OTP Morning Brief: Uncertainty ruled markets last week

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

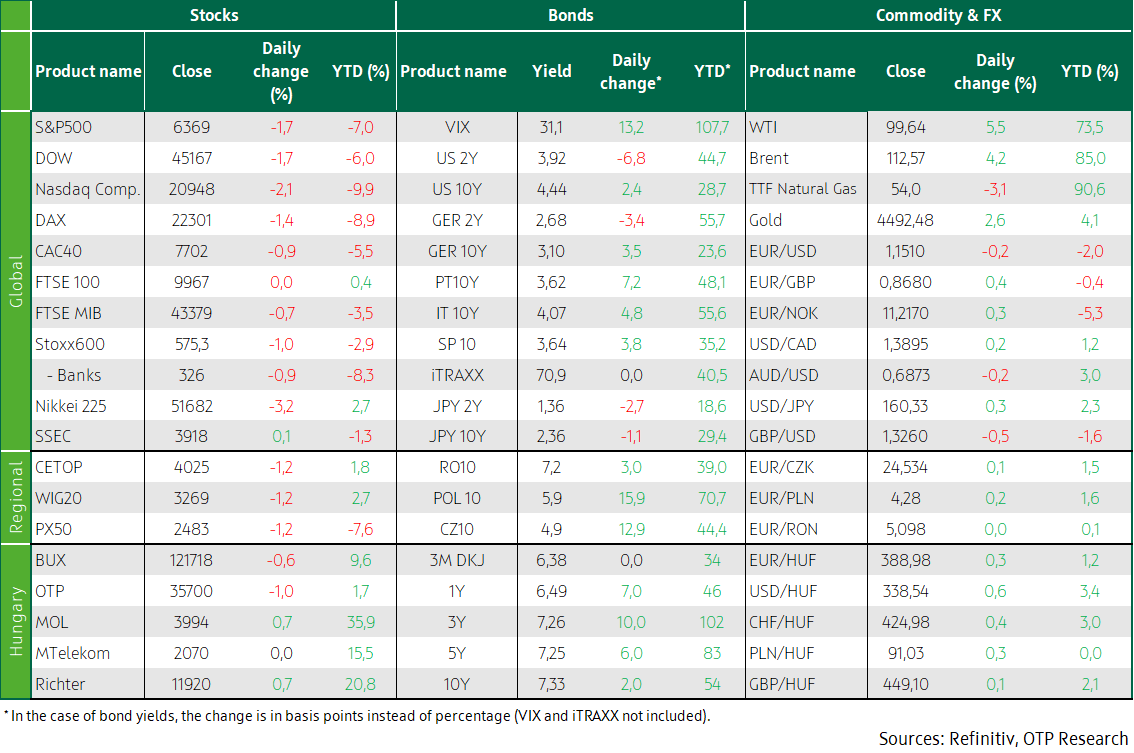

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Last week, investors struggled to react to the mixed news about the Middle East conflict. Europe’s markets fell on Friday but posted weekly gains. But US markets fell both on Friday and last week. Bad weather may have dampened UK retail sales. Interest rate hike expectations and bond yields rose last week. Asia’s markets were deep in red. Eurozone inflation and US labour market data will be worth watching this week.

Complete uncertainty ruled on the fourth week of the Iran conflict

Last week, markets were largely driven by news related to the USA’s and Israel’s war against Iran. At the beginning of last week, Donald Trump lifted the 48-hour ultimatum for Iran to open the Strait of Hormuz and suspended the previously suggested military strikes on Iran’s energy infrastructure for five days, as, according to Donald Trump's post, the USA had held constructive and fruitful negotiations with Iran, but the latter denied this throughout, saying that Iran only received an unacceptable draft and that substantive negotiations have not yet taken place. The only certainty is that the two sides' positions on making peace are still far apart. Donald Trump's milder comments temporarily supported markets and led to an uptick at the beginning of last week, before a new wave of uncertainty. First, Donald Trump said he would postpone attacks on energy infrastructure until 6 April, while Iran accused America of preparing ground operations. On Friday, Secretary of State Mark Rubio denied this, saying that America could achieve its goals without ground troops and that the war could be over within weeks. In the meantime, several ships passed through the practically closed Strait of Hormuz, but this could not bring down oil prices. The total uncertainty surrounding the conflict made investors very risk-averse by the end of last week.

