OTP Morning Brief: Mixed Investor Reaction to Delayed Labor Market Data

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

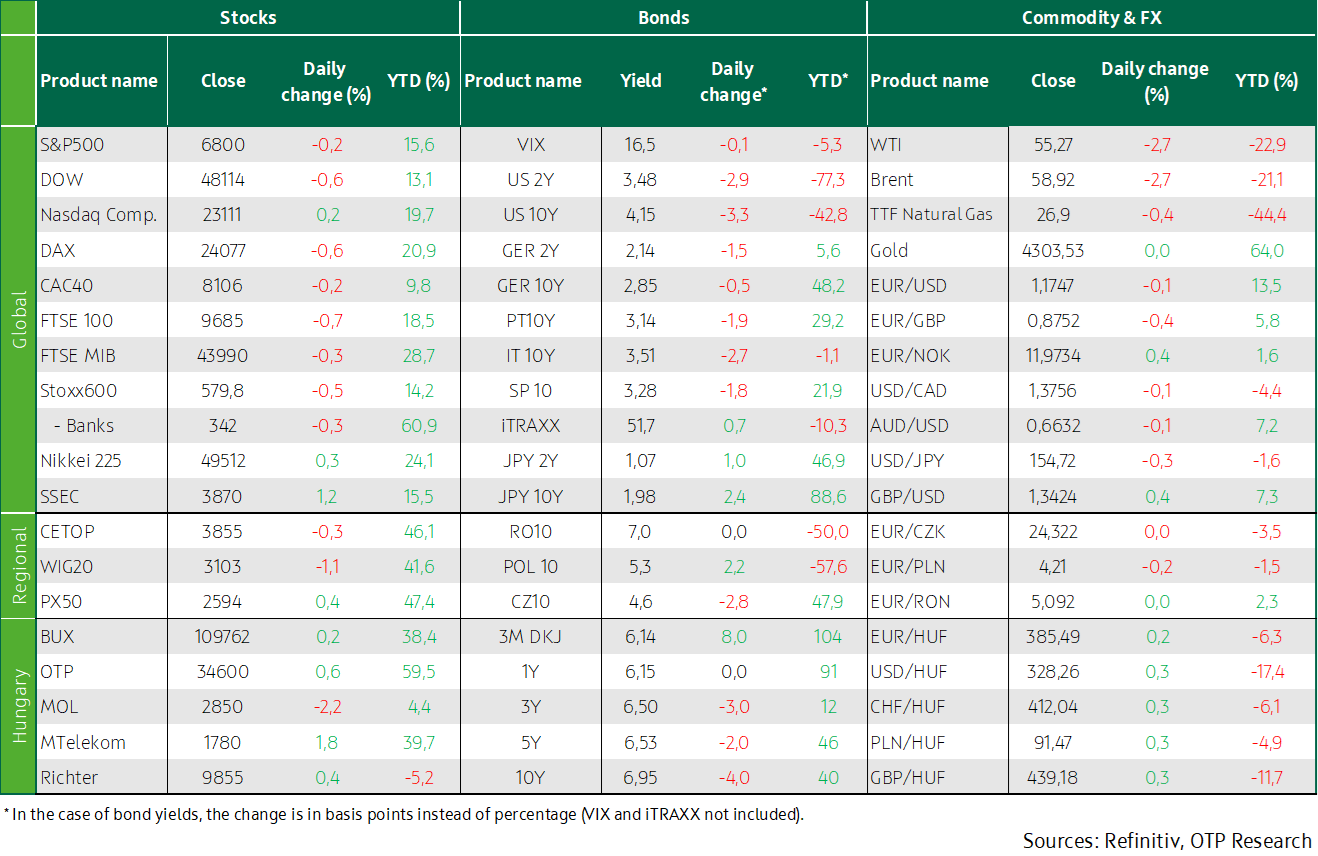

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

European Defense Sector Weakens Tuesday; Eurozone December PMI Misses Expectations. U.S. Investors React Mixed to Labor Market Data, Driving Lower Developed Market Yields. MNB Keeps Rates Unchanged; Trump Orders Blockade of Venezuelan Oil Tankers; Asian Markets Advance.

