OTP Morning Brief: Upside surprise in US job market data

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

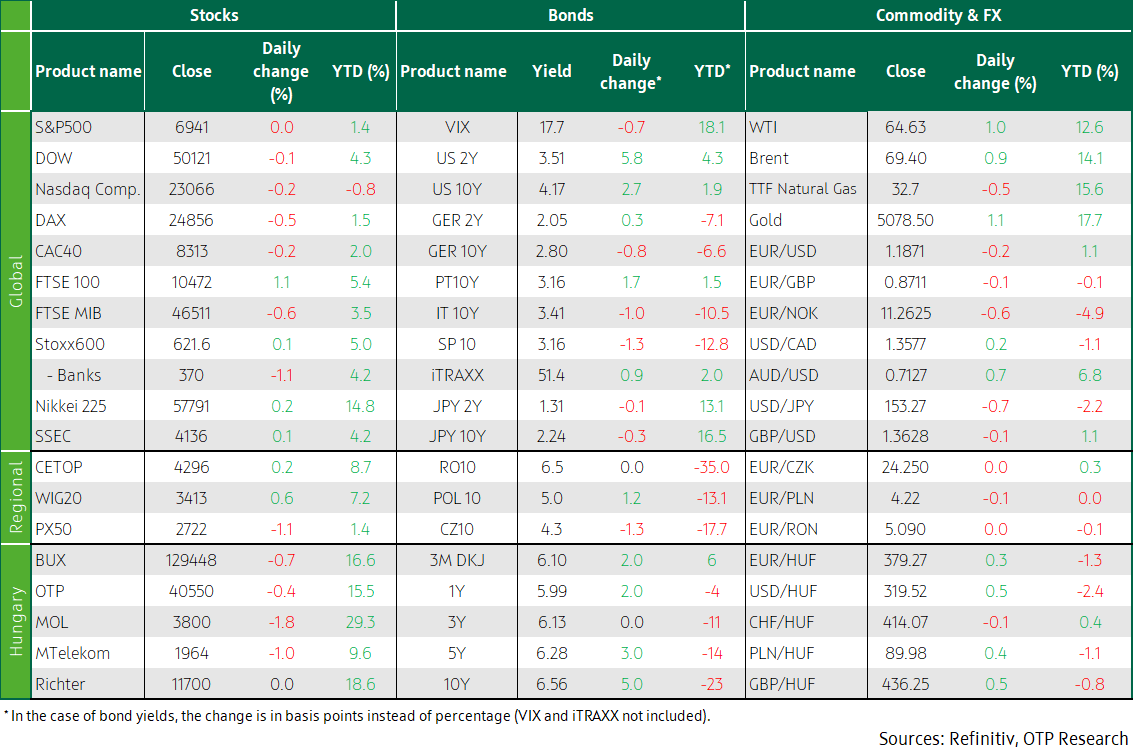

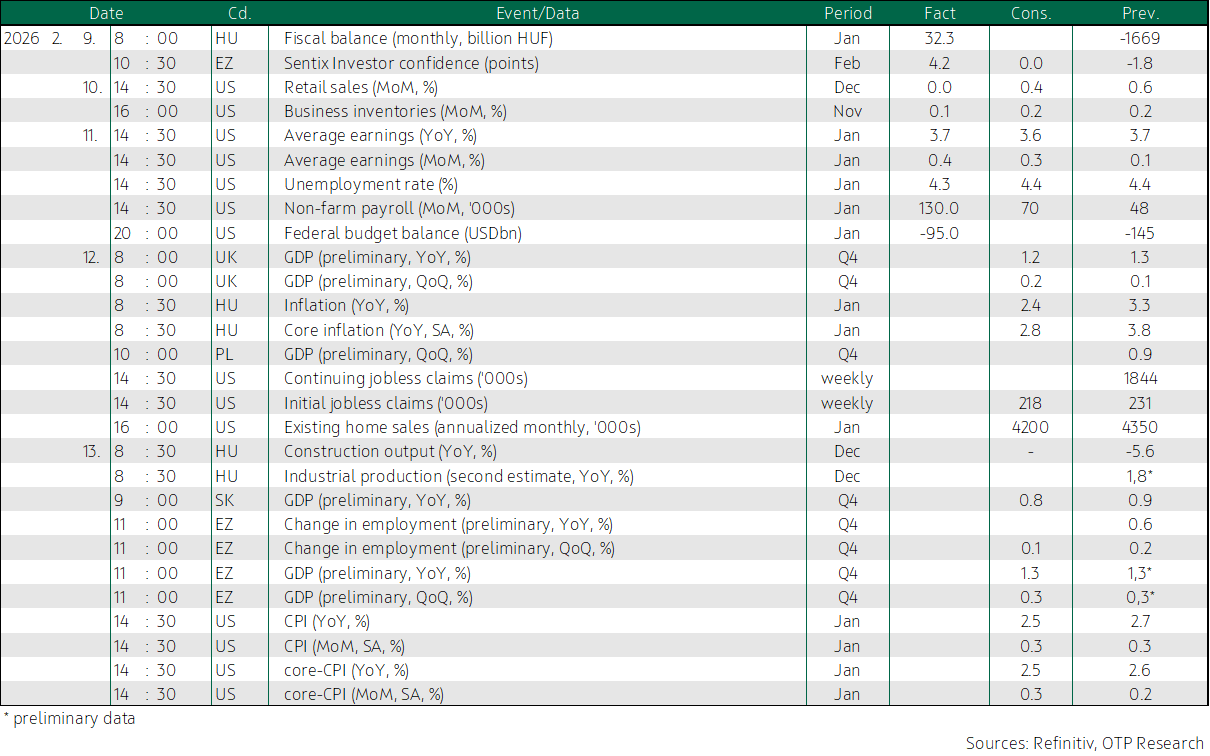

A 0.1% uptick led the STOXX 600 to record high. Technology and media stocks underperformed in Europe. Fears that AI may disrupt traditional companies in many sectors remain strong. In the USA, January job growth beat expectations: NFP grew by 130,000 and unemployment fell to 4.3%. The energy sector fuelled the rise on both sides of the Atlantic. US bond yields shed a few basis points on strong labour market data, yields in Europe were flat. The CBO expects US budget deficit at 5.8% of GDP in 2025 and 2026. Q4 GDP statistics from the UK and Poland, as well as the US jobless claim figures are data to watch today. Hungary publishes the January reading of inflation.

An 0.1% uptick took the STOXX 600 to record high

Having risen by 0.1%, the STOXX 600 closed at all-time high on Wednesday. Germany’s DAX (-0.5%) and France’s CAC40 (-0.2%) declined, while the UK’s FTSE 100 gained 1.1%. Rising oil prices helped energy stocks fuel growth, the sector index jumped by 3.8%. Technology (-1.8%) and media (-2.6%) stocks were the laggards. The latter was hit by sustained strong fears that artificial intelligence could disrupt certain industries, including ‘traditional’ software companies. France’s industrial software developer Dassault Systemes nose-dived 20.8% on Wednesday after reporting a 5% drop in software revenue in the fourth quarter of 2025. Siemens Energy’s net profit nearly tripled in the first three months of the company’s current fiscal year, boosted by AI-driven demand for gas turbines and grid equipment, and thanks to smaller losses at its struggling wind turbine business. Big tech companies plan to spend about USD 600 billion on AI in 2026, creating significant demand for power plants and grid infrastructure. The AI boom has helped Siemens Energy’s share price grow more than tenfold in the past two years; it soared 8.4% on Wednesday.

