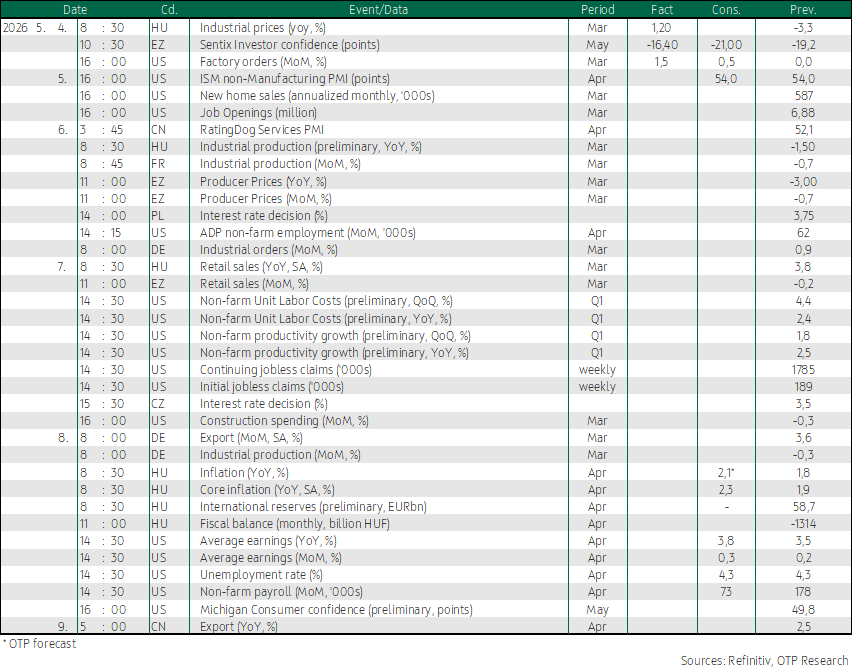

Today, attention will be focused on data coming out of the US, including the ISM non-manufacturing PMI, new home sales, and March labor market data. In addition, companies such as AMD, HSBC, and Pfizer are scheduled to report earnings.

Today, the Government Debt Management Agency (ÁKK) is offering HUF 30 billion worth of three-month Treasury bills (DKJ).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more