OTP Morning Brief: Western Europe’s stock markets hit new highs again

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

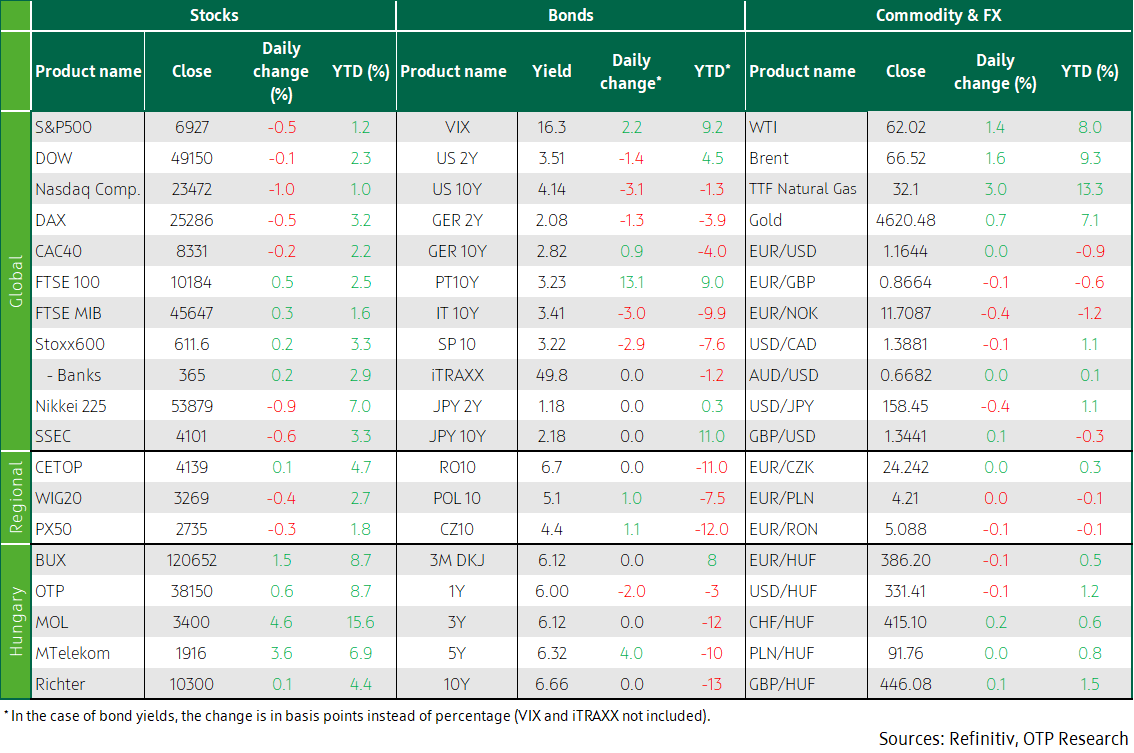

Western Europe’s stock markets and Hungary’s BUX hit new highs, MOL soared yesterday. Amid banks’ mixed earnings, Wall Street’s leading indices fell, despite stronger-than-expected retail sales data. Bond yields barely changed on Wednesday. Crude oil prices rose for the fifth day on fears of a possible US military strike against Iran. Gold and silver prices broke to new highs again. Detailed data on Hungary’s industrial output, industrial production statistics from the eurozone, and Germany’s GDP data are scheduled for release today.

Western Europe’s stock markets and Hungary’s BUX hit new highs again, MOL soared yesterday

Most stock markets in Western European closed at new highs on Wednesday, driven mostly by gains in the chemical and healthcare sectors, but bank stocks also went to new highs. The STOXX Europe 600 closed 0.2% higher, with chemicals (+2%) leading sector gains. EMS Chemie (+8%) and was among top earners of the STOXX index as UBS had upgraded the Swiss chemical company’s shares to Buy, from Hold. Chemical companies were also among the biggest winners in America’s S&P index. Shares in Orion skyrocketed 12%, to its highest since October, as the Finnish drugmaker’s 2026 revenue forecast has beaten expectations. AstraZeneca surged 2.4% a day after it said it had agreed to buy the Boston-based Modella AI; this helped the healthcare sector increase by 1.3%.