The European Defense Sector Declined on Tuesday, December PMI Data in the Eurozone Fell Short of Expectations

After early-week gains, European equities corrected lower on Tuesday, with the Stoxx 600 down by 0.5%. Investors’ attention remains on Thursday’s upcoming rate decision, especially after Christine Lagarde indicated that the ECB may once again revise its growth forecast upward in December. One of the day’s underperforming sectors was defense, as the Stoxx Europe Aerospace & Defense index fell 1.8%, with major losers including Sweden’s Saab (–4.8%), Germany’s Rheinmetall (–4.5%), and Renk (–4.3%). The energy sector also had a difficult day, dropping 1.9% due to lower oil prices. Although the automotive sector, down 0.4%, did not perform well either, the European Commission on Tuesday proposed easing the ban on internal combustion engine cars set to take effect in 2035. The plan, which still awaits approval from EU member states and the European Parliament, would replace the current rules with a 90% CO2 emissions reduction target by 2035 and introduce more flexible interim goals, while allowing automakers to offset remaining emissions through alternative fuels and low-carbon materials. Among individual stocks, German online retailer Zalando stood out, rising 4.2%.

Business activity slowed more than expected at year-end, according to December PMI data for the eurozone. The composite index for the region stood at 51.9, missing analysts’ forecast of 53 and falling by nearly one point. This was partly due to a deepening downturn in manufacturing—particularly in Germany—though services also fell short of expectations. Weak German manufacturing was partly offset by France’s PMI, which rose to 50.6 from November’s 47.8, beating forecasts, though its services sector also showed weak performance. In contrast, Germany’s ZEW economic sentiment index rose sharply in December to 45.8, well above expectations (38.5). Component data suggest improvements in the automotive industry and other export-oriented sectors.

Central and Eastern European indices were mixed yesterday: the BUX and Prague indices posted modest gains, while the Polish market fell 1.1%. In Hungary, MOL dropped 2.2%, tracking international energy companies, though this was offset by gains in the other three blue chips.

Mixed Investor Reaction to Delayed Labor Market Data

U.S. benchmark indices showed a mixed picture on Tuesday: the Nasdaq rebounded by 0.2%, while the S&P 500 slipped 0.2% and the Dow fell 0.9%, as investors assessed the Federal Reserve’s monetary policy outlook for next year based on delayed economic data releases. Eight of the S&P 500’s eleven major sectors closed in negative territory, led by energy stocks with a nearly 3% drop. The healthcare sector weakened by 1.3%, partly due to Pfizer falling 3.4% after signaling challenging prospects for 2026 amid declining COVID product sales and narrowing margins, while Humana closed 6% lower following an announcement of upcoming leadership changes.

After a significant delay, October and November U.S. labor market reports were released, indicating further cooling. In October, 105,000 jobs were lost, primarily due to 162,000 positions eliminated in federal government employment, while November saw 64,000 jobs added—slightly above analysts’ expectations. Meanwhile, the unemployment rate unexpectedly rose from 4.4% to 4.6%, and wage growth slowed from 3.7% to 3.5%. U.S. retail sales stagnated in October compared to September 2025, after the previous period’s 0.1% increase was revised downward, missing forecasts for a 0.1% gain. Finally, the preliminary S&P Global U.S. composite PMI fell to 53 in December—a six-month low—down from 54.2 in November.

Brent crude futures dropped 2%, approaching $59 per barrel, the lowest level since early 2021. Market pressure is being amplified by expectations that a potential resolution of the war in Ukraine could ease restrictions on Russian oil flows, as well as demands from Venezuela’s trading partners for lower prices in exchange for heightened risk. At the same time, Chinese economic data continues to signal persistent weakness, further dampening demand outlooks.

Developed Market Yields Decline on Labor Market Data, MNB Keeps Rates Unchanged

Yesterday, following weak U.S. labor market figures and softer-than-expected European PMI readings, yields edged lower: the U.S. 10-year fell to just above 4.15%, while the German equivalent dropped below 2.85%. The dollar weakened, with EUR/USD initially rebounding to 1.18 before stabilizing slightly above 1.175.

