OTP Morning Brief: There have been signs of a de-escalation of the Middle East conflict

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

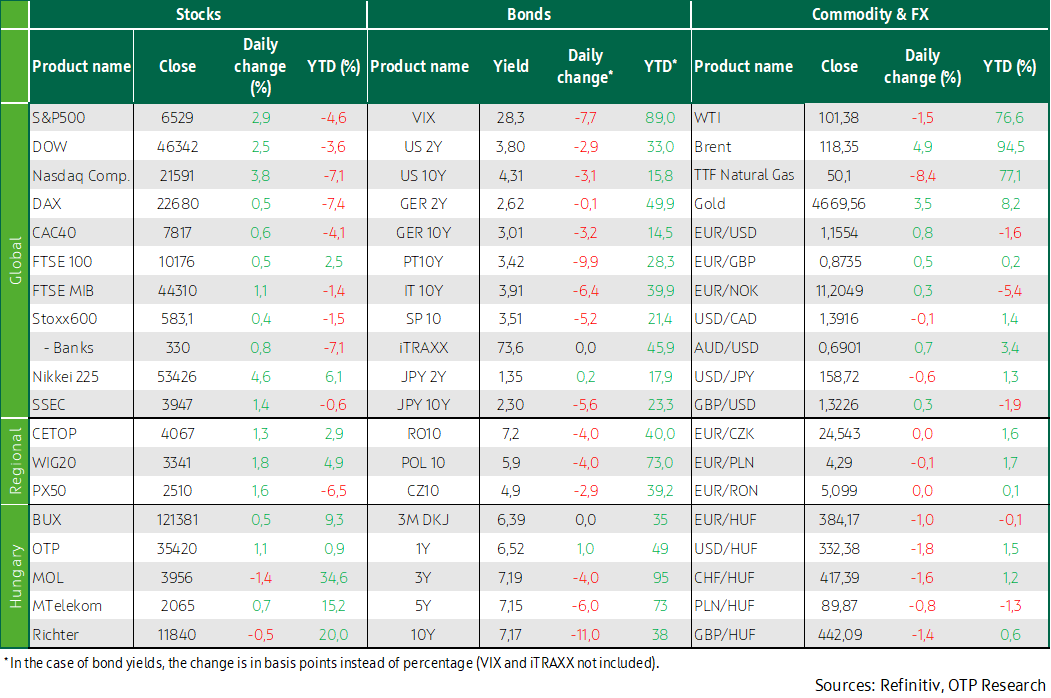

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Both the United States and Iran have signalled an easing of tensions. Key European and US indices, as well as stock markets in the CEE region, climbed. Headline inflation accelerated sharply in the eurozone in March, while core inflation slowed on an annual basis. In March, WTI rose by 51% and Brent by 63%. Developed economies’ bond yields fell, and the euro strengthened against the dollar. Domestic bond yields fell. The forint strengthened against the euro. The Hungarian Central Statistical Office (KSH) will publish the government sector’s fourth-quarter balance today. In the eurozone, February’s unemployment rate will be released. In the United States, the ADP Institute will release its March employment data, and the ISM Institute’s March manufacturing index, as well as retail sales data for February, will be released.

Major European stocks rose on Tuesday; significant losses built up throughout March

Tuesday’s trading brought a cautious rise on key Western European stock markets, but for March as a whole, this still meant heavy monthly losses—the worst in four years—accumulated in the shadow of the Middle East conflict. The pan-European Stoxx 600 rose 0.4% on the last trading day of March, while for the month as a whole, it fell 8%. Tuesday’s relief was primarily due to a comment by Donald Trump, who said he is prepared to end military operations even if the Strait of Hormuz remains closed. Investors, however, remain cautious, as this would not be the first statement pointing toward de-escalation in the past four weeks that has failed to bring a resolution.

Most of the Stoxx 600 sector indices rose, with the best performance coming from the basic resources sector (+2.3%). Among individual stocks, UBS is worth highlighting, as it rose 4% after the Financial Times reported that Swiss lawmakers had assured the lender that they would ease capital requirements; this news boosted the entire financial sector, which rose nearly 2%. Unilever shares fell 7.3% after the company reported that it is in advanced stages of talks to merge its food business with McCormick (-7.0%). Alstom shares jumped 5.4% after the train maker announced that it had won an $800 million contract for a multinational system.

