OTP Morning Brief: Crude prices fell, but no end in sight to the conflict

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

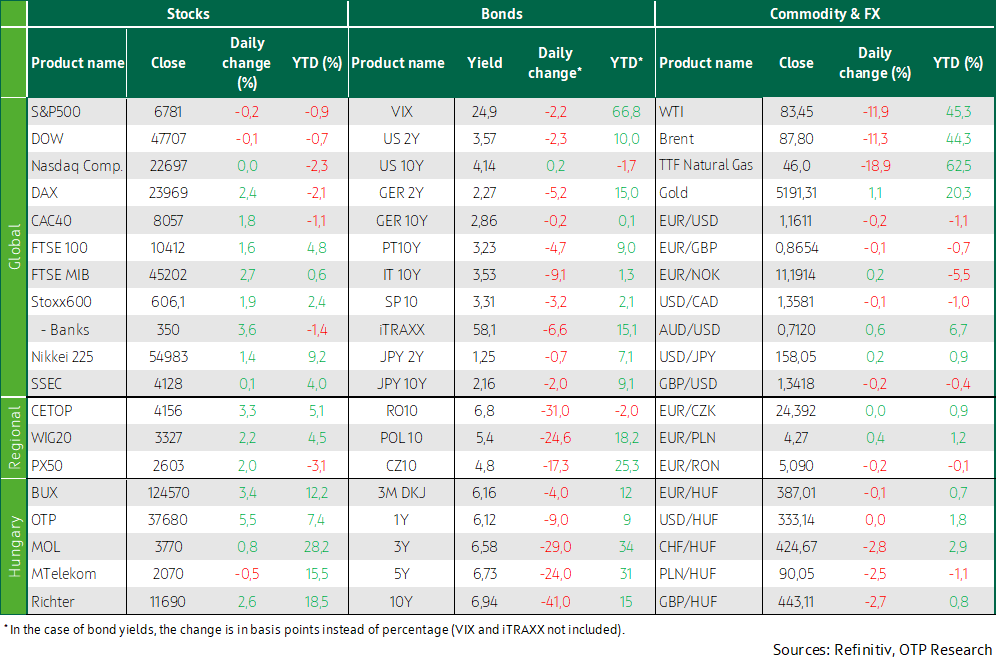

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Iran has reportedly begun to undermine the Strait of Hormuz. On Tuesday, crude oil prices plunged more than 10%, while European TTF natural gas prices fell by nearly 20%. Europe’s benchmark indices ended 1.5-3.0% higher, while Wall Street closed with smaller losses, ending a choppy trading. The CEE region’s stock exchanges rose, the BUX grew by more than 3%. The dollar strengthened against the euro, and the US 10Y yield climbed to 4.14%. The forint’s strengthening pushed the EUR/HUF to 387. As the oil market panic eased, the previously exploding CEE bond yields fell sharply yesterday. Hungary’s February headline inflation unexpectedly fell to 1.4% and core inflation to 2.1%. In addition to the developments in the Middle East conflict, US February inflation data will be in focus today.

Tensions in the Middle East continue to simmer; mining of the Strait of Hormuz reportedly began

Optimism drove developed markets’ trading on Tuesday, as investors interpreted Donald Trump's Monday statements as indication that there would be no protracted conflict in the Middle East. Nevertheless, US Secretary of Defence Pete Hegseth said yesterday that the most intense day of attacks yet might follow and that the USA would not back down until "the enemy is totally and decisively defeated." A White House press secretary reiterated that the action could end with the achievement of all US military objectives and the complete capitulation of Iran; but the exact meaning of that remains unclear. As US markets were closing, reports emerged that Iran had begun to lay mines in the Strait of Hormuz, a critical waterway for global trade and an almost unavoidable route for oil trade, but Tehran has not confirmed the news. Reacting in social media Donald Trump first threatened severe retaliation if Iran tried to close the strait and later posted that several mine-laying ships had already been destroyed. According to the CEO of Maersk, the market leader in maritime transport, beyond the insurance of their ships, the safety of their crews must also be guaranteed, to sail through the strait. Saudi Arabia, the United Arab Emirates, Iraq, and Kuwait have already cut back on oil production due to the uncertainty surrounding the strait. The CEO of Saudi oil giant Saudi Aramco said the conflict was by far the biggest crisis the region's oil and gas industry has ever seen and that the oil market is facing catastrophic consequences due to the Middle East war.

Owing to Donald Trump's statements on Monday, the WTI and Brent price slid more than 11%, but they are still more than 20% higher than before the conflict. According to the latest monthly report from the US Energy Information Administration (EIA), the price of Brent could rise above 95 USD/ barrel in the next two months and fall back to around USD 70 by the end of the year.

In Europe, the price of TTF natural gas plunged almost 20% yesterday, paring the increase since 28 February to around 40%.

Tuesday’s trading brought hefty gain to Western Europe’s stock exchanges; CEE region also did well

The benchmark stock markets in Western Europe grew dynamically on Tuesday: Spain’s IBEX, one of the biggest losers of the past week, did best among the indices, which advanced 1.5-3.0%. Italy’s and Germany’s stock exchanges were not far behind; the former two were fuelled by financials, the latter by the industrial sector. The upturn was broad-based at the sector level: of the Stoxx600 sector indices, only food edged lower. The best performers were the basic materials and the banking sectors (the latter was at the centre of last week's selling wave); but the industrial, tourism, and technology sectors could not complain, either. In individual names, Volkswagen surged 2.6% as it expects a recovery in margins after last year's collapse. Britain’s Rotork nosedived 13.4% after publishing its annual figures, to become the Stoxx600's biggest loser.