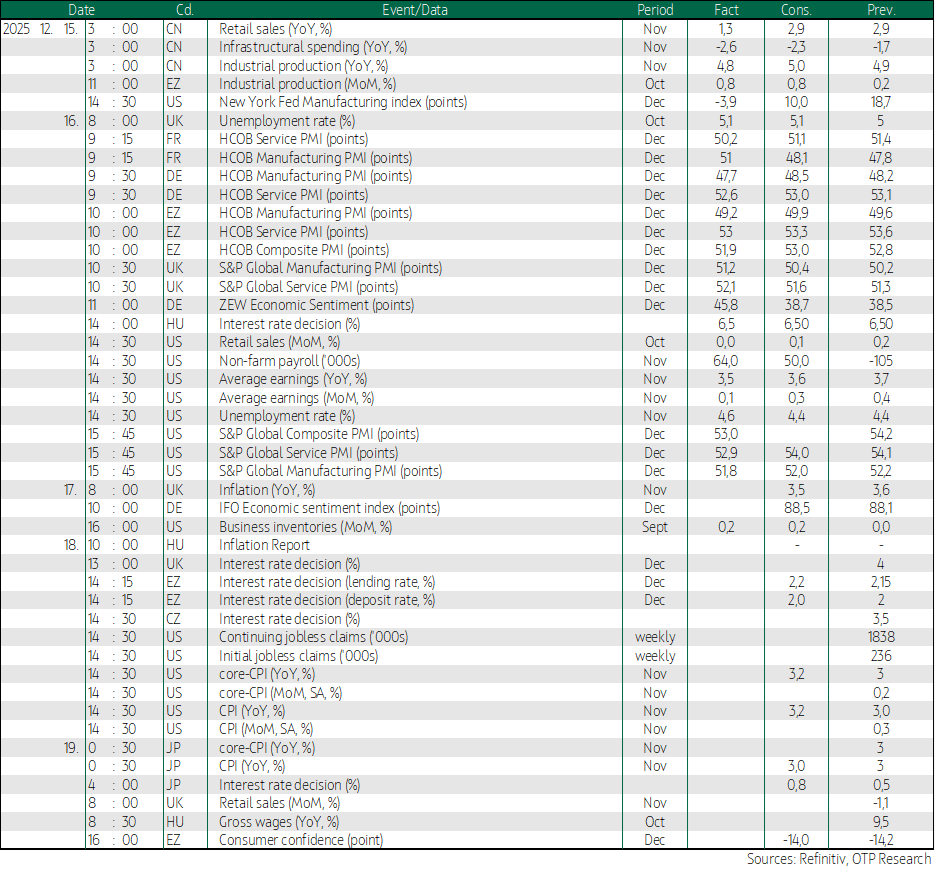

The Monetary Council of the Hungarian National Bank held its December policy meeting yesterday and presented key forecasts from the updated Inflation Report. The base rate remained at 6.5%, in line with expectations. The revised projections indicate lower growth and inflation for this year and next: GDP is expected to rise by 0.5% in 2025 (down from 0.6%), 2.4% in 2026 (previously 2.8%), 3.1% in 2027, and 2.7% in 2028. Inflation is forecast at 4.4% this year (vs. 4.6%), 3.2% in 2026 (vs. 3.8%), and 3.3% in 2027 (vs. 3.0%). Alongside the lower inflation outlook, the central bank emphasized that future decisions on the base rate will be made on a meeting-by-meeting basis, depending on inflation trends and financial stability—signaling the possibility of rate cuts. Following the announcement, the forint weakened moderately, moving from 384 to above 385.5. In the bond market, yields fell by 3–4 basis points until reference rates were set, and by an additional 4–5 basis points after the decision, with the 10-year yield dropping to 6.9%. At the ÁKK’s three-month discount bill auction, demand was exceptionally strong: against the announced HUF 20 billion offering, bids were six times higher, and ÁKK accepted HUF 60 billion. The average auction yield was 6.14%.

Today’s highlights

Global stock markets posted solid gains on Wednesday, despite U.S. employment data failing to bring any meaningful shift in interest rate expectations, leaving investors waiting for new guidance. China’s CSI300 blue-chip index rose 0.6%, while the Shanghai Composite and Hang Seng each gained 1.0%, and Japan’s Nikkei added 0.3%. In China, AI chipmaker MetaX Integrated Circuits debuted in Shanghai with a nearly 600% surge, underscoring the country’s push to accelerate listings of domestic chipmakers and reduce reliance on U.S. firms.

Early Wednesday, oil prices reversed their decline after U.S. President Donald Trump ordered a “blockade” of all sanctioned oil tankers leaving or heading to Venezuela on Tuesday evening. This marks Washington’s latest move to pressure Nicolás Maduro’s government by targeting the country’s main revenue source, lifting oil prices by about 1%.

Today, attention will turn to Germany’s Ifo business sentiment index and November inflation data from the United Kingdom.

The ÁKK will offer six-month discount bills worth HUF 20 billion, while the switch auction will allow investors to acquire 2031/A and 2033/A bonds in exchange for securities maturing next year.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more