The UK’s FTSE100 and Italy’s FTSE MIB went up; the former also hit a new high, while France’s CAC40 and Germany’s DAX declined. The latter ended its longest winning streak in more than a decade on Tuesday. The DAX (-0.5%) was dragged down by tech stocks such as SAP and Infineon. Meanwhile, traders digested the bankruptcy of luxury department store conglomerate Saks Global, whose creditors include Gucci owner Kering and the world's largest luxury conglomerate LVMH as unsecured creditors. Paring earlier gains, luxury stocks ended down 0.3%.

Investors also watched geopolitical developments in Venezuela and Iran, which weighed on commodities markets, but mining stocks also rose 1.8%. Defence stocks fell 1.6%, snapping eight consecutive days of gains. Among energy companies, RWE (+2.3%) and SSE (+2%) soared as they had won guaranteed power price contracts in the UK's latest offshore wind auction, which secured record capacity.

In the benign sentiment in Western Europe, the CEE region’s stock markets and Hungary’s BUX extended their gains, helping both the CETOP and the BUX close at new highs. The growth was fuelled by MOL’s 4.6% surge yesterday, partly benefiting from speculations about the acquisition of Serbia’s NIS, and the rise in oil prices. Hungary’s other three blue chips also achieved gains (MTelekom: 3.6%, OTP: 0.6%, Richter: 0.1%) yesterday.

Wall Street’s leading indices fell amid mixed bank results, despite stronger-than-expected retail sales data

US stock markets fell on Wednesday, led by the Nasdaq (-1%), as technology stocks were ailing as investors sought defensive sectors. Banking shares extended their recent losses, owing to mixed quarterly results. The S&P500’s banking index fell 2.1%, to a five-week low, dragged down by Wells Fargo (-5.1%), which missed Q4 profit expectations. Shares in Citigroup (-4.1%) and Bank of America (-4.2%) slumped, even though both have beaten Wall Street's quarterly profit estimates. The financial sector, including banks, which had been on a strong rise in 2025, weakened this week, mainly on concerns that President Donald Trump's proposal to cap credit card interest rates could hurt financial sector profitability. The technology sector led sector losses in the S&P500, while defensive sectors such as consumer staples rose. The Dow (-0.3%), the S&P500 (-0.8%), and the Nasdaq Composite (-1.4%) all closed lower.

Shares of Broadcom, Palo Alto Networks, and Fortinet fell as Reuters reported that Chinese authorities had told domestic companies to stop using cybersecurity software made by American and Israeli companies; this may affect a dozen companies.

According to data released on Wednesday, US producer prices in November matched forecasts, while retail sales data beat them. The latter further reinforced the belief that America’s fourth-quarter GDP growth may have been very strong, despite the government shutdown.

Oil prices rose for the fifth consecutive trading day on Wednesday (1%), on fears of potential disruptions in Iranian supply, fuelled by a potential US attack on Iran and the possibility of retaliation against US regional interests.

Amid geopolitical fears, gold rose to a new high of more than USD 4,600 and silver exceeded USD 90.

Bond yields barely changed on Wednesday

Europe’s bond markets lacked a single direction, while Germany’s 10Y yield inched up and Italy’s 10Y edged lower; the former hovered around the top of its post-pandemic trading range, above 2.8%. The US 10-year yield eased by three basis points, to below 4.15%, after the November reading of the monthly producer price inflation figure, which was released late due to the government shutdown, rose as expected. The EUR/USD was little changed, still trading below 1.165.

Zoltán Kurali, the MNB’s Deputy Governor, said at a Financial Times conference in Vienna that both the government and the central bank recognized that inflation was a problem that both organizations were fighting it. His words temporarily strengthened the forint, but the EUR/HUF closed nearly flat. The slow rise in Hungarian bond yields, which began after Tuesday's inflation data release, continued overall, except for the ten-year maturity, which stagnated at 6.66%. There was strong demand at yesterday's auctions of the ÁKK. The agency sold HUF 50 billion forints worth of six-month Discount Treasury Bills (vs the HUF 30 billion on offer), at an average yield of 6.09%. A total of HUF 60 billion worth of bonds changed hands at the switch auctions.

