OTP Morning Brief: Investors breathed a sigh of relief as crude oil prices fell on Monday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

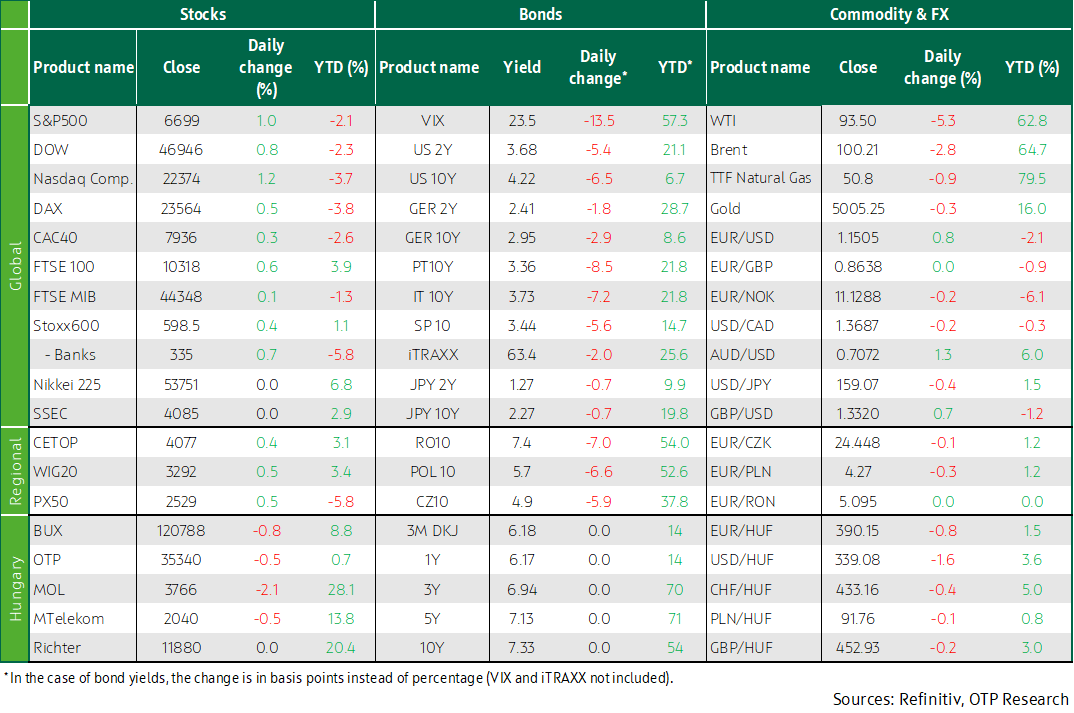

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Several tankers safely passed through the Strait of Hormuz over the weekend, easing fears about the strait being closed for a longer period; oil prices fell on Monday. As a result, global inflation fears eased, allowing investors to breathe a sigh of relief. The Stoxx600 rose and US stock indices also closed about 1% higher. Despite the benign external sentiment, the BUX weakened further. The long-term yields of developed economies’ bond markets decreased, the USD weakened. Hungary’s long-term yields fell sharply; the EUR/HUF sank below 390. Australia’s central bank raised interest rates today. The Fed's two-day interest rate decision meeting begins today. Today, the ZEW economic sentiment index and US housing market data will in the focus of attention, in addition to news from the Middle East.

Europe’s stock markets heaved a sigh of relief as crude oil prices fell, but the BUX extended losses

Western Europe’s stock exchanges opened this week higher; the leading indices recorded small gains at the end of Monday's trading. Erasing the morning’s slight losses, the Stoxx600 (+0.4%), the DAX (+0.5%), and the FTSE100 (+0.6%) closed higher. The sentiment on stock markets improved as concerns about the war in Iran and the closure of the Strait of Hormuz have abated. Investors’ attention shifted to this week’s central bank meetings, where the market does not expect interest rates to be changed, but policymakers will have an opportunity to outline how recent events will affect their outlook, giving market participants a new hint for building their positions. Of the Stoxx600 sector indices, the real estate and energy sectors posted the biggest shifts. Morgan Stanley upgraded its investment recommendation for European real estate companies from Underweight to Neutral. Stock market sentiment was also boosted yesterday by Goldman Sachs’ announcement that it had revised up its year-end target price for the FTSE100.

