OTP Morning Brief: The major stock indices declined on Thursday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The UK’s Q4 growth was weaker than hoped, British shares weighed on the Stoxx. Poland’s economy expanded dynamically. US indices fell. Donald Trump rolled back climate change policies. Investors sought bonds amid growing risk aversion. In Hungary, January inflation was lower than feared. Asia’s stocks echoed Thursday’s downward trend in the West. Today’s most important release is America’s CPI.

UK Q4 growth missed expectations, British stocks weighed on the European index, Poland’s economy grew dynamically

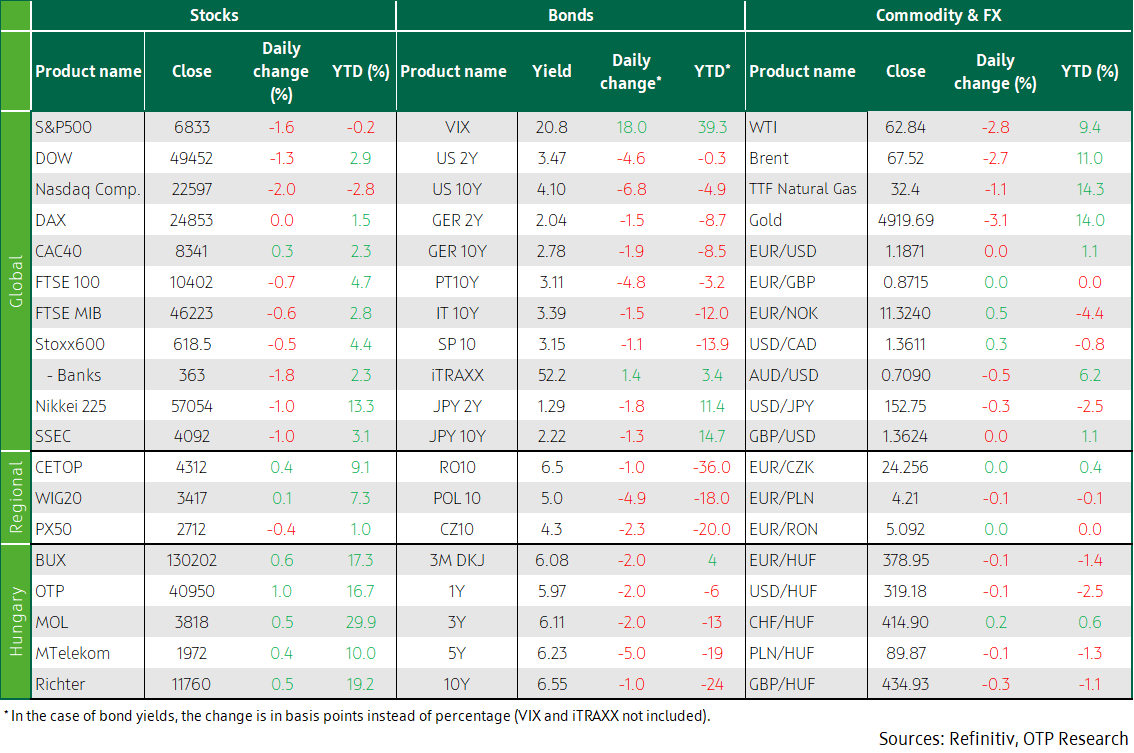

The stock markets of Europe painted a mixed picture on Thursday: France's CAC 40 added 0.3%, Germany’s DAX ended flat, while the UK's FTSE100 (-0.7%) dragged down Stoxx index (-0.5%). One reason for the weakness of the British market may have been the UK’s pale economic performance in the fourth quarter, when it rose by just 0.1% QoQ, whereas economists had projected 0.2% increase. The annual growth rate was 1.0%. The positive performance of the manufacturing industry was offset by the still ailing construction industry, while services stagnated for the first time in two years.

At sector level, telecommunications (+1.9%) and food (+1.8%) increased, while banking fell 1.8%. France's Sanofi replaced its CEO Paul Hudson, who is leaving after six years mainly because of slowing innovation and anti-vaccination pressure from the USA, with the relatively lower-profile Belén Garijo, head of Merck KGaA; the move sent shares down nearly 4.2%. Siemens shares jumped vigorously during the day, then reversed slightly, to end Thursday trading with 0.3% gain; its earnings report printed stronger-than-expected quarterly results on robust demand for its AI-driven data centre infrastructure, thus the giant raised its full-year profit guidance. French luxury goods giant Hermes (+2.6%) reported a 9.8% surge in sales, amid a stagnant luxury goods industry.