Europe’s stock markets ended a week of doubts with gains

European stocks fell on Friday, but they preserved moderate gains last week; this clearly shows investors' struggle with controversial developments in the Middle East. The STOXX 600 index slipped 0.9% on Friday, while most of its sectors closed in the red. Still, the index rose by 0.4% over the week. Germany’s DAX slid more than 1.4% on Friday, while Britain’s FTSE 100 ended flat; the latter gained 0.5% last week, as much as France’s CAC40 did. In individual stocks, Poland’s Dino slumped 16% as the food retailer said sales growth may have slowed in 2025, partly due to consumer uncertainty. Pernod Ricard shot up 8% after the spirits company said it was in talks about a possible merger with Jack Daniel’s owner Brown-Forman. AstraZeneca surged 3.4% after the drugmaker said its experimental respiratory treatment, Tozorakimab, had been successful in two late-stage clinical trials. Media (-2.7%) was the worst-performing sector in the STOXX 600.

UK retail sales shrank 0.4% month-on-month in February 2026, following an upwardly revised 2% increase in January. The decline was smaller than expected (-0.7%). This was the first monthly contraction in three months, with sales contracting particularly in supermarkets and household goods; retailers blame the rainy weather for the dampened demand.

The CEE region also suffered losses: Poland’s and Czechia’s indices sank 1.2% each, while Hungary’s BUX declined by 0.6%. Hungary’s blue chips moved mixed: OTP slipped by 1%, Richter and Mol advanced 0.7%, while MTelekom stagnated. In Budapest, some small stocks made exceptional strong moves: 4iG nose-dived 9.6% and Opus plunged 12.2%.

Wall Street closed last week with hefty losses

Investors in America were not as optimistic as those in Europe: US stocks extended their losses on Friday, while Wall Street closed its fifth consecutive week of losses, in the longest losing streak in nearly four years. The S&P 500 slid 1.7%, closing its worst week since the start of the Iran war, decreasing by 2.1% over the past week. The Dow Jones Industrial Average dropped by 1.7%, sliding more than 10% off its record high hit last month, while the Nasdaq Composite Index lost 2.1%, which brought last week’s loss to 3.2%. Most stocks on Wall Street fell, including three-quarters of the S&P 500, leaving the index 8.7% below its all-time high in January. Big Tech stocks weighed heavily on the index: Amazon (-4%), Meta Platforms (-4%), and Nvidia (-2.2%) ended in the red. Consumer discretionary companies, which sell non-essential consumer goods, i.e. products that consumers can easily cut back on when their budgets tighten, saw substantial losses. Norwegian Cruise Line Holdings (-6.9%), Starbucks (-4.8%), and Chipotle Mexican Grill (-4.1%) all ended in the red. The VIX index, which measures market volatility, hit levels last seen in 2022, indicating uncertainty.

Interest rate hike expectations and bond yields rose last week

Last week, the Middle East tensions shaped the sentiment, and volatility remained high in advanced economies’ bond and currency markets. Although Donald Trump’s words – that he was in talks with Iran – at the beginning of last week brought some relief, but the news proved to be unfounded. There was no breakthrough, the Strait of Hormuz remained closed, and the parties continued to attack the region’s energy infrastructure. By Friday, oil prices returned to the highs seen at the beginning of last week; Brent crude exceeded USD 110, WTI hit USD 100, and the Dutch TTF gas price stuck around EUR 55.

Although the latest confidence indices suggest that the recovery of the eurozone, which imports a significant portion of its energy, may have stalled in March and that the growth of the energy-exporting US economy may have slowed, inflation fears have increased due to the prolonged war and high oil prices, and the expected path of key interest rates has also risen further. The euro yield curve is pricing in four interest rate hikes for the next 12 months, after President Christine Lagarde indicated that the ECB was ready to raise interest rates “at any meeting”. The market has priced out previous expectations of interest rate cuts in the USA, and although currently the most likely scenario is to leave the key interest rate on hold this year, the priced-in probability that the Fed will have to raise it this year has now increased to 25%. After extraordinary swings – with about 10-basis-point swings on several days –, bond yields rose further last week. The US 10-year Treasury yield jumped to an eight-month high of almost 4.45%, slowly returning to the middle of its post-covid trading range. Bond yields in Europe and Japan are hitting ten-year highs; the 10Y German yield broke above its post-pandemic trading range, to a 15-year high of 3.1%, France’s 10Y yield is drawing near 4% (a 20-year high), and that of Japan was at 2.4% (nearly 30-year high).

