OTP Morning Brief: Brent traded above USD 100 again

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Western Europe’s stock markets extended losseson Thursday. Markets prices imply 25-basis-point ECB rate hike by July. Iran's supreme leader vowed to keep the Strait of Hormuz closed. Iran attacked tankers in the Persian Gulf. TTF natural gas price surged 2.5%, trading above EUR 50 again. Brent jumped above USD 100 on Thursday. US stock indices fell sharply yesterday. US 10-year yield upped another 5 basis points, above 4.25%. The EUR/USD dropped 0.5%, closer to 1.15. Investors remained concerned about USprivate credit. The USA releases January core PCE , and the UoM consumer sentiment index for March.

Western Europe’s markets extended losses on Thursday

Western Europe’s markets fell deeper on yesterday. The STOXX 600 (-0.6%), Germany’s DAX (-0.2%), France’s CAC40 (-0.7%), and the FTSE100 (-0.5%) all slipped. Apparently, investors worried about the resurgence of oil prices amid the Middle East war, which has brought inflation fears back to the fore. Financial markets now price in a 25-basis-point ECB interest rate hike by July as expectations took a U-turn: before the Middle East conflict, interest rates cuts were anticipated. The energy price shock of 2021/2022 is still fresh in the minds of policymakers and investors; at that time, major central banks overlooked energy price increases for more than a year, believing they were temporary; then they were forced to belatedly hike interest rates sharply.