Headline inflation in the eurozone accelerated by 1.2% MoM and by 2.5% YoY in March; the surge was almost entirely driven by higher fuel prices. Meanwhile, core inflation moderated from 2.4% to 2.3% YoY, mainly due to a slowdown in services inflation (from 3.4% to 3.2%), which, however, may rise later due to second-round effects of rising energy prices. Following the release of the data, market pricing regarding the ECB’s interest rate path for this year remained unchanged, with a 75-basis-point hike expected by year-end. Retail sales in Germany fell sharply MoM (-0.6%) in February, following a significant decline in January, instead of the expected modest expansion.

Stocks in the CEE region also rose yesterday, the BUX lagging behind with a 0.5% gain. Hungarian blue chips closed mixed. Looking at March as a whole, the region’s stock markets also fell; the BUX dropped by 4.1%.

According to data from the Hungarian Central Statistical Office (KSH), average gross earnings rose by 26.3% in January. Behind this unusually high figure is the six-monthly “service premium” (the so-called “firearms money”) paid to members of the army and the law enforcement personnel in January, which accounts for 18 percentage points of the increase.

The price of European TTF natural gas fell by just over 2% yesterday but still remained above 50 EUR/MWh.

Wall Street indices rose; Brent and WTI prices rose by more than 50% in March

Investors' optimism on Wall Street was fueled by Donald Trump's comments pointing toward a de-escalation of the Middle East conflict, as well as an unconfirmed report that Iranian President Masoud Pezeshkian was open to ending the war with security guarantees. Earlier, however, U.S. Secretary of Defense Pete Hegseth warned Tehran that the conflict could escalate if no agreement is reached. Tech giants—including Nvidia (+5.6%), Alphabet (+5.1%), and Meta (+6.7%)—led the major indices higher, driving the NASDAQ up 3.8%. Semiconductor manufacturers also performed well, while energy stocks fell despite rising oil prices. For the month of March as a whole, we saw declines of around 5% on the major Wall Street indices.

CoreWeave rose 12% after the company secured an $8.5 billion loan to expand its artificial intelligence infrastructure. Marvell Technology rose 12.8% after Nvidia invested $2 billion in the company.

The March consumer confidence index showed a slight increase instead of the expected decline. According to data released yesterday, the number of job openings in the United States fell more than expected in February, and hiring sank to a low not seen in nearly six years. While the incoming data reinforced concerns about labor market stability, it did not affect interest rate expectations for this year. The market continues to expect the Fed to keep the base rate unchanged for the rest of the year.

Indications of a de-escalation in the Middle East conflict helped drive down the price of WTI, which fell by 1.5% to around $101; in March, it had risen by 51%, a rise not seen since May 2020. Brent continued to rise yesterday, with prices climbing nearly 5%. In March, Brent crude prices rose 63%, marking a monthly jump not seen since 1988.

Developed economies’ bond yields fell; the euro strengthened against the dollar; the forint strengthened against the euro

Yesterday, almost everything pointed to a decline in inflation fears, expectations of interest rate hikes, and long-term yields. Not only the United States but also Iran expressed a willingness to end the war, causing oil prices to fall from their previous highs. In addition, eurozone inflation rose less than expected, while consumer and services inflation declined, and German retail sales were weak. In the United States, a decline in the number of job openings and voluntary quits pointed to a further cooling of the labor market. The US 10-year bond yield fell by 5 basis points to 4.3%, and a similar decline occurred in Europe across the German, French, and Italian bond markets, with the 10-year German yield closing at 3% again. Due to the return of risk appetite, the euro strengthened by 0.8% against the dollar, with the EUR/USD rising to around 1.155.

