OTP Morning Brief: Tensions in the Persian Gulf have not eased

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Yemen’s Houthi militia launched attacks on Israel over the weekend, further escalating tensions in the Persian Gulf and stoking fears of a protracted war and a wider conflict on Monday. Crude oil prices rose further on Monday; futures traded at nearly four-year high during the day, but Brent returned to near Friday's closing level by the end of the day. The sentiment was sour on Monday morning; Europe’s stock indices made it back into positive territory, but their US peers mostly closed in the red. In the risk-averse sentiment, developed economies’ long-term bond yields sank. The EUR/USD fell to 1.151. Hungary’s bond market slightly outperformed its regional peers. The EUR/HUF remained below 390. Today’s highlights include the eurozone’s CPI, US house price statistics and JOLTS labour market data. Reportedly, President Trump was ready to end the Iran war without reopening the Strait of Hormuz. Crude oil futures were flat this morning, but most stock markets in Asia fell deeper.

Monday’s trading started on a bad note, before indices reversed

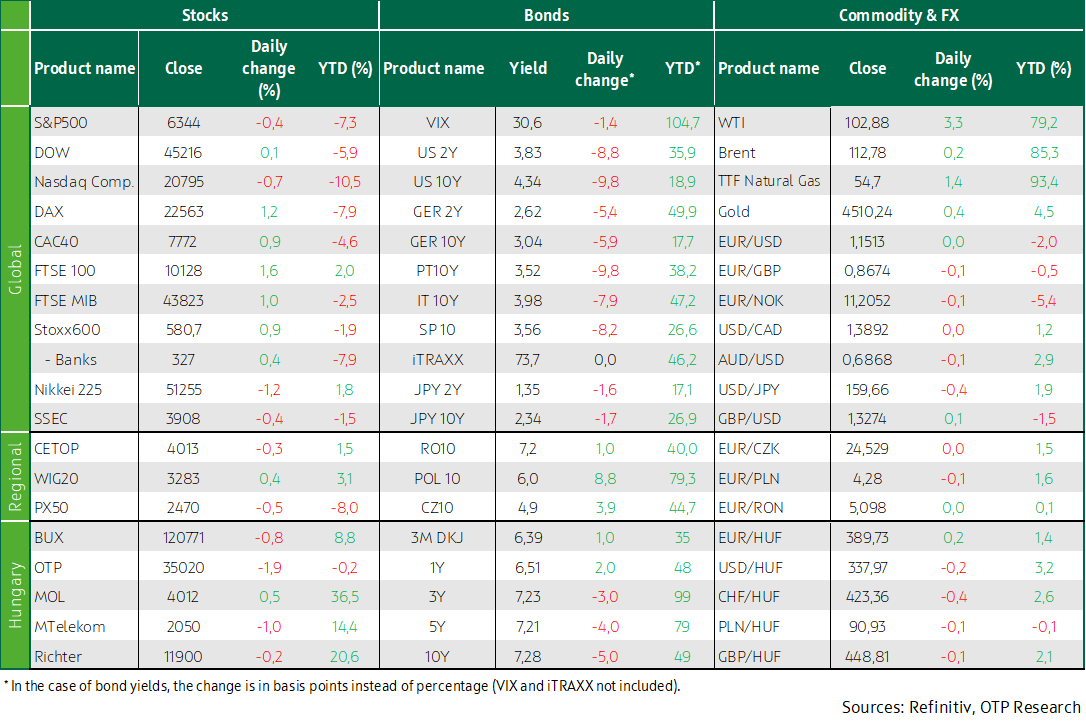

In Europe, stock markets opened in the red on Monday after a sell-off swept through Asia as investors braced for a protracted Gulf conflict. The latest concern about the Middle East situation was that Yemen's Houthis entered the conflict over the weekend, firing missiles at Israel, further deepening fears of an escalation of the Iran war. Brent briefly jumped 117 USD/barrel, and, despite a subsequent reversal, it had gained more than 45% in a month. Inflation fears related to the rise in oil prices were confirmed by Germany’s preliminary inflation data for March: the increase in the HICP accelerated to 2.8% year-on-year in March, from 2% in February, and the picture of accelerating inflation was already confirmed by the regional data released in the morning. The eurozone’s economic sentiment index deteriorated slightly in March, and the final reading of the consumer sentiment index confirmed the deterioration reflected in the preliminary data. In the eurozone, Consumer inflation expectations jumped from 26 points to 43 points in March. Despite the rapid rise in oil prices, European stock indices climbed higher. The Stoxx600 increased by 0.9%, but it lost 8.5% in March, apparently marking the biggest one-month decline since March 2020. The FTSE100 (+1.6%) and the DAX (+1.2%) closed higher. Utilities and media led the gains in the Stoxx600 sector indices, with energy in third place, fuelled by Shell (+2%) and TotalEnergies (+3.2%). Orsted soared 7% after Bank of America upgraded its investment recommendation on the offshore wind developer to Buy, citing an improving outlook. Tauron Polska Energia (+12%) was the day's winner, after announcing a dividend payment for the first time in a decade. Norsk Hydro also performed well; the aluminium producer jumped nearly 10% as concerns about supply shortages pushed up aluminium prices. Rio Tinto surged 3.5% after the company said three of its four Pilbara iron ore port terminals had restarted operations after Tropical Cyclone Narelle passed.