On Thursday, China cut import duties on more than USD 500 million worth of EU dairy products; in the final decision of an 18-month anti-dumping investigation launched in response to the EU’s tariffs on electric vehicles from China. The new duties on dairy products from the EU, ranging from 7.4% to 11.7%, will be in effect for five years from today, 13 February 2026, replacing the 21.9% to 42.7% rates in a preliminary decision made in December.

The sentiment in the CEE region was also mixed: Czechia’s PX index sank 0.4%, Poland’s WIG upped 0.1%, and Hungary’s BUX rose by 0.6%. In Budapest, the strongest blue chips was OTP (+1%), but the other three also increased by about half a percent each. Poland’s economy expanded by 1.0% on a quarterly basis, thus achieving 4.0% annual growth rate, the highest since Q3 2022.

America’s indices fell, Donald Trump revoked further climate change regulations

US indices fell as investors increasingly dumped technology stocks and fled transportation companies following AI-related news. According to a report by CNBC, the Algorhythm Holdings AI company could increase the efficiency of freight transportation, thereby narrowing the market. The Dow (-1.3%), the S&P500 (-1.6%) and the Nasdaq (-2.0%) all fell . Although the early trading session was heading higher, stock indexes turned back as investors abandoned riskier sectors and sought more defensive categories such as utilities (+1.5%), consumer staples (+1.3%) and real estate (+0.3%). Shares of Cisco Systems slumped 12.3% on Thursday after the networking equipment giant reported a lower-than-expected quarterly gross margin due to the crowding-out effect of AI companies. Shipping company C.H. Robinson nose-dived 14% for the above-mentioned reasons. Shares in Palantir slid almost 5%, bringing their year-to-date loss to more than 27%.