In individual stocks, Commerzbank’s price jumped by 9% following a bid by Italy’s UniCredit to increase its stake in the German bank. UniCredit’s share price did nut budge. Shares in Amplifon dived 14% after the Italian hearing aid maker announced plans to buy Denmark's GN Store Nord's similar business for EUR 2.3 billion. Oil companies fared well on the London Stock Exchange, despite a drop in crude oil prices.

The Prague (+0.5%) and Warsaw (+0.6%) stock exchanges benefited from the positive sentiment, but Hungary’s benchmark index fell further. The BUX (-0.8%) was dragged down by Mol (-2%) and 4iG (-4%); OTP and MTelekom slipped 0.5% each, while Richter closed flat.

Crude oil prices fell on reassuring news, giving a boost to US stock markets

America’s major stock indexes closed almost 1% higher on Monday as the sentiment improved owing to a sharp drop in oil prices, following reports that, despite the blockade, tankers were able to pass through the Strait of Hormuz over the weekend. The Dow (+0.7%), the S&P100 (+1%) and the Nasdaq Composite (+1.2%), and the Russell2000 (+0.9%) mid-cap index all gained yesterday. Investors returned to their preferred field, artificial-intelligence-related companies. Meta jumped 2.3% following a Reuters report that it was cutting at least 20% of its workforce. Nvidia increased by 1.6% after CEO Jensen Huang introduced new components at the company's annual developer conference. Foxconn, a Taiwanese company that uses Nvidia chips to make AI servers, published a strong quarterly earnings outlook on Monday. Tesla advanced 1.1% after CEO Elon Musk said the company’s Terafab AI chip manufacturing facility would start production within a week. Micron Technology Inc. jumped nearly 4% after the memory chip maker said it planned to build a second manufacturing plant in Taiwan.

All of the S&P500 eleven sector indices rose, particularly technology (+1.4%), and consumer discretionary (+1.3%). Wall Street’s “fear index,” the CBOE VIX Volatility Index, shed 3.5 points, back to 23.7. Travel stocks Delta Air Lines and Norwegian Cruise Line surged 3.5% and 5.1%, respectively, benefiting from lower oil prices. Discount store chain Dollar Tree rallied more than 6% after signalling it could benefit from favourable tariffs in the short term.

The February reading of US industrial and manufacturing output in came in slightly better than expected. The data released yesterday showed 0.2% MoM increase, slightly topping expectations for a 0.1% uptick. In contrast, the New York Empire State manufacturing index fell sharper than thought and entered negative territory.

Oil prices fell sharply on Monday as several tankers safely passed through the Strait of Hormuz over the weekend, easing fears of a prolonged closure of the strait and raising hopes that the route could reopen soon. India is negotiating the safe transit of six more ships, while several countries are holding unofficial talks with Iran to ensure the safe passage of their ships. The USA is allowing Iran to continue shipping crude oil through the Strait of Hormuz, while US President Donald Trump has called on other countries to support efforts to protect trade in the strait. Reportedly, a direct communication channel between the USA and Iran has also been established.

The TTF natural gas price fell below 51 EUR/MWh.

Falling oil prices eased global inflation fears, bond yields declined, and the USD weakened. Hungary’s long-term yields also fell sharply, the EUR/HUF sank below 390

Given that a few ships passed through the Strait of Hormuz, oil prices slumped; tensions and global inflation fears eased, bond yields dropped, and the US dollar weakened. The ten-year US bond yield sank below 4.25% and the German one below 2.95%, both declining by about 5 basis points from the levels seen at the end of last week. Ending a massive appreciation in the previous two weeks, the dollar weakened by nearly 1% against the euro yesterday, sending the EUR/USD above 1.15.

