OTP Morning Brief: December’s US retail sales were weaker than hoped

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

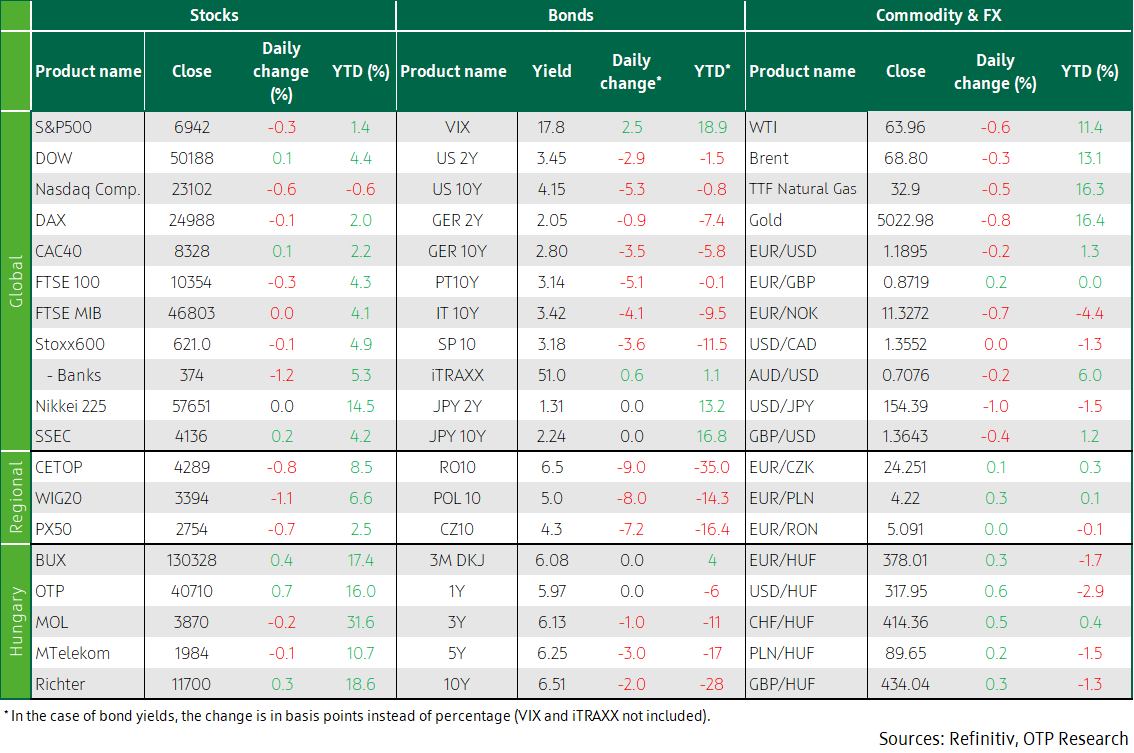

Most stock markets in Europe declined yesterday. Earnings from Philips and Kering beat expectations; BP’s shares fell. America’s major indices closed mixed. Disappointing retail sales data put retail stocks under pressure. The financial sector’s shares also fell. US business inventories grew less than expected. Developed markets’ and Hungary’s yields declined. The USD strengthened slightly, while theHUF weakened somewhat, paring previous gains. Employment and federal budget data will be published in the USA today.

Most of Europe’s stock markets declined on Tuesday; Philips’s and Kering’s reports beat expectations; BP’s shares fell

In Europe, many stock markets ended in the red on Tuesday. Several major European companies released their results. The 2025 annual report of Philips revealed that it had achieved a 6% increase in order intake, returned to profitability after a loss-making 2024, and forecast sales growth of 3-4.5% for 2026. The stock price jumped nearly 12%. In contrast, BP lost 6.1% after announcing that it will suspend share buybacks to strengthen its balance sheet, and its 2025 net profit of USD 7.49 billion missed expectations. Shares in France's Kering jumped by 10.9% as the revenue of Gucci’s owner beat analysts' forecasts and the company expects growth to return by 2026. The positive sentiment buoyed the entire luxury segment. Investors continue to keep an eye on political developments in Britain, where Prime Minister Keir Starmer's position has been weakened by fresh criticism and scandals surrounding the appointment of Peter Mandelson to Washington.

The CEE region's indices closed mixed: the BUX rose, but the Prague and Warsaw indices slipped. In Budapest, OTP and Richter rose, while the other two blue chips subsided.

US indexes closed mixed; pale retail sales data put retail stocks under pressure; the financial sector’s stocks also fell; US business inventories rose less than expected

US indexes closed mixed on Wednesday as investors grew cautious on weaker-than-expected retail sales data and the potential impact of artificial intelligence on the financial sector. The retail sector came under pressure: shares in Costco and Walmart slid nearly 2%. In the USA, retail sales were flat in December, well below market expectations for a 0.4% increase and in a clear slowdown from a 0.6% increase in November. The ex-auto and fuel sales figure also stagnated, while the control group retail sales, used to calculate GDP, shrank 0.1% MoM, in the first decline in three months. Investors focused on key macro data due later this week: non-farm payrolls on Wednesday and the consumer price index on Friday. The financial sector also saw selling pressure after technology platform Altruist unveiled a new tax planning tool based on artificial intelligence: LPL Financial shares (-8.3%), Charles Schwab (-7.4%), and Morgan Stanley (-2.4%) all suffered painful losses. At the same time, there was a rotation into sectors that are less sensitive to cycles, such as basic materials and utilities.

