OTP Morning Brief: On Friday, the S&P and the Nasdaq closed at new highs following the turnaround in the oil market

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

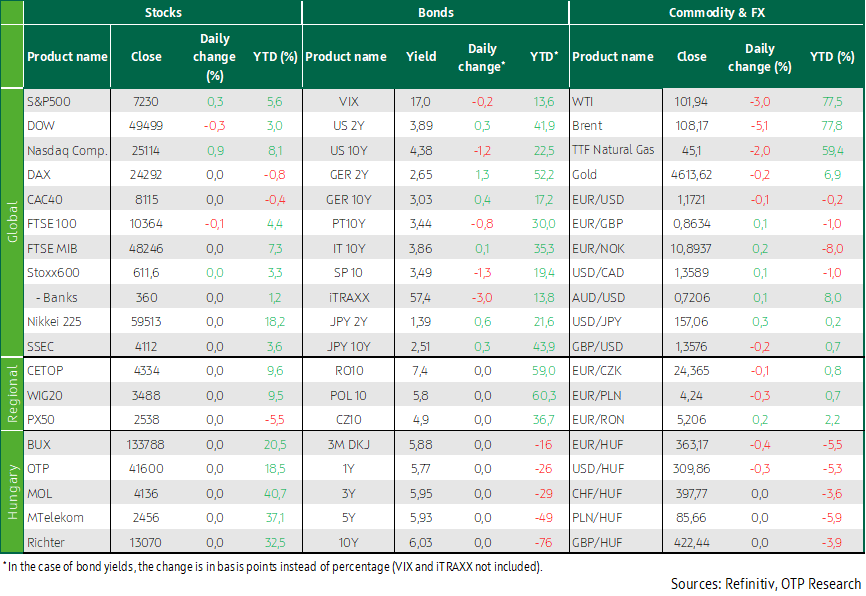

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The absence of further escalation in the Middle East, combined with month-end technical factors, led to a turnaround in the oil market last Thursday. Since then, futures prices have declined steadily, while the opposing parties have adopted a more constructive tone. According to President Trump’s latest statement, efforts are being made to assist vessels stranded in the Strait of Hormuz; at the same time, the US president also voiced his dissatisfaction over the Iranian peace proposals over the weekend. European equity futures point to a positive open today; however, sentiment may be tempered by an unfavorable announcement made by Trump over the weekend regarding European automakers, stating that a 25% punitive tariff would be imposed on the sector. Over the past week, corporate earnings reports also supported the equity market rally, while the large volume of macroeconomic data releases failed to deliver any major negative surprises, and central banks adopted the hawkish tone that can be expected under the current circumstances. The coming week is expected to be less intense; from a macroeconomic perspective, the most important events will be the release of Hungary’s April CPI and fiscal data, as well as the US April job report.

Following Thursday’s turnaround in the oil market, Western European stock markets rose on Thursday, while on Friday the vast majority of European markets remained closed

Thursday’s session, similarly to previous days, started with further losses across the major Western European stock exchanges; however, sentiment improved during the day thanks to a turnaround in the oil market, and equity indices began to rise. Ultimately, optimistic sentiment led key benchmarks more than 1% higher. Following four consecutive days of declines, the Stoxx 600 ended the session up 1.4%, the FTSE 100 rose by 1.6%, while the DAX posted a 1.1% daily gain in the last session ahead of May 1 public holiday. Among the Stoxx 600 sector indices, healthcare, utilities, and industrials led the advances, with the defense industry standing out within industrials. Rolls-Royce soared nearly 8% after announcing that it was maintaining its previous earnings guidance. Among pharmaceutical stocks, AstraZeneca climbed nearly 2%, while Novo Nordisk rose 4.5%. The banking index edged lower after several French banks released disappointing quarterly results. Puma skyrocketed 5% after reporting better-than-expected Q1 revenue and operating profit figures.