The improving global sentiment had its effect on Hungary’s foreign exchange and bond markets. The forint strengthened by nearly 1% versus the euro, pushing the EUR/HUF below 390. Bond yields declined, the 10Y bond yield dropped by 3-5 basis points at the belly of the curve, and by 10-15 basis points, to less than 7.25% for 10Y maturities and beyond. At the ÁKK’s switch auction, discount Treasury bills worth HUF 20 billion changed hands yesterday.

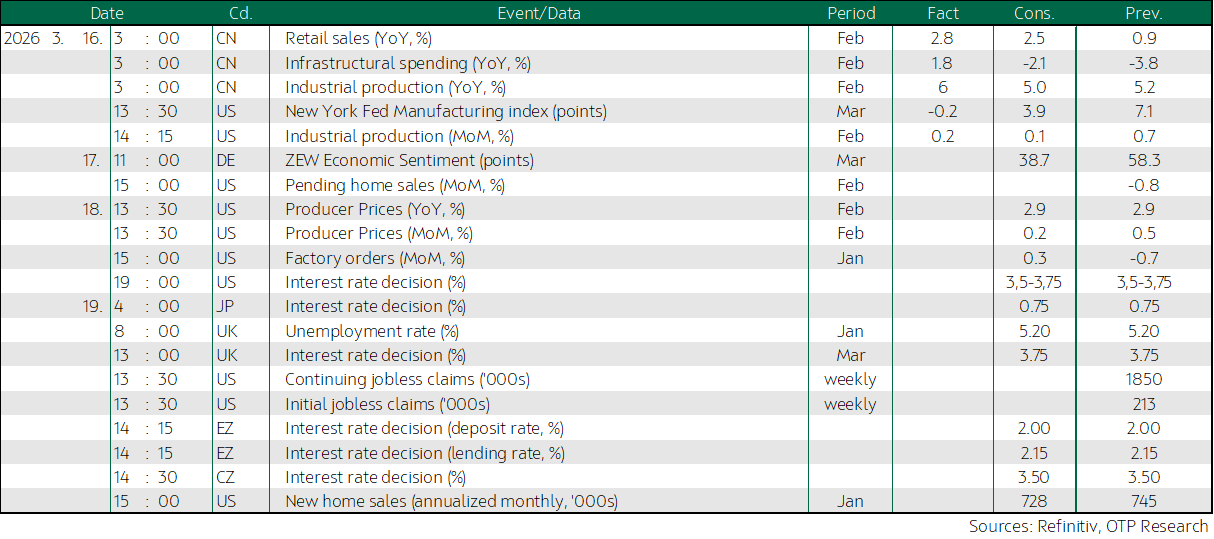

Today’s highlights

This morning's trading shows a mixed picture for Asian stock markets. In the last hour of today’s trading, the Nikkei (-0.3%), the Shanghai Composite (-0.5%), and the CSI300 (-0.4%) were all in the red. But the Hang Seng inched up, and most Korean indices were up 1-2% on Tuesday morning.

This morning, Brent crude rebounded 3.4%, trading above 103 USD/barrel as several US allies rejected Donald Trump's call on Monday to send warships to escort tankers through the Strait of Hormuz. Reuters reported that Iran's Revolutionary Guards (IRGC) had arrested ten foreign nationals accused of spying in the country's northeast, the semi-official Tasnim news agency reported on Tuesday.

Today the Reserve Bank of Australia raised interest rates at its policy meeting, for the second time this year. The benchmark rate rose to 4.1%, but the 5-4 vote is close enough to cast doubt on the bank's next move.

Today the Fed begins its two-day policy meeting, at the end of which it is widely expected to leave its benchmark interest rate on hold. According to data collected by LSEG, traders have pushed back their expectations for a rate cut of at least 25 basis points to October, compared to the previous expectation of a rate cut in July. According to the CME FedWatch Tool, interest rate futures are pricing in a 99.1% probability that the FOMC will decide to hold interest rates on Wednesday.

Today’s important publications are Germany’s ZEW economic sentiment index and the latest data on US pending home sales.

In Hungary, the ÁKK auctions 3M discount Treasury Bills, offering HUF 30 billion debt.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more