The CEE region’s indices closed mixed: Poland’s WIG20 gained 0.4%, while the Czech and Hungarian benchmarks dropped. The BUX slid 0.8%; its blue chips showed a mixed picture: OTP (-1.9%), MTelekom (-1%) and Richter (-0.2%), slipped but Mol gained 0.5%. Among small-cap stocks, 4iG fell another 2%, extending Friday's almost 10% plunge, while Opus bounced back 7.6%, paring Friday's 12% drop.

Most of Wall Street’s major stock indices sank on Monday

After significant intraday volatility, US stock indices closed mixed: the S&P500 (-0.4%), Nasdaq Composite (-0.7%), and the Russell2000 (-1.5%) declined, while the Dow inched up 0.1%. The morning’s optimism stemming from negotiations between the US and Iran could not offset Donald Trump's new threats against Iran’s energy targets and fears about the expansion of the war. Meanwhile, Iran called the US peace proposals unrealistic. The VIX index of volatility remained above 30 points. In this situation, investors watched the development of oil prices and its economic effects. The statement of Jerome Powell also supported the stock markets; the Fed Chairman said long-term inflation expectations appear to be sustainable despite the current energy shock and the Fed does not need to react to the current situation for now, Reuters reported.

Among the S&P sectors, industrials, IT and energy fell the most. In contrast, the financial sector index was the winner of the day after the US Department of Labor published long-awaited guidelines aimed at clarifying how asset managers can add alternative assets to retirement plans. For March as a whole, industrials and telecommunications were the biggest losers, down more than 11%, while the energy sector (+12%) was the winner of the month. The energy sector was the only one in the S&P to avoid losses in March.

Chipmakers all closed in the red. Among S&P500 companies, Broadcom and Nvidia escaped yesterday's trading with a 1-2% declines, but AMD (-3%), Intel (-4.5%) and Micron Technology (-10%) slumped. Of megacap companies, Alphabet and Apple closed with moderate losses, Tesla fell almost 2%, while Microsoft, Amazon and Meta edged higher.

Long-term bond yields fell amid the risk aversion, the USD appreciated. Hungary’s FI and FX markets did slightly better than CEE peers

Energy prices continued to rise, WTI added nearly 5% (to USD 105) and Brent upped 1.5% (to USD 115), and the Dutch TTF gas price reached EUR 55. According to preliminary data, inflation in Germany accelerated from 1.9% to 2.7% in March, as expected, due to rising fuel prices. Nevertheless, developed economies’ bond yields subsided from last week’s peaks, as growth concerns increased due to the protracted war and investors turned to less risky assets. The 10Y US yield shed 10 basis points, to 4.35%, the German one by 5 basis points to 3.05%, but the French and Italian 10Y yields sank almost 10 basis points. The dollar strengthened further, and EUR/USD fell by half a percent, to 1.145.