Heineken, which is looking to replace CEO Dolf van den Brink, said on Wednesday it could cut up to 6,000 jobs from its global workforce of 87,000, in a bid to boost productivity. The company lowered its profit growth forecast from last year, expecting 2%–6% increase 2026, as the Dutch brewery and its rivals face weak demand. Investors welcomed the announcement, the share price shot up 4.4% yesterday. Germany’s Commerzbank said on Wednesday it expected its 2026 net profit to exceed its previous target of EUR 3.2 billion. In 2025, net profit shrank slightly due to restructuring costs but beat analysts’ expectations. Italy’s UniCredit has acquired a 26% stake in the German bank and continues to push for a merger between the two banks, while Commerzbank executives are trying to convince shareholders of the viability of the bank’s standalone strategy. The German government is also opposed to the takeover. Commerzbank’s share price fell 2% on Wednesday.

The European Commission this week approved Volkswagen Group’s request to exempt its Chinese-made all-electric Cupra Tavascan SUV from import duties, in exchange for a minimum price and sales quota. While China had been seeking a collective agreement on tariffs on electric vehicles between its automakers and the EU, Volkswagen’s bilateral deal is a sign that a collective solution is increasingly unlikely.

In the CEE region, Hungary’s BUX lost 0.7% and Czechia’s PX50 fell 1.1%, while Poland’s WIG20 gained 0.6%.

In the USA, January job growth surpassed expectations

The Nasdaq and Dow edged lower on Wednesday, while the S&P 500 closed practically flat.