Overall, leading European equity indices delivered mixed performance over the week: the Stoxx 600 gained 0.1%, the DAX strengthened by 0.7%, while the FTSE 100 slipped 0.1%. On May 1, most European stock exchanges were closed, with the exception of London, where the benchmark edged down 0.1%. Over the course of April, despite the geopolitical crisis, major Western European indices recorded strong gains: the Stoxx 600 rose 5%, the DAX rose 7%, the CAC 40 rose 4%, while the FTSE climbed 2%.

Regional equity indices mostly declined yesterday: the Warsaw index fell 0.5%, while the Prague index dropped 2%. The BUX, however, rose 0.9%, despite a modest decrease in OTP, as Richter gained 2%, Mol was flat, and Magyar Telekom’s share price declined 1%. A correction was seen among state-linked stocks, with 4iG soaring 7% and Opus skyrocketing 11%.

Over the course of the week, regional indices mostly declined, with the BUX performing the best, posting only a 0.1% decrease. As for April, the BUX soared 10%, led by OTP, Magyar Telekom, and Richter, while the WIG20 rose 4% and the PX rose 1%.

A number of key macroeconomic data releases were published on Thursday: Germany’s preliminary GDP expanded by 0.3% quarter on quarter, outperforming expectations, while German retail sales fell by a much sharper-than-expected 2%. French GDP came in weaker than forecast, whereas Italian and Spanish GDP figures were slightly stronger than expected. In France, CPI rose faster than anticipated in April. CPI for the euro area as a whole also increased more rapidly than expected, while core CPI surprisingly eased to 2.2%. The euro area’s Q1 GDP undershot expectations, expanding by 0.8% year on year and by only 0.1% quarter on quarter. At their meetings last Thursday, both the Bank of England and the ECB left policy rates unchanged. While the ECB remains well positioned to manage uncertainty, officials pointed out that upside risks to CPI and downside risks to growth have intensified. They also noted that longer-term CPI expectations remain stable, although short-term expectations have increased markedly. At the post-meeting press conference, ECB President Christine Lagarde said that the decision to keep rates unchanged was unanimous, although policymakers discussed various options, including a potential rate hike.

Over the weekend, US President Donald Trump said that a 25% punitive tariff would be imposed on European cars.

Following Thursday’s turnaround in the oil market, the S&P reached a new high, and by Friday the Nasdaq had also set a new all-time high

Following Thursday’s decline in oil prices, US equity indices posted a strong rally: led by Alphabet and Apple, the S&P climbed to a new high, while the Nasdaq reclaimed its previous peak. The S&P, the Dow, and the Nasdaq recorded their strongest monthly performances since 2020 in April, with the Nasdaq rising 15% and the S&P advancing 10%. On Friday, the rally continued amid optimism about a potential resumption of peace talks, as oil prices edged lower further and corporate earnings reports continued to support gains. Both the S&P and the Nasdaq set new highs, while the Dow eased slightly.

Apple shares rose 3.3% after the company issued solid sales guidance, highlighting strong demand for its flagship products, the iPhone 17 and the MacBook Neo. Software stocks also moved higher after Atlassian revised its full-year outlook upward, with the company’s shares soaring nearly 30%. Among peers, Salesforce advanced 4%, while ServiceNow gained just over 3%. Roblox, meanwhile, plunged 18% following a downward revision to its full-year revenue guidance. Reddit shares skyrocketed 13% on the back of an optimistic quarterly revenue outlook. Exxon Mobil’s quarterly profit was negatively affected by the Middle East conflict, while Chevron beat profit expectations; however, its overall earnings fell to their lowest level in five years, leading the two stocks to decline by 1.0% and 1.4%, respectively.

Earnings reports remain largely positive; based on analyst expectations, this points to nearly 28% year-on-year profit growth in Q1, according to LSEG I/B/E/S data—almost 12 percentage points higher than analysts’ estimates a week earlier. Over the week as a whole, the S&P and the Nasdaq each rose by around 1%, while the Dow gained 0.5%.

