OTP Morning Brief: Geopolitics were in focus on Tuesday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

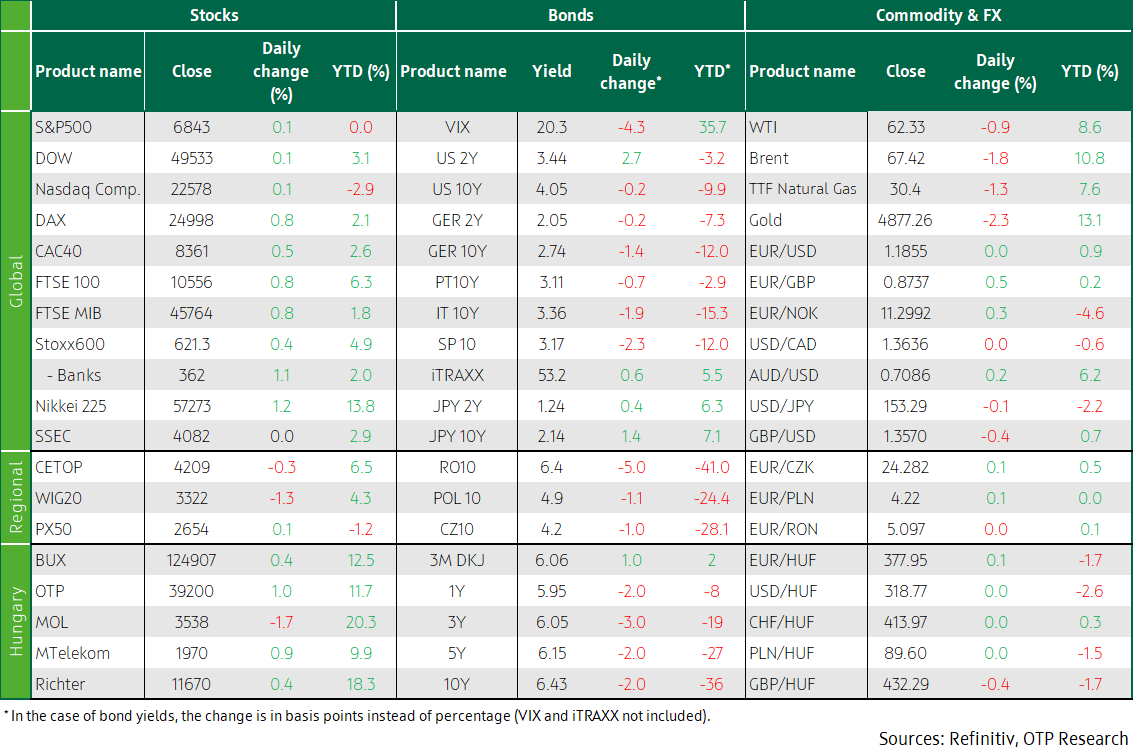

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Geopolitical events were in focus on Tuesday:US-Iranian and Russian-Ukrainian talks were held in Geneva. Europe’s leadingstock indexes rose on Tuesday. US indexes edged higher after the bank holiday. Softwarecompanies remained under pressure. Oil, gold, silver, and copper prices all fellyesterday. Long-term bond yields fell markedly in Japan. The bond yields of Europeand the USA barely changed yesterday.

Europe’s leading stock indices rose on Tuesday

On Tuesday, geopolitical events were in focus: the USA and Iran held talks in Geneva to resolve nuclear program disputes, while US-brokered Ukraine-Russia peace talks continued, also in Geneva. Of Europe’s major stock indices, the STOXX 600 (+0.45%), the DAX and FTSE 100 (+0.8% each), and the CAC40 (+0.5%) all closed higher. The banking sector (+1.3%) extended Monday's gains, picking up from the pressure of the previous two weeks. Healthcare stocks recovered 1.4%, and the real estate sector index increased by 1.8%. Energy stocks fell 0.6% as Brent crude slid more than 1%, while the materials sector shrank 1.6% on weaker gold, silver and copper prices.

Continuing a trend that began in September 2024, unemployment in the United Kingdom rose again. The 5.2% rate in December 2025 is only 0.1 percentage point shy of the peak hit during the Covid pandemic. The rise in unemployment has been accompanied by a further slowdown in wage dynamics: annual wage growth slowed to 4.2%, from 4.6% in November. The data reinforces expectations that the Bank of England may cut interest rates as early as next month. On Monday, investors almost fully priced in a two 25-basis-point interest rate cuts by the end of 2026, as concerns about inflation were replaced by fears about the labour market and the broader economic outlook.

The February reading of Germany’s ZEW economic sentiment index, at 58.3, indicated decline from the previous month, wrong-footing analysts who had expected further improvement after two months of increases. The data suggest that Germany’s cautious recovery is still fragile.

Continuing Monday’s 3.4% slump, MOL's share price slipped 1.7% on Tuesday, with significant turnover. There are several factors behind the fall: crude oil supplies on the Barátság (Friendship) pipeline halted on 27 January, so the oil company has already requested the release of strategic reserves from the government, and has also started purchasing seaborne shipments. However, the Croatian party indicated that transporting Russian offshore crude oil via the Adriatic oil pipeline was not possible. From a technical perspective, profit-taking following the rally from late December to early February is also keeping Mol's share price under pressure. Despite Mol's decline, BUX rose by 0.4% on Tuesday. Czechia’s PX50 also inched up 0.1%, while Poland's WIG20 eased by 1.3%.

