OTP Morning Brief: Markets were on roller-coaster on Monday, and the volatility may persist today

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

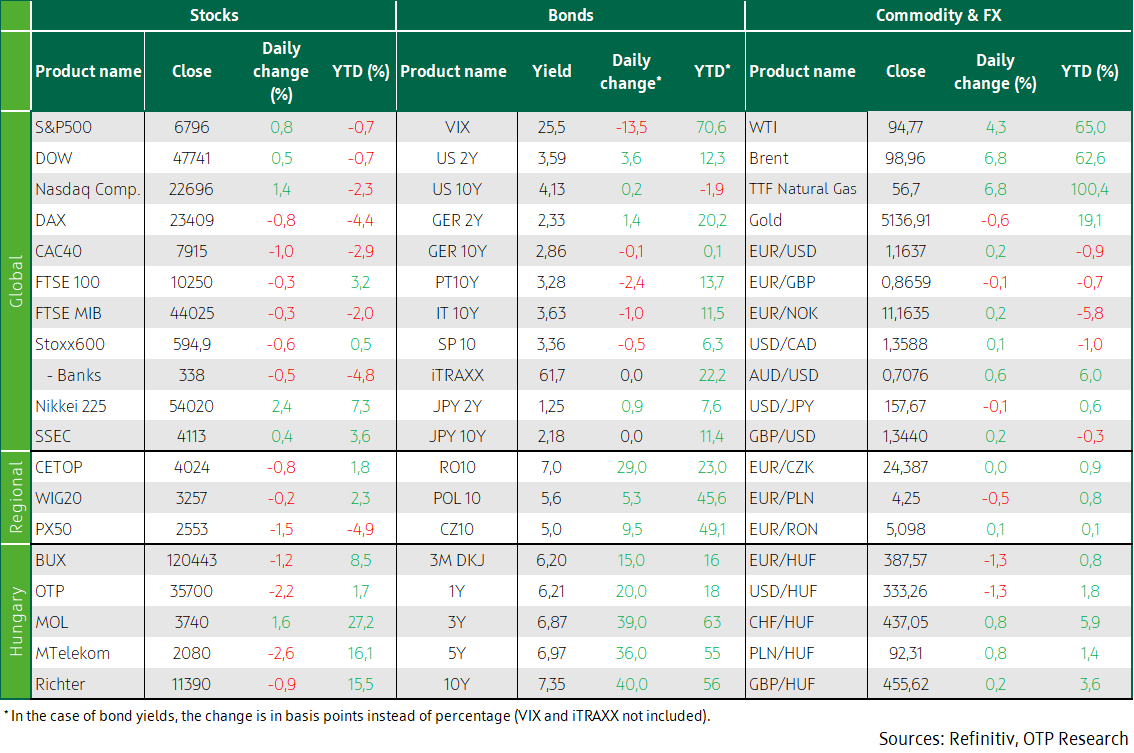

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Western Europe’s stock markets fell amid elevated inflation risks due to a further jump in energy prices and heightened expectations of interest rate hikes. Hungary’s BUX also ended in the red. Brent hit USD 120 at one point on Monday, before falling well below USD 100 by the evening as Donald Trump signalled that the war may soon end. US markets rebounded by the close. Hungary is to cap fuel prices and reduce the excise tax rate. Global yields closed mixed, ending the roller-coaster ride. In Hungary, there was a spike when benchmark yields were fixed, but later subsided somewhat. The dollar weakened trivially, and the forint strengthened against the euro following Donald Trump's announcement; the EUR/HUF closed below 388. Today, Hungary publishes inflation data. The roller coaster may continue as the IRGC rejected Donald Trump's announcement this morning.

Western Europe’s markets fell as soaring energy prices fuelled inflation risks and interest rate hike expectations; the BUX also ended the day in the red

Europe’s stock markets continued their decline yesterday and fell to more-than-two-month lows on Monday. A sharp rise in oil prices (briefly to USD 120) augmented inflation concerns. The STOXX Europe 600 fell (-0.6%) for the third day in a row, after posting its worst weekly performance in almost a year on Friday. The index is almost 6% below its record closing level on February. The STOXX volatility index rose to its highest since April 2025, before retreating by the end of the day. Iran has appointed Mojtaba Khamenei as its supreme leader, to succeed his father Ali Khamenei, in a move widely seen as a consolidation of Tehran’s hardliners’ power, further reducing the chances of a quick resolution to the war.