Although the exchange rates of the zloty and the Czech koruna barely changed against the euro, the forint strengthened by 1% to the 384 level. Expectations of regional interest rate hikes also eased, and bond yields fell. In the domestic bond market, yields on three- to five-year bonds fell by 5 basis points, while longer-term yields fell by 10 basis points; the 10-year yield returned to around 7.1%. Amid subdued demand, the ÁKK sold the announced HUF 20 billion worth of three-month DKJ at an average yield of 6.44%.

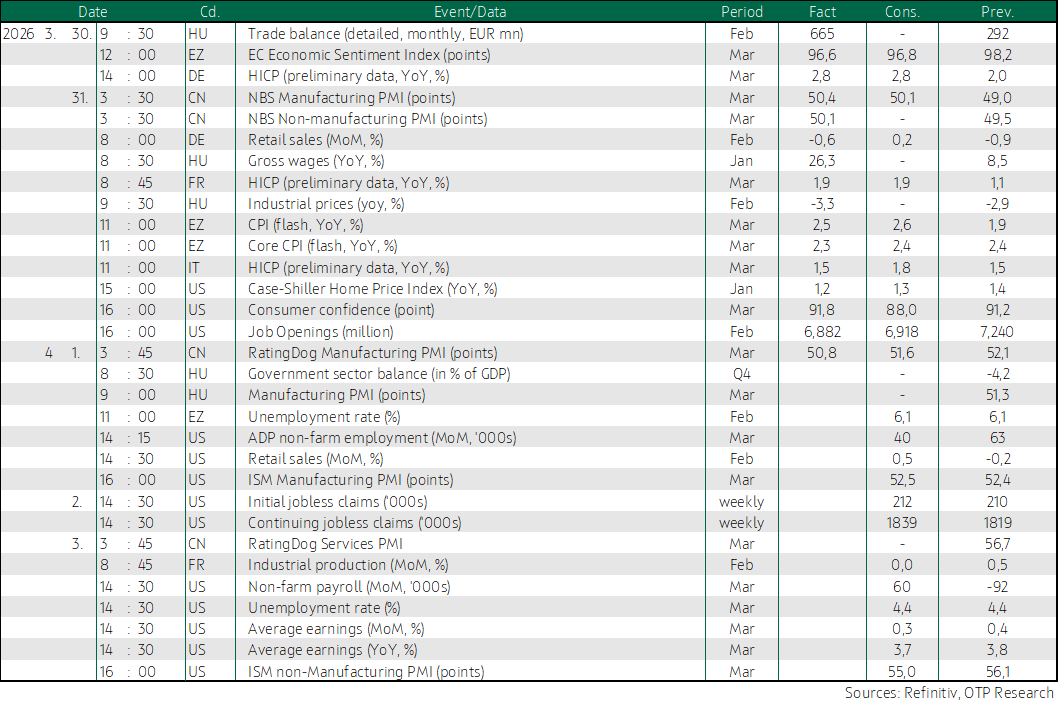

Today's highlights

Optimistic investor sentiment dominated trading this morning on stock markets across the Asia-Pacific region, with all major indices moving higher. In addition to news pointing toward an easing of the conflict in the Middle East, investors were encouraged by South Korea’s sharp jump in exports in March and Japan’s Tankan business confidence index, which showed improvement in Q1. In China, however, RatingDog’s March manufacturing purchasing managers’ index fell more than expected, though it remained in expansionary territory. Trading in the crude oil market opened higher today. Index futures point to a positive opening in both Europe and the US.

The Hungarian Central Statistical Office (KSH) will publish the government sector’s fourth-quarter balance today.

From the eurozone, February’s unemployment rate is due, which is expected to have remained at 6.1%, its historic low.

In the United States, the ADP Institute will publish its March employment data, which, according to market expectations, will show a more modest increase in employment compared to February, but it is important to note that the ADP data does not correlate with the official statistics due on Friday, where expectations are that the sharp decline in February will be followed by a rebound in March. The ISM Institute’s March manufacturing index is also due, with the market expecting it to remain roughly at the same level as the previous month; however, rising input prices will eventually have to leave their mark on manufacturing performance. Retail sales may show a jump in February following the weak data from the previous two months. This data is also very important in terms of growth expectations, as AI investments or not, household consumption is the engine of U.S. economic growth.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more