OTP Morning Brief: Uncertainty in the oil market continued

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

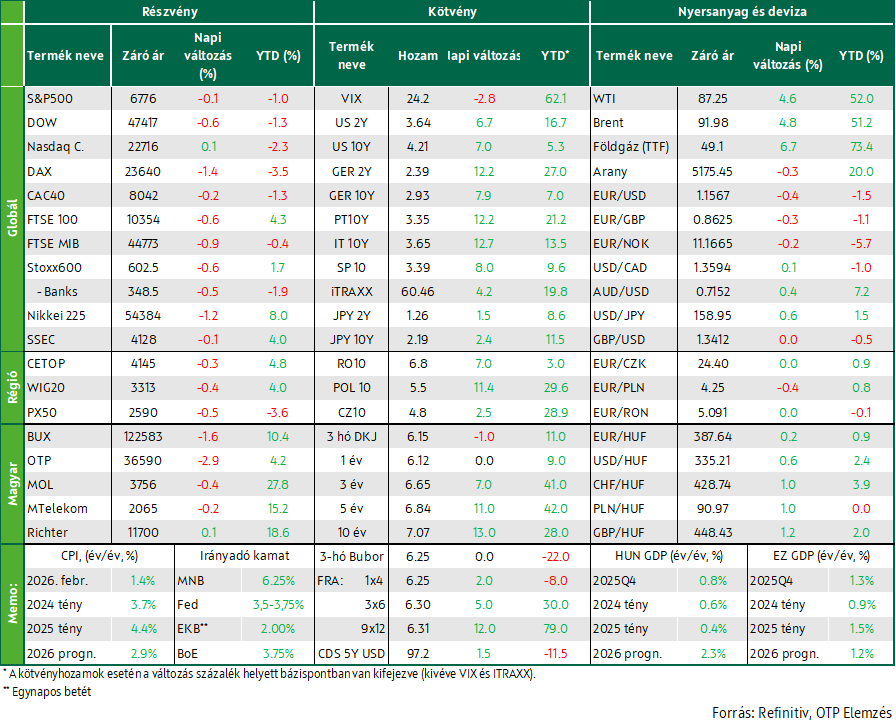

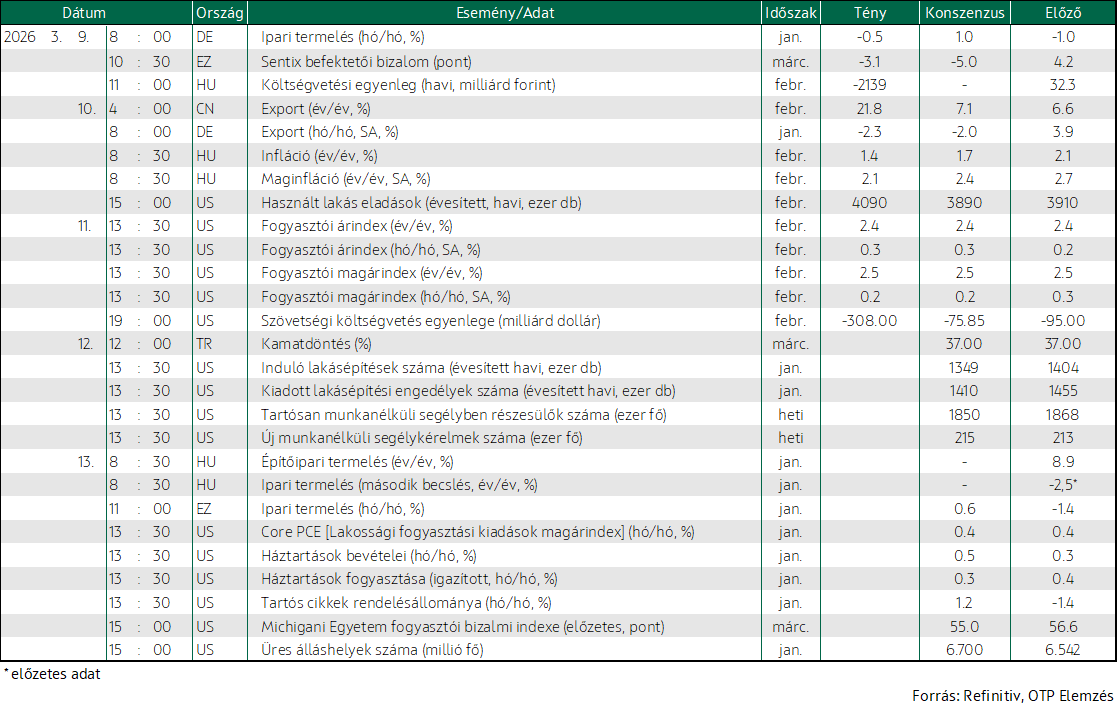

Europe’s indices fell yesterday; IEA decides torelease strategic reserves amid continued uncertainty in the Middle East. America’sindices closed mixed; US inflation in February was as expected; Oracle shares grew sharply. Developed markets’ bond yields rose; the USD strengthened; CEE currencie smoved mixed, the HUF weakened. Today, the US will release housing market data and the weekly jobless claims statistics. Turkey’s central bank holds rate-setting meeting.