US indices rose slightly on the day of reopening

Having reopened after Presidents’ Day, US markets nudged higher on Tuesday. Technology stocks have rebounded from previous lows, helping the S&P500 information technology sector gain 0.5%, after recovering from a 1.5% intraday decline, as gains in Nvidia (+1.2%) and Apple (+3.3%) offset declines in Microsoft (-1.1%) and Oracle (-3.8%). As investors continue to worry about how AI is disrupting traditional business models in some sectors, software companies remained under pressure; the S&P500 software Index slipped 1.6%. Financials were among the best performers, supported by Goldman Sachs (+1.2%) and JPMorgan (+1.5%). Consumer staples (-1.5%) was the worst performer.

In individual names, Masimo skyrocketed 34.2% after Danaher said it would acquire the manufacturer of non-invasive pulse oximeters for USD 9.9 billion. Danaher shares fell 2.9% on the news. Stocks in Fiserv shares jumped by 6.9% after a report by the Wall Street Journal that activist investor Jana Partners had bought a stake in the payments service provider. Norwegian Cruise Line shares advanced 12.1% as activist investor Elliott built a more-than-10% stake in the company. Diplomatic talks were busy in Geneva on Tuesday. The morning began with US-Iranian talks led by Steve Witkoff and Jared Kushner. As the US has built up a large naval force in the Middle East and Iran has begun military exercises in the Strait of Hormuz and partially blocked it, the talks have focused on Iran's nuclear program and sanctions imposed on the Persian country. The US wants to extend the scope of the talks to non-nuclear issues, particularly to Iran's missile program. However, Iran is only willing to negotiate restrictions on its nuclear program in exchange for sanctions relief. According to Iranian Foreign Minister Abbas Araqchi, ‘guiding principles’ have been agreed upon, but this does not mean that an agreement is imminent. Araqchi's words have eased war concerns and sent oil prices down: Brent (-1.8%) and WTI (-0.9%) prices sank. In the afternoon, US-brokered Russian-Ukrainian talks took place, where territorial issues may have been discussed.

Japan’s long-term bond yields fell noticeably

Although Japan’s long-term bond yields fell markedly from their previous decade-long peaks – the ten-year one sank by almost 10 basis points –, bond yields in Europe and the USA barely changed. The 10Y US yield closed slightly above 4%, and the German one near 2.75%. Although the dollar's exchange rate against the euro temporarily strengthened to 1.18, the EUR/USD eventually returned to its previous breakout level, 1.185, where it had closed on Monday.

Trading in the CEE region’s currency markets was also uneventful: the zloty (PLN), the koruna (CZK), and the forint (HUF) barely moved. The Hungarian currency remained close to its strongest in the past two years: the EUR/HUF hugged the 377.5 mark. Hungary’s benchmark bond yields sank further from one-year lows: the 10Y bond yield is drawing closer to 6.4%. In the auction of three-month discount Treasury Bills, the healthy demand prompted the ÁKK to sell 50% more Treasury bills than the HUF 30 billion it had offered; the average yield was 6.07%.

Today’s highlights

In the Asia-Pacific region, the stock markets of China, Hong Kong, and South Korea were closed on Tuesday, to celebrate Lunar New Year holidays. Heading into the close, Japan’s Nikkei was seen gaining 1.3%.

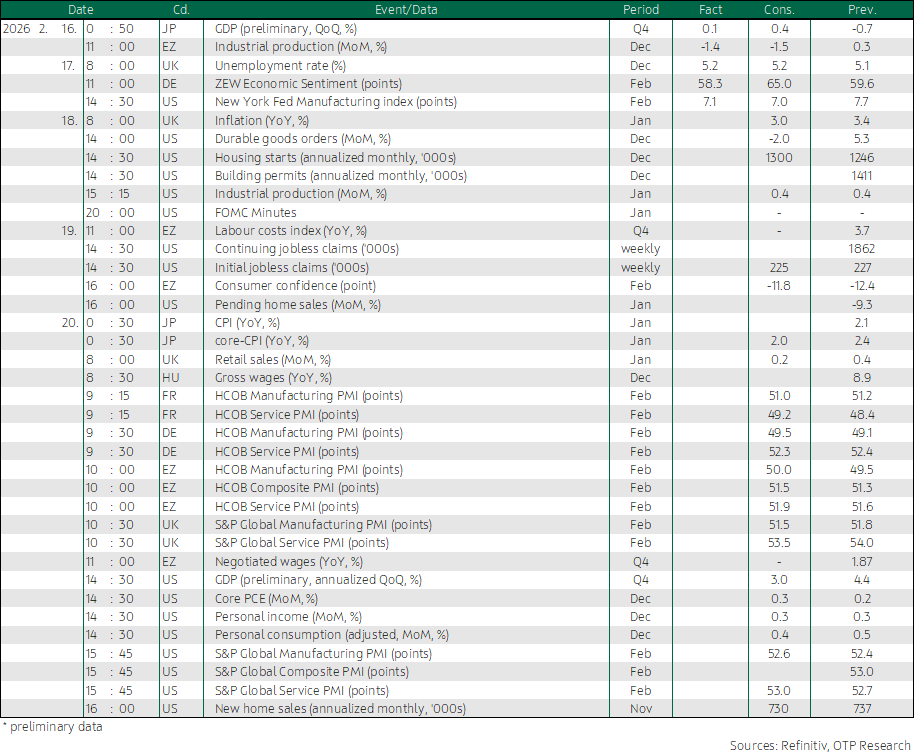

Today, the United Kingdom will release January inflation data, and the USA publishes December data for durable goods orders , housing starts, and building permits. Industrial production data for January and the minutes of the FOMC rate decision will also make interesting readings.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more