Meanwhile, US business inventories upped just 0.1% in November 2025, missing the market consensus of 0.2%. Inventories rose at wholesalers (0.2%) and manufacturers (0.1%), while retail inventories dipped 0.1%. Inventories rose by 1.2% year-on-year.

Developed markets’ and Hungary’s yields declined; the dollar strengthened slightly; the forint weakened somewhat, reversing a previous appreciation

In Japan, bond trading started with a decline in yields, as fears of excessive fiscal spending eased after the two-thirds victory of the Liberal Democratic Party led by Takaichi Sanae. Japan’s 10Y yield sank by six basis points, to less than 2.25%. Later, the weaker-than-expected US retail sales data and the slowing rise in wage costs (quarterly growth of 0.7% after the previous 0.8%) contributed to the decline in yields on both sides of the Atlantic. The ten-year dollar yield sank by more than 5 basis points, to 4.15%. In the eurozone, there was a smaller yield decrease of 3-4 basis points; the 10Y German yield sank to 2.8%. Ending Monday’s dollar weakening, the EUR/USD sank below the 1.19 mark yesterday.

Reversing a previous rapid strengthening, the forint lost 0.4% on Tuesday, sending the EUR/USD above the 378 level. The zloty (PLN) and the koruna (CZK) also weakened, but to a lesser extent. Bond yields sank again, by 1-3 basis points, thus the 10Y yield dropped to the bottom of its 12-month trading range, to 6.5%. There was adequate demand at the auction of three-month discount Treasury Bills, and the ÁKK did not hesitate to sell HUF 50 billion worth of T-bills (vs the planned 30bn), at an average yield of 6.1%.

Today’s highlights

Asia’s stock markets were on the rise today. In China, January inflation came in at a lower-than-expected 0.2%, confirming the deflationary situation in the absence of major stimulus. Japan’s markets were closed for a national holiday.

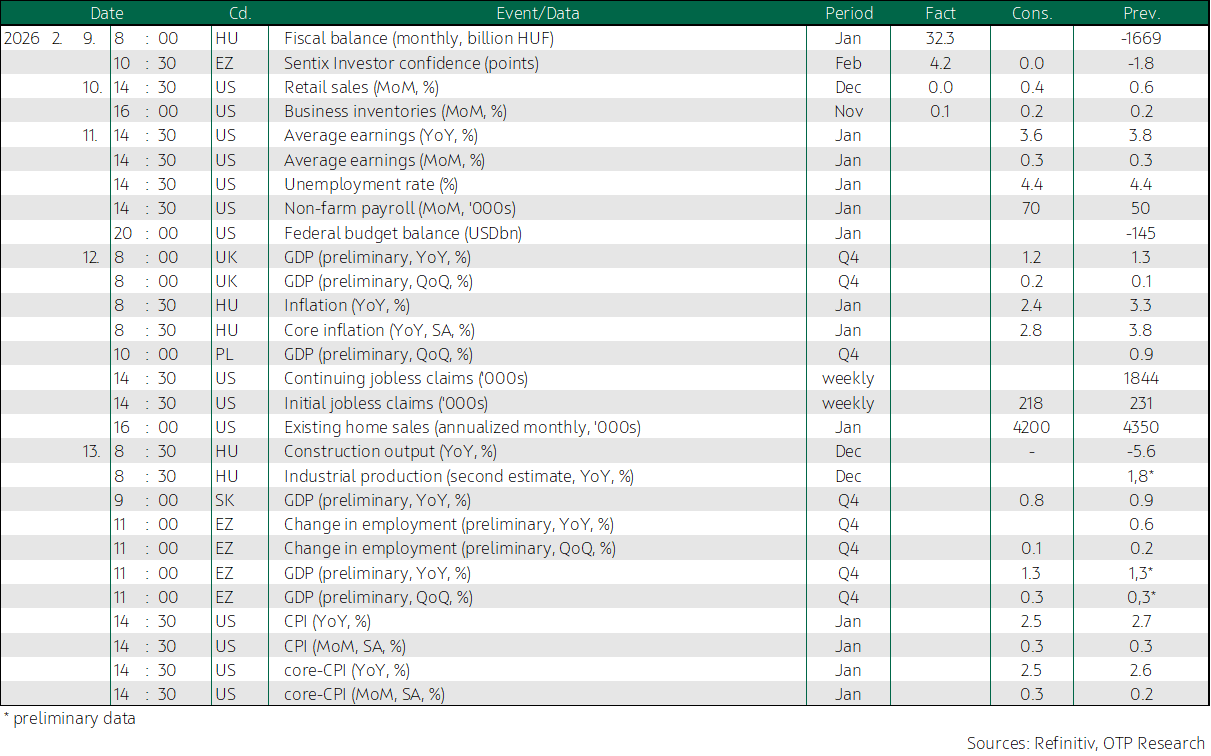

Today, the USA releases average earnings and unemployment data, non-farm payrolls for January, as well as the US federal budget balance for January.

In Hungary, the ÁKK auctions six-month discount Treasury Bills, offering HUF 30 billion. At the switch auction, investors can obtain 2033/A and 2037/A bonds worth HUF 15 billion in each, in exchange for securities maturing this year.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more