Europe’s stocks fell on Wednesday; IEA is to release strategic reserves amid continued uncertainty in the Middle East

Europe’s stock markets declined yesterday. The Stoxx 600 index slipped 0.8%, as investors watched the escalation of military operations in the Middle East. Germany's Rheinmetall reported full-year revenue of EUR 9.94 billion and EUR 1.68 billion profit; despite its potential role in replacing US missile stocks depleted in the Iran war, its shares dived 8%. Porsche, which projected cost-cutting plans and an expansion of its model range after a year plagued by multiple profit warnings in 2025, saw its shares fall 1.2% yesterday. The exception to the negative sentiment was Inditex, which rose 0.5% thanks to strong first-quarter results. The Strait of Hormuz remained blocked, and the IEA has decided to release a record 400 million barrels of oil from its strategic reserves to offset the loss of oil supply. Oil prices grew sharply on the news: Brent jumped by 5.4%. Geopolitical risk was further heightened by the US military's announcement yesterday that it had destroyed Iranian ships, including 16 minelayers, in the Strait of Hormuz area, after Washington called on Iran to immediately remove mines it had laid in the area.

The indices of the CEE region fell, Hungary’s BUX underperformed. Of its blue chips, only Richter eked out gain.

US indices closed mixed; US inflation in February was in line with expectations; Oracle shares rose sharply

America’s stock markets closed mixed yesterday as investors continued to watch developments in the US-Iran war and oil market movements. The Dow Jones Industrial Average slipped 289 points, or 0.61%, to 47,417, the S&P500 shed 0.08%, but the Nasdaq Composite inched up 0.08%. Market analysts said the International Energy Agency’s record 400-million-barrel stock release alone would not solve the risks related to the Strait of Hormuz, especially the logistics of refined products such as kerosene. Adding to the uncertainty was news yesterday of another missile strike on a commercial vessel off the coast of Iran, stoking market fears that oil prices could remain high despite President Donald Trump’s earlier message that the war could end very soon. In the corporate world, Oracle ‘s shares skyrocketed 9% after reporting better-than-expected third-quarter results and a strong revenue outlook for 2027.

In line with market expectations, US annual inflation remained at 2.4% in February. This is the same as the January reading, and marks its lowest since May 2025. Details were mixed: energy prices rose 0.5% (as expected), gasoline prices slowed year-on-year, while diesel and natural gas prices rose. Food and housing inflation were unchanged, in line with forecasts, while used car prices fell. CPI rose 0.3% MoM, also in line with the consensus, but accelerated from 0.2% in January; housing contributed the most to this (+0.2%). Core inflation remained at 2.5% YoY, also in line with expectations, but it slowed to 0.2% MoM, from 0.3% in January.

Developed markets’ bond yields rose; the USD strengthened; CEE currencies moved mixed, the HUF weakened

Although US inflation and core inflation data were in line with expectations, rising tensions in the Middle East and growing oil prices have re-intensified inflation and interest rate hike expectations, especially since President Christine Lagarde said that the European Central Bank would do everything it can to keep inflation in check despite rising oil prices. The market expects at least one interest rate hike from the ECB this year, but even two moves could be in the cards, according to pricing. As a result, Germany’s 10Y Bund yield jumped by almost ten basis points, to around 2.95%, the top of its post-pandemic trading range; it has not been higher in more than three years. French and Italian yields rose by a few basis points stronger. US yields rose milder, still the ten-year dollar yield drew near 4.25%. As investors sought risk-free assets, the dollar strengthened by 0.4% against the euro, sending the EUR/USD to around 1.155.

The CEE currency market turned tables: on Tuesday, the HUF was the only currency to strengthen, but on Wednesday it was the only one to weaken against the euro (EUR/HUF: 388). The sentiment on bond markets was unenthusiastic. At the auction of six-month discount T-Bills, not even a quarter of the planned quantity could be sold, owing to anaemic demand. Interest was relatively stronger at the switch auction, where the planned HUF 10 billion bonds changed hands. Reference yields rose by about ten basis points; the ten-year yield drew near 7.1%.

Today’s highlights

Asia’s indices sank this morning – even though the IEA decided on a larger-than-ever strategic stock release; the measure does not appear to have reassured Asian investors.

Today, the US will release housing data and the usual weekly jobless claims figures. Turkey’s central bank will also hold a rate-setting meeting.

Today, the ÁKK auctions 12M discount T-Bills and 15Y fixed-interest bonds, offering HUF 20 billion and HUF 10 billion, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more