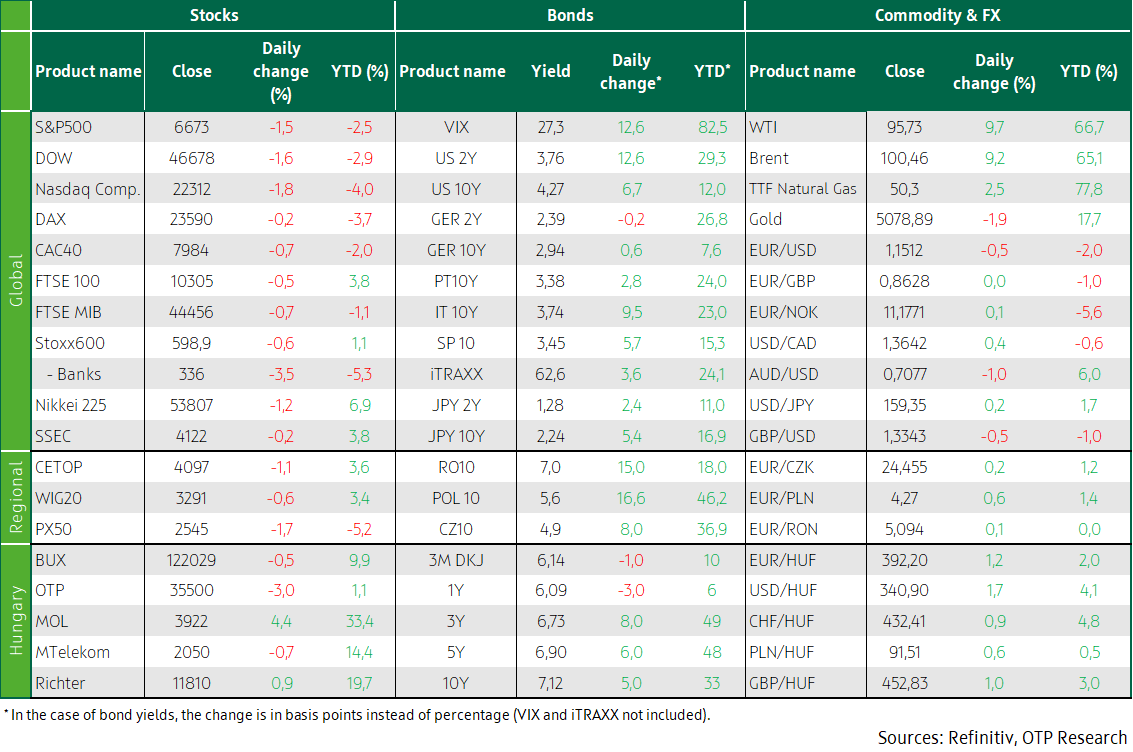

Banking stocks (-3.5%), which are sensitive to economic cycles, saw the sharpest dive but the losses were broad-based. Rising oil prices helped the energy sector gain 1.4%. The defensive utilities sector rose 1.8%. Some positive earnings reports helped pare losses. Leonardo shares took off 5.7%, to a record high, as the defence company said its orders, revenue, and core profit would continue to grow this year. Daimler Truck, which specializes in commercial vehicles, advanced 4.1% after forecasting a stable profit rate for 2026. Zalando jumped 9.5% after the online fashion retailer forecast a growing adjusted operating profit for 2026. Germany's largest electricity producer, RWE said on Thursday that it would begin a more aggressive expansion in the USA, where data centres have significantly boosted demand for electricity. This will also include the construction of new gas-fired power plants. The company's share price soared nearly 4% on Thursday.

Neither could the CEE region’s stock markets avoid losses. Hungary’s BUX declined 0.5%. OTP shares (-3%) were under pressure, while MOL gained 4.4% – both in sync with the banking and energy patterns in Western Europe. Poland's WIG20 (-0.6%) and Czechia’ PX50 (-1.7%) also ended in the red. As expected, Turkey’s central bank left its base rate at 37%. The Western Balkan countries' accession to the European Union may be accelerated by compromises, in which they would give up some of their rights, including their veto power in the European Council.

The price of TTF natural gas added 2.5%, going beyond EUR 50 again.

US stocks closed lower on Thursday

US stock indices fell on Thursday. The S&P 500 (-1.5%), the Dow Jones (-1.6%), and the Nasdaq Composite (-1.8%) all closed in the red. All sectors of the S&P500, except energy (+1%) and defensive sectors like consumer staples (+0.1%) and utilities (+0.7%), posted losses. The decline was primarily driven by negative news about the war in Iran. In his first public speech, Iran’s new Supreme Leader, Mojtaba Khamenei, vowed revenge and the closure of the Strait of Hormuz. Meanwhile, Iran launched an attack on tankers stranded in the Persian Gulf, using small boats. According to US intelligence, Iran’s leadership remained largely intact, and the regime is not in danger of collapsing, despite nearly two weeks of bombing by the USA and Israel. Although Donald Trump’s message on Monday (that the war had essentially been won) brought relief to markets, the events did not exactly validate this. Thus, Brent jumped above USD 100 again on Thursday, and the price of European-listed TTF natural gas rose above EUR 50. This caused WTI (+9.7%) and Brent (+9.2%) skyrocket in a single day. US Energy Secretary Chris Wright said that the Navy was unlikely to be able to provide escorts for commercial ships passing through the Strait of Hormuz before the end of March. In response to the events, China banned the export of refined fuels in March with immediate effect. The USA has also issued a 30-day sanctions waiver, allowing countries to buy Russian oil and petroleum products currently stranded at sea under sanctions. As of Thursday, about 124 million barrels of Russian crude oil were at sea worldwide, enough to replace the volume lost from the Middle East for five to six days.

Investors continue to watch US private credit developments with concern. This involves loans that are provided not directly by commercial banks, but by funds or other institutional investors outside banking regulations, typically to corporate clients. One of the concerns is that the lending clientele is heavily represented by software companies whose operating models are threatened by the rise of artificial intelligence. The recent liquidity crunch in private equity funds has forced several major players — including Morgan Stanley and BlackRock — to limit redemptions after some funds reached the 5% redemption level that traditionally allows such action. The Federal Reserve’s vice chairwoman for supervision, Michelle Bowman said that capital requirements for big banks will be reduced slightly in a review of capital requirements rules. The weekly US jobless data were in line with expectations.

The US 10Y yield jumped by another five basis points, above 4.25%

The attacks on tankers passing through the Strait of Hormuz and Iran’s statements threatening Middle East energy infrastructure have pushed oil prices up by another 10%, to around USD 100, further increasing tensions in bond and currency markets. The US ten-year yield jumped another 5 basis points, surpassing 4.25%. Germany’s ten-year yield inched up trivially, remaining below 2.95% – yet this marks a three-year high, and is at the top of the post-pandemictrading range. The dollar was further strengthened by demand for risk-freeassets; the EUR/USD sank another half a percent, to close near 1.15.

