OTP Morning Brief: Stock markets surged following the U.S.–Iran ceasefire agreement

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Europe and the U.S. both closed with solid gains, long-term yields fell, and rate-hike expectations eased. The travel sector and mining stocks were the biggest winners, while energy stocks declined amid a roughly 15% drop in oil and gas prices. However, by this morning markets have turned uncertain again: Asian markets, as well as European and U.S. futures, are mostly in decline due to conflicting news about the ceasefire. Beyond developments related to Iran, it will be worth watching domestic international reserve data today, while in the U.S. the Fed’s closely monitored February core PCE inflation figure will be released. From Western Europe, German industrial production will be the most notable, and within the region the Polish rate decision will also be important to follow.

European stock markets surged after the U.S.–Iran ceasefire agreement

U.S. President Donald Trump and Iran, with Pakistan mediating, agreed to a temporary two-week ceasefire, which significantly eased fears of a global energy market shock. As geopolitical risks receded, oil and gas prices fell by around 15%, rate-hike concerns diminished, bond yields declined, risk appetite increased, and equity markets rose sharply. Europe’s “fear gauge,” the STOXX volatility index, fell below 25 points for the first time in more than three weeks.

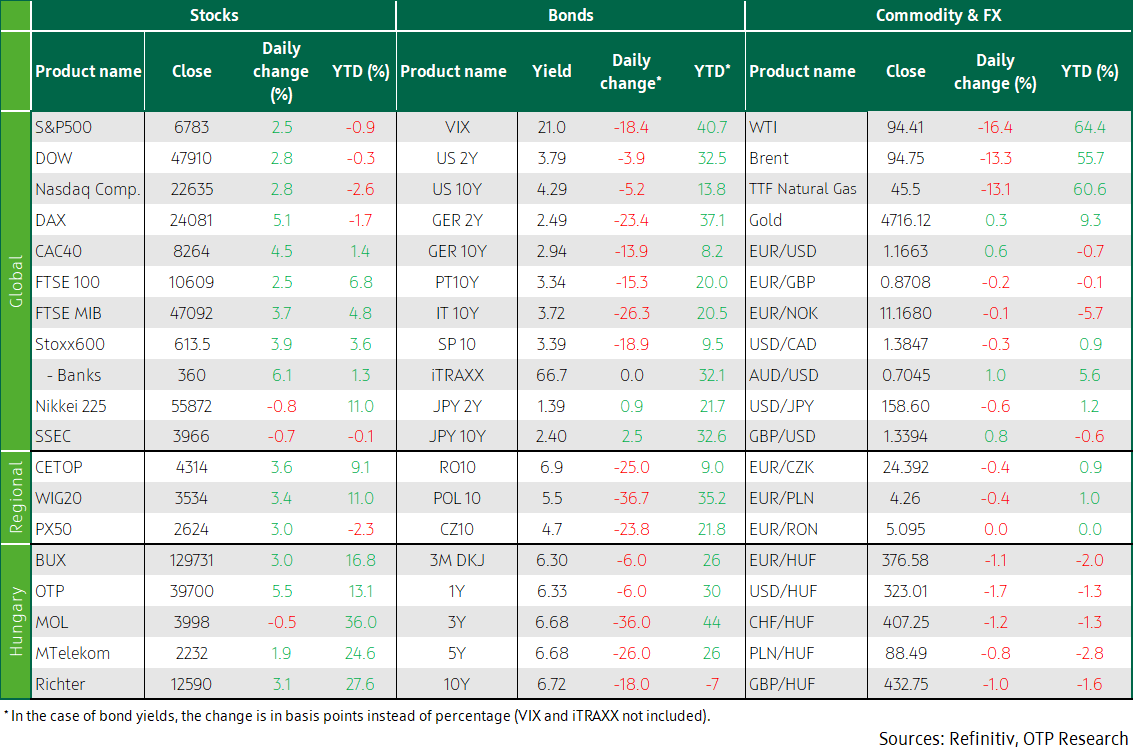

European stock markets opened with strong gains yesterday, as global investors welcomed news of the conditional ceasefire between the United States and Iran. Supported by the improved sentiment, major European indices saw substantial increases: the STOXX 600 rose by 3.9%, the FTSE 100 by 2.5%, the DAX by 5.1%, and the CAC 40 by 4.5%. By sector, the biggest winners were automotive (+5.3%), mining (+5.2%), and travel (+7%). Airlines were the top performers, with their shares gaining more than 10%. European macro data had little impact, but it is worth noting that eurozone retail sales growth slowed from 2.1% to 1.7%, while the construction confidence index deteriorated further.

Regional indices also closed strongly higher: the BUX and the Prague Stock Exchange rose by 3%, while Poland’s WIG gained nearly 3.4%. Among Hungarian blue chips, only MOL fell (-0.5%), while Magyar Telekom rose 1.9%, Richter 3.1%, and OTP closed with a 5.5% gain.

Hungarian March inflation came in well below expectations: headline inflation was 1.8% (vs. market consensus 2.2% and OTP’s 2.0%). Core inflation slowed from 2.1% to 1.9%. The stronger-than-expected figure was partly due to non-durable goods and partly to processed food prices.