As part of Thursday’s data deluge, several key releases were published, including a Q1 GDP print pointing to 2% growth—slightly weaker than expected but faster than the subdued expansion seen in Q4 last year in the initial estimate—along with consumer spending price data in line with expectations and personal income figures rising faster than forecast. Data also indicated an acceleration in consumer spending growth. Weekly jobless claims fell to their lowest level since 1969, while the number of continuing claims dropped to a more than one-year low. This was followed on Friday by the release of final S&P PMI data and the manufacturing ISM index: the former came in stronger than expected, while the latter undershot expectations slightly.

Oil prices showed significant volatility on Thursday, with futures turning lower from four-year highs: WTI fell by nearly 2%, while Brent declined by more than 3%. On Friday, optimism surrounding the potential resumption of Iranian-U.S. peace talks—or at least the avoidance of further escalation—led to additional declines in oil prices, trimming the past week’s price increase to 8% for WTI and 3% for Brent. During the week, the United Arab Emirates announced its withdrawal from OPEC and OPEC+, in line with its strategy. Over the weekend, the remaining OPEC+ members decided on a further increase in production quotas, a move that is currently of largely symbolic significance due to the blockage of the Strait of Hormuz.

Despite the correction that began on Thursday, developed-market government bond yields increased over the past week, while the EUR/USD closed above 1.17.Domestic yields continued to decline during the week, and the EUR/HUF finished near 363

Last week also failed to deliver a breakthrough regarding the Middle East oil crisis. Ceasefire talks stalled, Donald Trump signaled the possibility of further major military strikes, the Strait of Hormuz remained closed, and global oil inventories continued to decline due to demand exceeding supply. As a result, oil prices rose by a further 7–10% over the week as a whole, despite a roughly 5% correction in the second half of the week amid strengthening hopes for a peace agreement.

Incoming macroeconomic data pointed to weaker-than-expected growth and higher price pressures driven by oil prices. In the euro area, Q1 GDP expanded by 0.1% quarter on quarter (vs. 0.2% expected), while the annual growth rate slowed from 1.2% to 0.8%. In the U.S., GDP grew at an annualized 2% pace in Q1, also slightly below expectations. In the euro area, CPI rose from 2.6% to 3.0% in April, compared with a 2.9% consensus, even as core CPI unexpectedly eased to 2.2% and services CPI to 3.0%. In the U.S., the headline PCE CPI surged from 2.8% to 3.5%, while core PCE accelerated from 3.0% to 3.2%, alongside a 0.3% month-on-month increase.

Both the ECB and the Fed left policy rates unchanged this week, but at both central banks the emphasis shifted toward monetary tightening. In the US, markets continue to expect an unchanged policy rate this year, although the probability of potential rate cut(s) has declined. In Europe, expectations for rate hikes have strengthened, with markets effectively pricing in around 100 basis points of cumulative tightening this year and a 3% policy rate by year-end, potentially followed by a rate cut in 2027. Bond yields increased over the week despite a correction that began on Thursday. In Europe, 10-year yields moved 5–10 basis points higher, with the German 10-year closing near 3.05%, above the post-pandemic trading range. In the U.S., the 10-year Treasury yield rose by nearly 10 basis points over the week to around 4.4%, approaching the middle of its post-pandemic trading range.

The EUR/USD fluctuated between 1.165 and 1.18 and ultimately closed slightly higher, above 1.17, although the 25% retaliatory tariff on European cars announced over the weekend has not yet been priced in.