Hungary’s bond and FX markets once again did slightly better than its regional peers. The HUF strengthened against the euro, trading around 388, while other regional currencies weakened slightly. Czechia’s and Poland’s yields inched up yesterday, while Hungary’s yields eased by 5 basis points, the 10Y one fell below 7.3%. Monday's switch auction of HUF 10 billion worth of discount T-bills was twice oversubscribed, but the ÁKK accepted none of the bids.

Today’s highlights

The major stock markets in the Asia-Pacific region traded in the red. Japan’s Nikkei fell more than 1%, its losses increased to 13% in March. China’s Shanghai Composite shed less than 0.5%, while the Hang Seng lost 0.5% before Tuesday's close, putting it on track for a monthly loss of 5-6%. China’s NBS manufacturing and services sector PMI improved slightly in March, according to data released today.

Most index futures boded well for today’s trading session.

Crude oil prices were stagnant this morning. News reports suggest that Donald Trump told his staff that he was willing to end the Iran war without opening the Strait of Hormuz. Crude oil prices have skyrocketed about 45% in March alone. The prices of various plastic raw materials have jumped 30-40% this month.

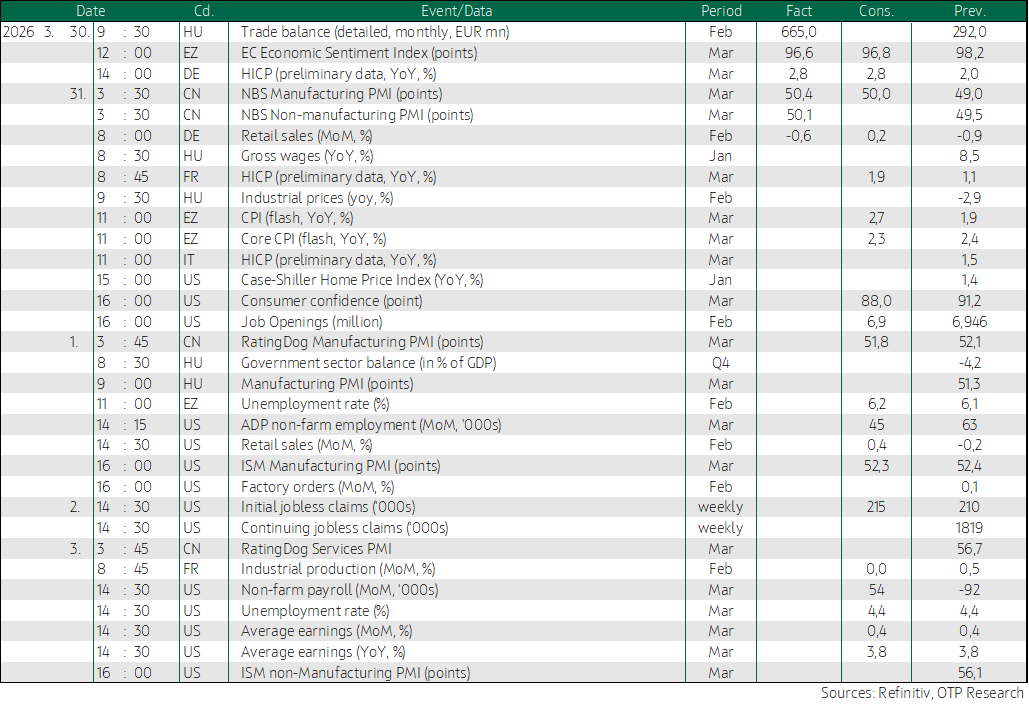

Today, Germany’s retail sales statistics as well as the eurozone’s, France’s and Italy’s inflation data will be worth checking in Europe.

In America, the JOLTS (Job Openings and Labor Turnover Survey) may be the focus of attention today before the US labour market comes to light on Friday. The Case-Shiller home price index for January and the consumer confidence index for March may also be of interest.

In Hungary, the KSH publishes earnings data and industrial producer price indices.

Today, the ÁKK auctions 3M discount Treasury Bills, offering HUF 20 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more