Hungarian retail sales grew by 3.8% year-on-year in February 2026, slightly accelerating from the 3.5% pace seen in the previous two months. Month-on-month growth, however, slowed from 0.5% to 0.4%. Industrial production data for February 2026 also came out: output fell by 1.5% year-

on-year, an improvement from January’s 2.5%, but still showing no meaningful turnaround, Hungarian industry has yet to move sustainably off its low point.

U.S. markets also rallied strongly on ceasefire news

Following the announcement of the U.S.–Iran ceasefire, U.S. markets surged yesterday as well: the Dow and the Nasdaq rose by 2.8%, the S&P 500 gained 2.5%. Of the S&P 500’s eleven main sectors, eight rose at least 2%, led by industrials. Energy stocks — hurt by falling oil prices — were the only losers, dropping 3.7%. Sectors hit hard since the start of the war saw a strong rebound: commercial airlines +5.7%, travel and leisure +5.2%, homebuilders +4.9%. Delta Air Lines gained 3.8% despite a weaker-than-expected Q2 profit forecast. The company declined to update its annual guidance due to uncertainty linked to the Iran conflict. Delta’s competitors also rallied: Southwest Airlines rose 6.7%, United Airlines 7.9%.Among cruise operators, Carnival gained 11.2% and Norwegian Cruise Line 7.6%.

Rate-hike expectations eased, long-term yields declined

The ceasefire significantly lowered rate-hike expectations and pushed down bond yields — though primarily in Europe. In the United States, unchanged interest rates until late 2026 remain the most likely scenario. In Europe, markets now expect only two 25-basis-point hikes, down from the previously anticipated three to four. The U.S. 10-year yield ended unchanged at 4.3%, while the German yield fell by 15 basis points to around 2.9%. French and Italian long-term yields dropped by 20–30 basis points.Improved sentiment weakened the dollar notably: EURUSD rose by 0.6%, surpassing 1.165.

Regional currencies also strengthened significantly: the Czech koruna and the zloty by 0.5%, the forint by 1.3%, reaching a 2.5-year high vs. the euro, with EURHUF approaching 376.Hungarian rate-hike expectations also eased sharply: instead of the previously priced four to five 25-basis-point hikes, markets priced in only one yesterday. Domestic government bond yields also fell substantially: longer-term reference yields were down by 15–30 basis points, with the 10-year yield dropping to around 6.7%. The better-than-expected inflation figure likely contributed to the move.