The CEE region’s currencies have weakened. The koruna (CZK) shed 0.2%, the zloty (PLN) lost 0.4%, and the forint (HUF) depreciated by 1.2%; the latter traded at 392 against the euro. The sentiment in Hungary’s bond market remained depressed. Due to weak demand, only half of the planned HUF 20 billion worth of 12M discount Treasury Bills were sold at yesterday’s auction, at an average yield of 6.16%. There was subdued demand for the 15Y bond too; the ÁKK sold the amount on offer, HUF 10 billion, at an average yield of 7.18%. On the secondary market, benchmark yields grew by 5-8 basis points, the 10Y bond yield exceeded 7.1%.

Today’s highlights

Asia’s markets were also seen in the red in the last hour of trading. Japan’s Nikkei (-1.2%), Korea’s KOSPI (-1.7%), Hong Kong’s Hang Seng (-0.5%) and China’s SSEC (-0.2%) were all set to lose.

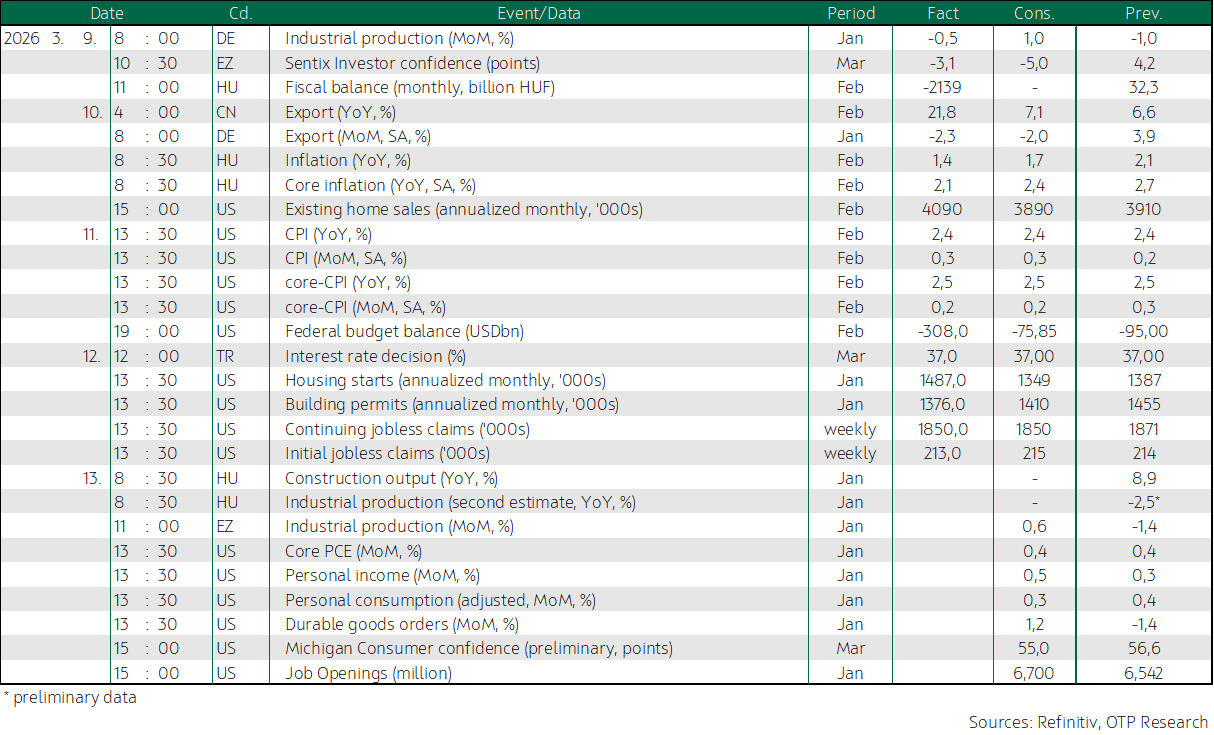

Today Hungary’s KSH statistics office publishes January construction production data and the second (detailed) estimate of industrial output. Elsewhere, the eurozone’s industrial production data for January will be released. On the other side of the Atlantic, the January core PCE indicator will see the light of day; based on the producer price index, it may show a strong 0.4% MoM dynamic, similarly to the December gauge; but the January consumer price index suggests otherwise. The January readings of personal income and consumption, durable goods orders, and the job openings statistics will also be published in the USA, as well as the University of Michigan's consumer confidence index for March.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more