OTP Morning Brief: Earnings and geopolitical tensions drove markets on Tuesday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

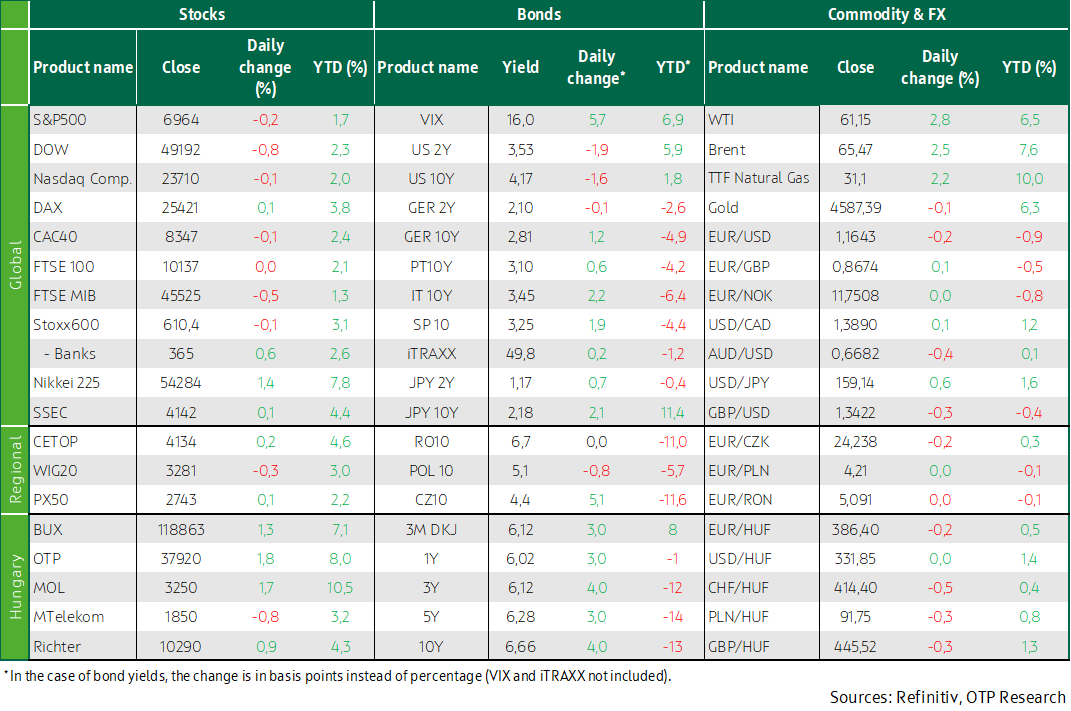

Most of the key stock exchanges in Europe and the USA closed Tuesday's trading in the red. The BUX outdid its regional peers; its main engine OTP hit new high. In Hungary, inflation was 3.3% in December, in line with market consensus. December’s US inflation data were reassuring. Gold and crude oil prices marched higher. Hungary’s benchmark bond yields rose by 2-6 basis points. The forint has regained some lost ground from the euro. November’s producer price index and retail sales data, and the Fed's new Beige Book will be released in the USA today. The earnings season is picking up steam.

Tuesday's trading ended with trivial changes on Western Europe’s leading stock exchanges

In Western Europe, the leading indices closed with tiny, mostly negative changes on Tuesday. Germany’s DAX stood out with an uptick, fuelled by a 1.9% rise in Airbus after the company reported a 4% take-off in the number of aircraft delivered last year. Having had set a record high at one point on Tuesday, the Stoxx600 eventually closed 0.1% lower. The losses was led by the construction sector, following a 7.7% fall in shares of Rockwool after Russia ordered temporary administration over two of the Danish company’s Russian subsidiaries. Meanwhile, Danish offshore wind developer Orsted soared 5.4%, thanks to a US court ruling that the company can press ahead with its USD 5 billion project, which the Trump administration had suspended in December.

Hungary’s BUX (+1.3%) was the top performer in the CEE region. MTelekom was its only its blue chip to close in the red, while OTP went to a new all-time high.

Wall Street’s leading indices declined yesterday; December’s inflation data were reassuring

America’s stock exchanges dropped on Tuesday, largely dragged down by the financial sector, after JPMorgan executives expressed concerns about Donald Trump's proposal to impose a 10% cap on credit card interest rates for one year. This has intensified the selling wave seen in the financial sector in recent days. Visa and Mastercard also lost roughly 4% each, and shares in JPMorgan (-4.2%) also plunged even though the bank reported better-than-expected quarterly profit. Delta Air Lines descended as the company’s 2026 profit forecast missed analysts’ forecasts.

US headline inflation was flat at 2.7% year-on-year in December, in line with consensus, while core inflation eased to 2.6%, a better reading that than the market had expected. However, items that go into the core PCE index came in higher than thought, so there could be an upside surprise. The incoming data did not overwrite interest rate expectations: the market is pricing in a total of 50-basis-point rate cuts by the end of 2026, and almost unanimously expects rates to be held at the January meeting. At the same time, tensions around the Fed continue to simmer: in response to the investigation against Jerome Powell, the heads of the world's leading central banks issued a joint statement, standing up for central bank independence and standing by Chairman Powell.