Today’s highlights

Asia’s stock indices were seen sinking today; at one point, China’s SSEC was down 0.6%, and Japan’s Nikkei lost 0.9%. The latter slipped from the new high hit on Wednesday, following recent news that Japan’s Prime Minister may call early elections in February, to give the government the necessary authority for a fiscal stimulus. Western Europe’s index futures inched up trivially, while America’s indices were near-stagnant. The price of WTI gave back more than 3% from yesterday's rise.

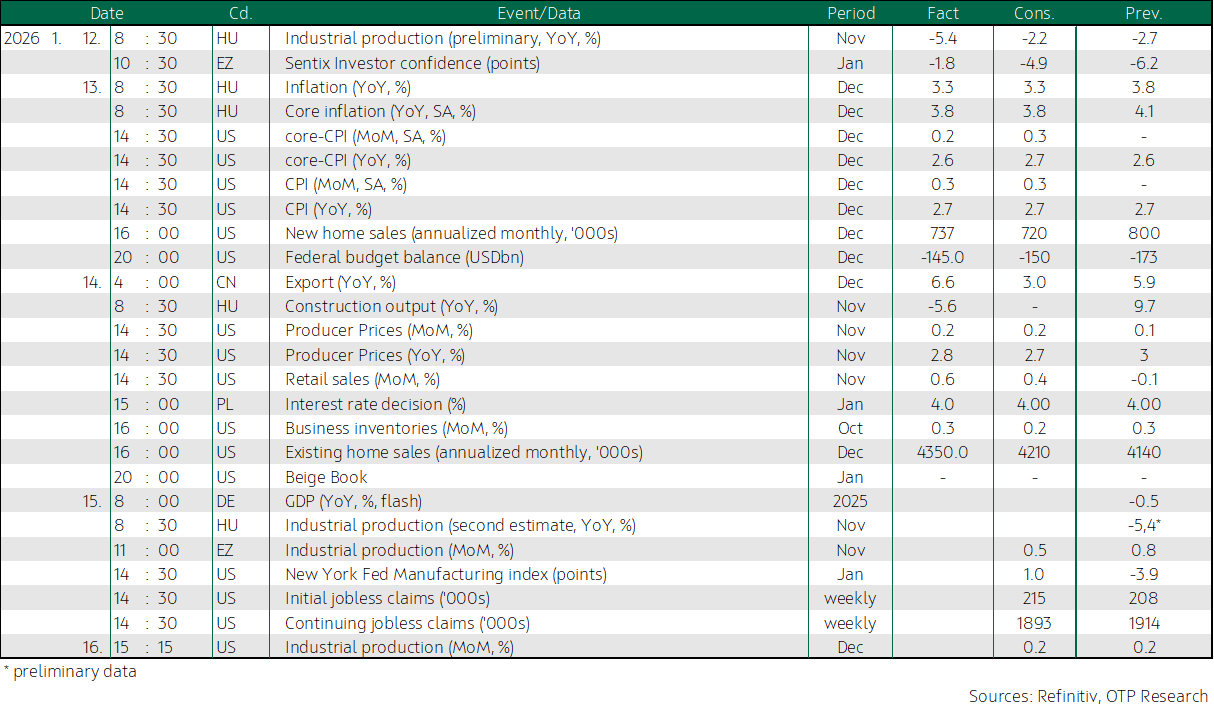

The eurozone’s industrial production statistics, and Germany’s GDP data for 2025 are scheduled for release today. As the earnings season continues, a new round of big American banks (Goldman Sachs, Morgan Stanley) will release their reports today. Hungary publishes detailed data on industrial production, and the ÁKK auctions 12M discount T-Bills, as well as 10Y and 15Y bonds worth HUF 30, 30, and 10 billion, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more