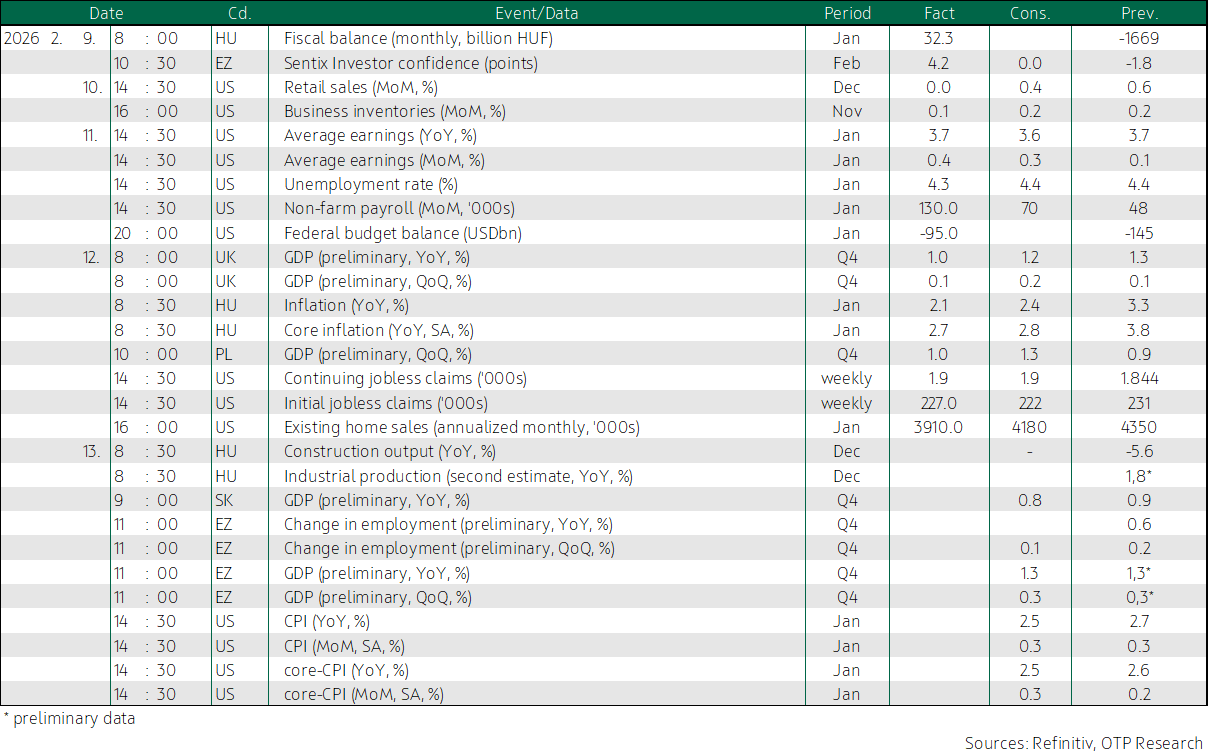

Last week, US jobless claims fell slower than expected but disruptions caused by winter storms continued to have an impact. Initial jobless claims dropped by 5,000, to 227,000 in the week ended 7 February, whereas analysts estimated the latter at 222,000. In the USA, existing home sales shrank by 8.4% in January, to a more-than-two-year low of 3.91 million. The tight supply has pushed up prices, and the decline likely reflects the contracts signed in November and December. On Thursday, Donald Trump announced that he would end federal greenhouse gas emissions requirements for all vehicles and engines, thereby rejecting scientific finding that greenhouse gases are harmful to human health. Separately, ’border czar’ Tom Homan said that President would halt a much-criticized wave of deportations in Minnesota.

Oil prices fell on Thursday owing to weakening demand, easing tensions in the Middle East, and expected supply increases. Brent (-2.71%) crude futures closed at 67.5 USD/barrel, while WTI (-2.77%) ended the day at USD 62.8.

Investors sought bonds as risk aversion mounted; Hungary’s January inflation came in lower than expected

Following the sharp fall in US equities and precious metals, investors sought shelter in bonds. US bond yields with maturities of three years and beyond have dropped sharply, by 5-8 basis points, and the 10Y yield declined to a two-month low of 4.1%. The eurozone’s bond yields also fell, but to a lesser extent, by 2-3 basis points; the ten-year German Bund yield sank below 2.8%. The dollar barely benefited from the declining risk appetite this time: the EUR/USD dipped 0.1%, to 1.185.

On Thursday morning, Hungary’s markets awaited January inflation data, which came in significantly lower than expected – not only the headline (2.1%) but also core (2.7%) and service inflation, opening the door to an interest rate cut in February. Should February inflation data be favourable, even an interest rates reduction in March may not be ruled out. Immediately after the data release, the forint weakened, sending the EUR/HUF to 381, but later the cross returned to 379, despite the deteriorating sentiment abroad and news that Hungary may lose access to the EUR 12.2 billion EU fund that had already been released. At the auction of 12M discount Treasury Bills, the ÁKK sold the amount on offer, HUF 30 billion worth of T-bills, seeing subdued demand. The average yield was 5.99%. About HUF 35 billion worth of 15Y and 20Y year fixed-interest bonds (2041/A, 2051/G) were sold, amid healthy demand; yield levels were five basis points below Thursday's benchmark yields. Yields inched up by one or two basis points before the benchmark yields were fixed in the early afternoon, but they sank by 1-5 basis points compared to Thursday. The ten-year yield remained slightly above 6.5%.

Today’s highlights

Asia’s stock markets retreated from record highs as concerns about shrinking margins in the tech sector, which has hit companies like Apple, drove investors towards safer government bonds ahead of important inflation data from the USA. The Nikkei and SSEC slipped 1.0% each, while the Kospi descended 0.3%.

In Hungary, a string of macroeconomic data for December will be out today, in the form of industrial production and construction output. In the eurozone, the second estimate of fourth-quarter GDP and employment data will be released. In the USA, the focus will be primarily on the consumer price index; headline and core inflation are both expected to have accelerated by 0.3% month-on-month. However, the sharp jump in US natural gas prices in the middle of the month due to extreme weather conditions, and the increase in food prices due to import tariffs both pose upside risks to the January data. We maintain that the impact of the tariffs will be less severe than previously thought, but it may strengthen price pressures for a few more months, so inflation may remain above the Fed's 2% target throughout the year.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more