US jobs report for January came in better than expected. Nonfarm payrolls rose by 130,000, exceeding the consensus forecast of 70,000, and posting the best figure since early 2025. In addition, the annual benchmark revisions were not as negative as many had feared, as the monthly growth estimate for last month, which was originally an average of 49,000, was revised down to a still positive 15,000. Wrong-footing those expecting stagnation, the unemployment rate dropped to 4.3%. Wage growth remained strong, at 3.7% year-on-year in January. Even the average weekly workweek rose from 34.2 hours to 34.3 hours. The latest statistics suggest that the labour market is stable and strong – at a time when data on the US labour market tend to be inconsistent. In terms of the market impact of the data releases, the stronger-than-expected employment data eased concerns about the economy, but reinforced expectations that the Fed may slow the pace of interest rate cuts. Thus, the initial strong gains in all three major stock market indices quickly melted away. Eight of the eleven main sectors of the S&P 500 rose yesterday. Financial services and communication services lost more than 1%, while energy marched 2.6% higher, second to it was the defensive consumer staples sector (+1.4%). The technology sector moved mixed: chipmakers grew sharply while software companies slid, ending three days of gains. The Philadelphia Semiconductor Index soared 2.3%, while the S&P 500 software index slumped 2.6%. Microsoft slid 2.2%, while Alphabet (-2.3%) weighed heavily on communications services index. Brokerage firms, which had already fallen on Tuesday after startup Altruist announced AI-powered tax planning features, weakened further on Wednesday, with Charles Schwab and Ameriprise Financial slipping nearly 4% each and LPL Financial diving 6.1%.

The U.S. budget deficit is expected to rise slightly in 2026, to USD 1.853 trillion, the Congressional Budget Office (CBO) said in a forecast released on Wednesday. The CBO said the deficit in fiscal year 2026 will be about 5.8% of GDP, roughly the same as in 2025. But the U.S. deficit-to-GDP ratio will average 6.1% over the next decade and reach 6.7% by 2036. The CBO forecasts a much slower economic growth than the Trump administration's estimates.

Strong labour market data pushed US bond yields a few basis points higher

China’s lower-than-expected inflation data led to a drop in yields on global bond markets, but stronger-than-expected January US labour market data on all fronts – job creation, unemployment, wages – have turned the tables. In the end, US bond yields upped a few basis points, but the 10-year yield still closed below 4.2%. There was no significant movement in European bond markets, Germany’s 10-year Bund yield remained around 2.8%. The dollar gained strength from the strong labour market data, and the EUR/USD sank below 1.19 by the afternoon.

On Monday, Hungary’s forint strengthened to its strongest since the end of 2023, pushing the EUR/HUF below 377, before the slow reversals (by 0.3% each on Tuesday and Wednesday) drove the cross to 379.5. Hungary’s benchmark bond yields on 5Y maturities and beyond rose by 3-5 basis points, but the 10Y yield is still around its one-year low, slightly above 6.5%.

Investors sought longer-term bonds at yesterday's auctions. At the auction of six-month discount Treasury Bills, the amount on offer (HUF 30 billion) was sold with moderate demand, at an average yield of 6.06%. However, there was hefty demand at the switch auctions, where the ÁKK offered 2033/A and 2037/A bonds worth HUF 15 billion in each, in exchange for securities maturing this year. Bids totalled more than HUF 130 billion, and nearly HUF 100 billion, respectively. The ÁKK did not hesitate to exchange bonds worth HUF 80 billion and 60 billion, respectively, at average yields of 6.34% and 6.63%.

Today’s highlights

Heading into the close in Asia, Japan’s Nikkei upped 0.2%, the KOSPI soared 2.8%, the SSEC added 0.1%, while the Hang Seng sank 0.8%.

Hungary publishes inflation data for January today. We forecast 2.3% year-on-year inflation, thus we expect the index to have fallen well below the MNB's 3% target. January is one of the most significant repricing periods of the year, so January inflation data always carry extra uncertainty. Previously, the MNB indicated that inflation data from the beginning of the year would be crucial in the timing of its easing cycle. Beyond the possibly reassuring headline data, the indicators that better capture underlying processes are also worth checking.

Elsewhere, the United Kingdom and Poland release GDP data for the fourth quarter. In the USA, initial jobless claims will reveal whether the previous week's figure of 231,000 was a one-off spike. The January reading of existing home sales will also come to light in the USA.

In Hungary, the ÁKK auctions 12M discount T-Bills, 15Y, and 20Y fixed-interest bonds (2041/A, 2051/G), offering HUF 30, 15 and 15 billion, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more