In regional FX markets, the zloty and the koruna traded broadly sideways over the week, while the forint ultimately strengthened—moving from around 366 to 364 by Thursday, and reaching as strong as 363 during illiquid trading on Friday. Several factors contributed to the appreciation. Following talks in Brussels, Péter Magyar, the incoming prime minister of the election-winning Tisza Party, stated that an agreement enabling the use of EU funds would be signed in May. The NBH kept its policy rate unchanged at 6.25%, in line with expectations, but Governor Mihály Varga struck a hawkish tone on the outlook due to CPI risks linked to the oil crisis, while noting that the central bank would support euro adoption should the government decide to pursue it. In addition, domestic GDP expanded by a stronger-than-expected 1.7% in Q1, a performance that may have been partly supported by pre-election spending.

Today's highlights

Asian stock markets opened the week on an optimistic note, supported by the turnaround in the oil market and an increasingly conciliatory tone between Iran and the U.S. Ahead of the morning close, the Nikkei was up 0.5%, the Hang Seng was 1.5% higher, while Korean benchmarks were showing gains of 2–6%.

WTI futures slipped 1.3% this morning, falling below USD 101 per barrel. Equity futures point to a broadly higher open in both Europe and the US .

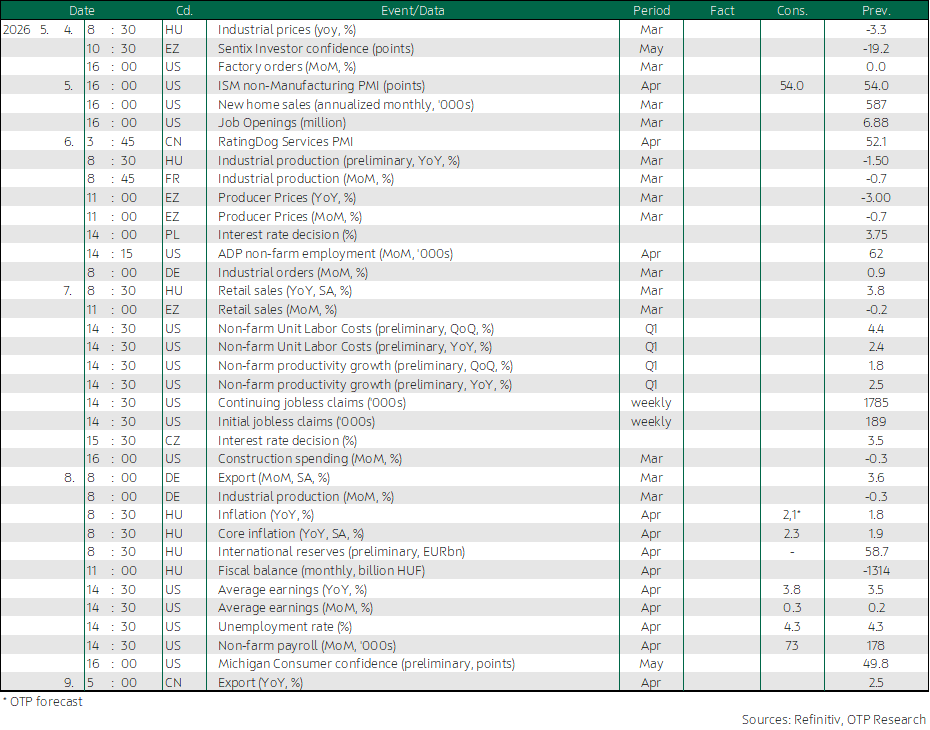

Today, attention will be focused on the euro-area Sentix investor confidence index and US factory orders data. In Hungary, the Central Statistical Office (KSH) will publish March industrial producer data.

Over the course of the week, the focus among international data releases will be on the U.S. labor market report. In the Hungarian market, investors will be watching several key macroeconomic indicators, with the most notable being the release of April CPI data and the April fiscal balance, both scheduled for Thursday.

We are still far from the end of the quarterly earnings season. Today, attention will be on reports from Palantir, BAT, and Vertex. Looking ahead, earnings from companies such as AMD, Pfizer, HSBC, Anheuser-Busch, Infineon, Novo Nordisk, BMW, Shell, McDonald’s, and Rheinmetall are also expected to be in focus.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more