The CEE region’s stock markets also thrived on hopes for an early end to the Middle East conflict. The top gainer, Hungary’s BUX advanced more than 3%. Among its blue chips, only MTelekom closed in the red, while OTP excelled (+5.55%), in line with the overall good performance of the financial sector.

Wall Street’s key indices, except the NASDAQ, inched down in Tuesday's trading

After initial optimism and several reversals, Wall Street’s leading indices - with the exception of NASDAQ, which climbed slightly higher - closed Tuesday's trading with tiny losses. News on mining of the Strait of Hormuz triggered the last major decline, but the contradictory statements of the US administration cast shadows on trading almost all day. In addition, the uncertain geopolitical situation strengthened inflation fears, as large fluctuations in oil prices, in addition to the already loose labour market, increase the risk of stagflation. Of the S&P’s sector indices, technology achieved gains, while the energy sector slid, along with the slipping in oil prices. Although the prices of some chipmakers rose, software companies dropped again.

The dollar strengthened against the euro; Hungary’s February inflation slowed to 1.4%

Tuesday’s trading was mostly determined by the easing of war fears. European interest rate hike expectations eased slightly, but the market continues to price a 25-basis-point increase this year. Germany’s 10Y yield remained near 2.86%, while the French and Italian bond yields (which are considered riskier) dropped by about 5 and 10 basis points, respectively. On the other hand, the US 10Y yield upped by 5 basis points, to 4.15%. The dollar’s strengthening led the EUR/USD to 1.16.

In Hungary, February inflation came as a big surprise: the headline index fell from 2.1% to 1.4% (versus the expected 1.7%), and core inflation slowed from 2.7% to 2.1% (expected: 2.4%). The CEE region’s currencies moved in all directions: the zloty (PLN) weakened by 0.3%, the koruna (CZK) closed flat, while the forint (HUF) appreciated by 0.2% against the euro, causing the EUR/HUF to climb back to 387. With the easing of the oil market panic, CEE bond yields fell sharply yesterday, from a previous skyrocketing: the Czech 10Y (-20bps), the Polish (-30 bps), and Hungarian benchmark yield (-40 basis points, below 7%) all dropped. The ÁKK sold the announced HUF 30 billion worth of 3M discount Treasury Bills, at 6.16% average yield, amid lacklustre demand.

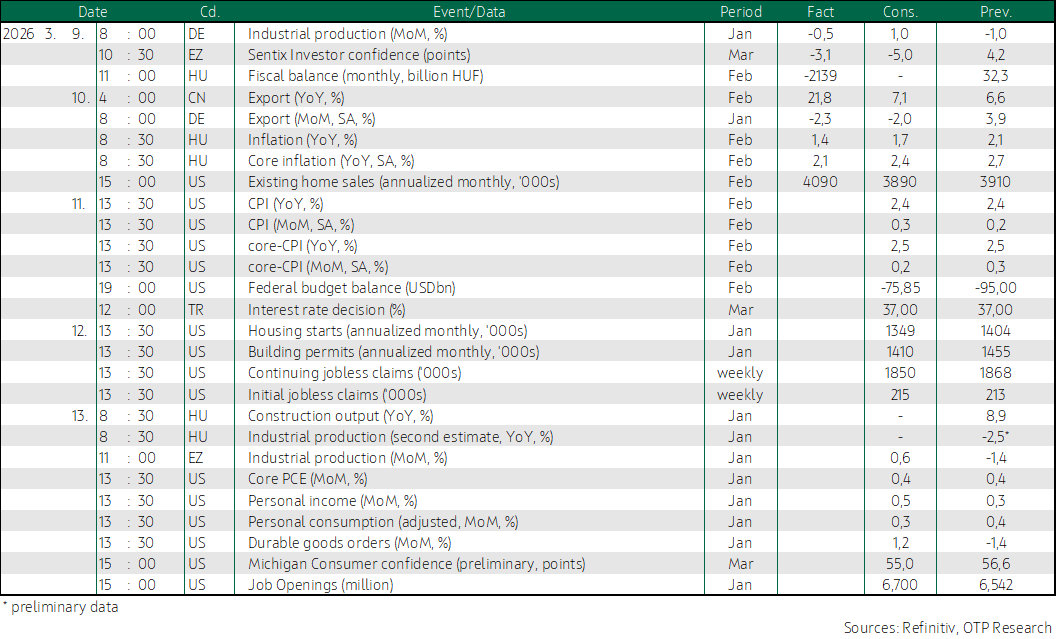

Today’s highlights

Yesterday's decline in oil prices left its mark on the stock markets of the Asia-Pacific region, where most of the leading indices climbed this morning. The share price of electric vehicle manufacturer Nio, listed on the Hong Kong stock exchange, is expected to close around 15% higher, thanks to reassuring fourth-quarter results.

Index futures boded well for today’s trading in the USA, while most of Europe’s leading indices may turn red.

In Hungary, the ÁKK auctions 6M discount Treasury Bills, offering HUF 30 billion debt. In addition, investors can obtain 2034/A and 2037/A bonds worth HUF 10 billion each at the switch auction, in exchange for securities maturing this year.

In addition to the developments in the Middle East conflict, the February inflation data from the USA are worthy of attention today. The Middle East conflict and its impact on oil prices and global supply chains in general, due to the closure of the Strait of Hormuz, will not leave a mark on the February data yet: according to the market's median expectation, headline inflation may have increased by 0.3% and core inflation by 0.2% month-on-month. At the same time, the harsh weather in February and the already slightly rising oil and service prices may cause negative surprises. The market’s expectations continue to point to a 25-basis-point interest rate cut by the end of this year.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more