Today's highlights

However, by this morning sentiment has deteriorated, as cracks quickly emerged in the fragile ceasefire, which pushed oil prices higher again and reminded investors that the inflationary consequences may remain with us for a long time. On the one hand, the Strait of Hormuz has not reopened yet; on the other hand — although the U.S., Israel and Iran did not attack each other — Israel again struck Lebanon yesterday, and Iran launched rockets at several Gulf states. As a result, U.S. crude oil futures rose by 2.8% to 97 dollars per barrel, while Brent increased by 2.1% to 96.7 dollars. Among equity markets, Japan’s Nikkei is down 0.8% after yesterday’s 5.4% jump, and the SSEC is falling by 0.7%. On Wall Street, S&P 500 futures and Nasdaq futures are both down 0.2% as Wednesday’s rally faded. Pointing to a mixed European open, EUROSTOXX 50 futures are up 0.1%, DAX futures are down 0.3%, while FTSE futures have risen by 0.5%.

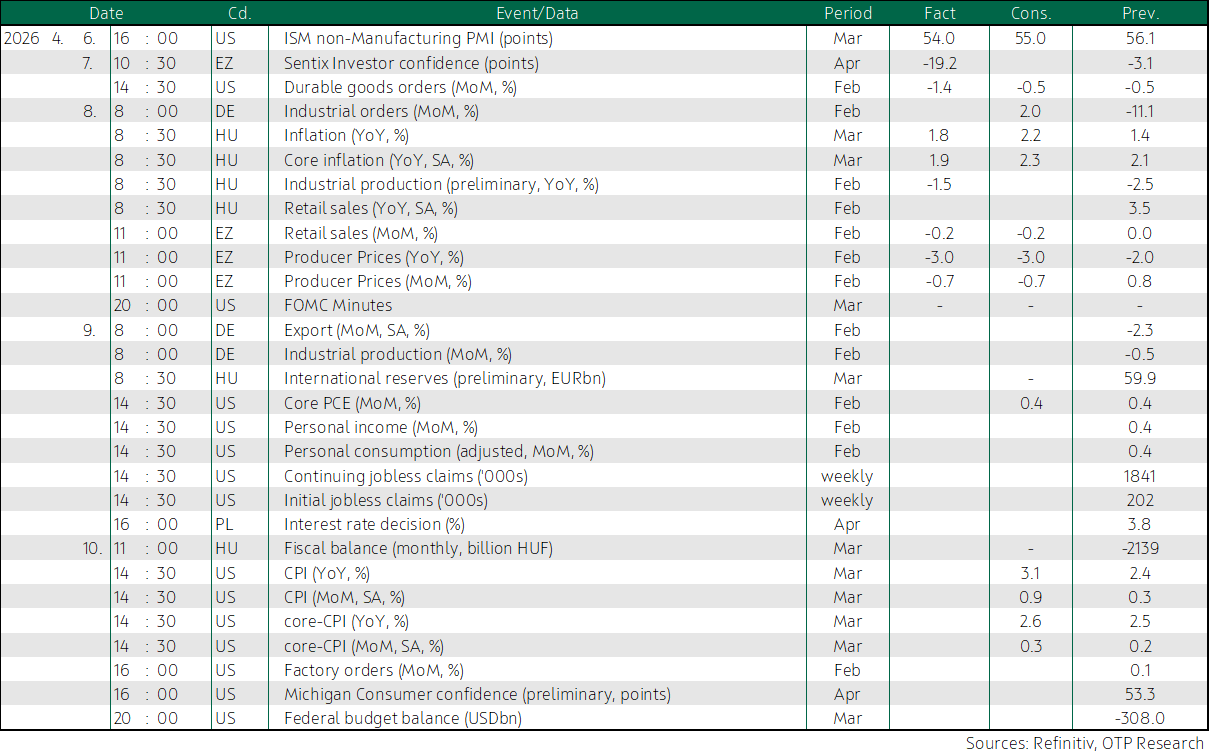

From Hungary, today the MNB’s international reserve data will be released, while from overseas the Fed’s closely watched February core PCE inflation figure arrives. From Western Europe, German industrial production will be the most notable, and within the region it will also be worth following the Polish rate decision.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more