Geopolitical tensions fuelled the rise in crude oil prices after President Trump promised help to Iranian protesters and cancelled planned meetings with Iranian officials.

Japan’s bond yields picked up again; Hungary’s inflation was 3.3% in December

On Tuesday, the bond markets of advanced economies started trading with yields rising due to the repeated substantial increase in Japanese bond yields - they jumped by seven basis points, to above 2.16%, the highest level since 1999. However, this later reversed when favourable US inflation data were released: the US 10Y yield closed below 4.2% again. In the eurozone, yields upped by a few basis points; Germany’s 10-year yield is back above 2.8%. The dollar strengthened slightly, pushing the EUR/USD below 1.165.

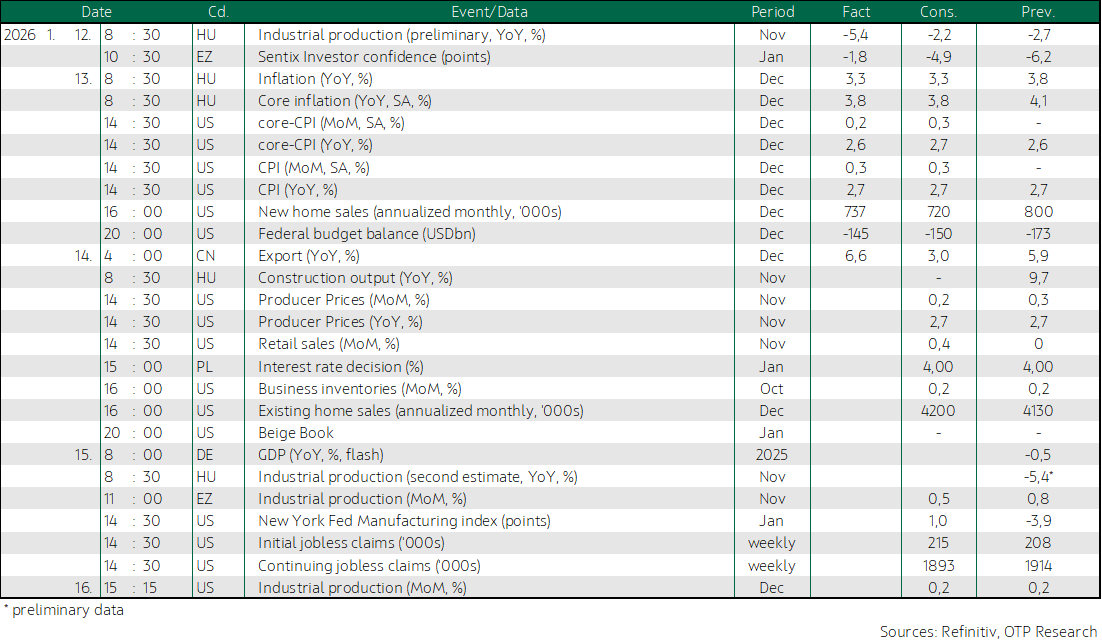

In Hungary, headline inflation fell to 3.3%, core inflation sank to 3.8%, in line with market consensus, but services inflation rose, to which the MNB added that corporate repricing remained strong. After the inflation data release, interest rate cut expectations slightly eased, the forint strengthened (the EUR/HUF closed trading at 386), and benchmark bond yields rose by 2-6 basis points. The 10Y yield rose to 6.65%, yet this is considered low compared to its typical trading range in the past almost a year. Amid healthy demand, the ÁKK accepted bids worth HUF 40 billion (vs offered: HUF 30 billion) at yesterday's auction of three-month discount Treasury Bills, at an average yield of 6.11%.

Today’s highlights

Asia-Pacific stocks traded mixed this morning. Japan’s indices went to new highs on expectations that Prime Minister Takaichi Sanae could call a snap election in February. She has been a proponent of looser monetary policy and has announced a massive economic stimulus package, which markets have welcomed.

The yen weakened, pushing the USD/JPY below 159, its lowest since July 2024, when Japan’s authorities intervened to stop the yen's depreciation.

Silver’s price broke above USD 90 for the first time, bringing its year-to-date gain to more than 25%. Meanwhile, gold’s rally continued; it has gained more than 7% this year.

In Hungary, the ÁKK is offering six-month discount T-bills worth HUF 30 billion, and at the switch auction, investors can obtain 2032/A and 2034/A bonds worth HUF 10 billion each, in exchange for securities maturing next year. Hungary’s KSH statistical office publishes construction production data for November.

In the USA, November’s producer price index and retail sales figures, as well as the Fed's new Beige Book will be released.

The earnings reports season continues with figures from Bank of America, Wells Fargo and Citigroup, among others.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more