There were also huge swings in Hungary’s FX and bond markets, but overall, the forint and the bond market held up well. The MNB’s Monetary Council left its key interest rate at 6.25%, as expected, but raised its inflation forecasts and signalled its commitment to achieving the inflation target. In Hungary, interest rate hike expectations remained strong; the market is pricing in 100 basis point higher interest rates on a one-year horizon (essentially the market expects the same increase from the Czech National Bank and 75-basis-point hike from the National Bank of Poland). Although the forint weakened by half a percent on Friday, it appreciated by 0.75% over the past week, whereas the Czech (CZK) and Polish (PLN) currencies slightly depreciated. Hungary’s 3Y and 5Y bond yields rose by 5-10 basis points on Friday and by 10-20 basis points last week but yields on 10Y and longer maturities moved sideways; the 10Y yield closed near 7.3%, while Poland’s yields rose to a lesser extent week/week and Czechia’s yields grew markedly.

Today’s highlights

Asia’s stock markets fell as investors braced for a protracted Gulf conflict that is already pushing oil prices to near-record monthly growth, causing an inflation shock and raising the risk of recession for much of the world. The Nikkei (-3.2%) and the Kospi (-3.0%) were in the red, while the SSEC was seen inching up.

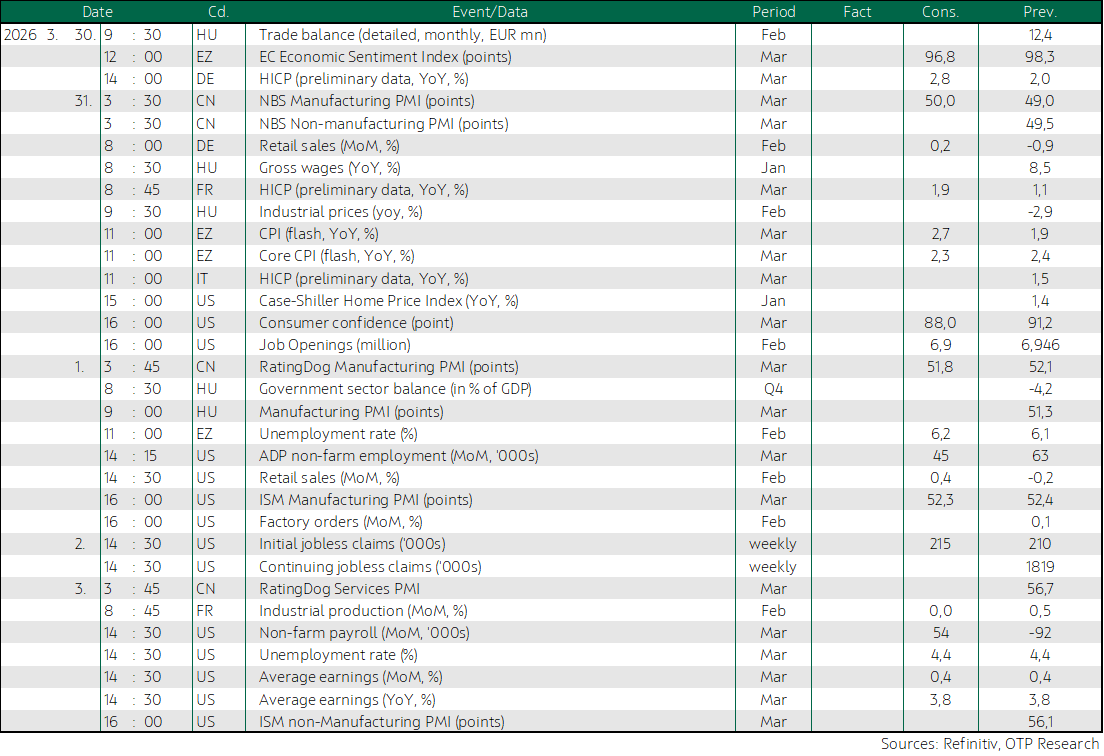

Today, Germany’s inflation data and the eurozone’s sentiment index, as well as Hungary’s foreign trade data will be released. Later in the week, the market will watch eurozone inflation. If our calculations based on weekly fuel prices are correct, headline inflation may have jumped significantly, from 1.9% in February to as much as 2.7-2.8%. The increase is almost exclusively due to fuel prices’ growth, as diesel prices soared 28% and gasoline prices by 15% in a single month. On the other hand, core inflation is expected to remain at 2.4%. In the USA, labour market data will be in focus; the labour market report for March may follow the pattern: the large expansion in January was followed by a marked drop in February – now non-farm payrolls may rebound again, although the forecast figure (around 50,000) is significantly lower than the 200,000 reading typical for peacetime or the 100,000 gain seen in recent years. Hungary releases the 2025 balance of the government sector. Elsewhere, Pakistan has indicated that it was ready to host US-Iran negotiations.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more