The STOXX 600’s energy sector (+1.4%) was the only one to rise yesterday. The real estate sector (-2.7%) took the biggest hit as concerns about a renewed surge in inflation pushed the market scale down rate cut expectations in the USA, and it began pricing in a rate hike in the eurozone. Meanwhile, the G7 countries have yet to decide whether to release emergency oil reserves as the war in Iran sent prices above 119 USD/barrel, the French finance minister said. Banking shares, which were at the heart of last week’s sell-off, continued to lose (-0.5%). Travel & leisure stocks (-2%) came under renewed pressure.

In the corporate word, Kinnevik nose-dived 17%, to become the STOXX 600’s worst performer, after Ningi Research said it had taken a short position in the company. Roche slumped 2.6% as the drugmaker’s oral breast cancer drug had failed in a trial.

In the gloomy market sentiment, Hungary’s BUX underperformed, losing 1.2%, but the Budapest market closed earlier than its Western European peers did, so it could not benefit from the Brent’s late-day reversal. The CEE region’s markets slipped 0.2%–1.5%. In Budapest, MOL (-1.6%) was the only blue chips to see gain, while the other three ended Monday’s session in the red, sliding 0.9%–2.6%.

Hungary’s government announced fuel price caps of HUF 595 (95 type gasoline) and HUF 615 (diesel). Moreover, Minister Márton Nagy said the excise tax on fuels will be reduced by nearly HUF 20.

US markets picked up as Donald Trump said that the war might end very soon; having reached record highs last seen in mid-2022, oil prices sank below USD 100 by the end of the day

On Monday, everything was driven by developments related to the war in Iran. Wall Street stocks recovered from the steep sell-off and finally closed higher, during a reversal in the last hour: US President Donald Trump suggested that the war against Iran could be nearing its end. All three indexes rebounded late after Trump said the war was going much better than expected.

In early trading, oil prices rose to levels last seen in mid-2022 as delivery disruptions squeezed supplies as the war with Iran entered its 10th day. Brent and WTI traded near USD 120. The soaring energy prices could easily translate into broader inflationary pressures at a time when many U.S. consumers are already struggling to cope with the cost of living.

The Dow Jones Industrial Average (+0.5%), the S&P500 (+0.8%), and the Nasdaq Composite (+1.4%) all grew. Nine of the 11 major S&P 500 sectors closed higher, with technology stocks leading the gains. Financials and energy ended lower. The Philadelphia Semiconductor Index rebounded, with chipmakers SanDisk, Broadcom, and Nvidia surging 2.7%–11.7%. Construction companies, banks, and aerospace/defence stocks were clear underperformers.

After a roller-coaster ride, advanced economies’ yields closed mixed, but in Hungary there was another jump when benchmark yields were fixed, but it abated later. The USD weakened trivially, the HUF strengthened against the EUR and closed below 388

The war in Iran was the most important market driving force in the FX and bond markets too. In the morning, fears of inflation and interest rate hikes intensified due to the nearly 30% skyrocketing in oil prices; the EUR/USD sank to around 1.15, and the American and German ten-year yields grew by 5-6 basis points, and the French and Italian ones by another 10-12 basis points. Tensions eased in the afternoon and developed markets’ bond yields returned to Friday's closing levels. But the real surprise came when Donald Trump announced that the US had practically achieved its goals in Iran and that the war might soon be over. Then, alongside the sharp fall in oil prices, yields continued to descend: the 10Y dollar yield sank below 4.10%, the German one below 2.85%, both closing the day lower. The EUR/USD returned to 1.163.

Monday’s trading started with heavy selling pressure on the CEE region’s currency and bond markets. The Czech koruna (CZK) and the zloty (PLN) started the day with 0.5-1% weakening, and the forint lost nearly 2%; the EUR/HUF jumped to almost 400. The Czech and Polish currencies retained 0.2%, and the forint strengthened back to 395. After Donald Trump's words, the Hungarian currency rebounded in the evening, pushing the EUR/HUF below 388. In Hungary’s fixed income market, interest rate cut expectations were temporarily replaced by interest rate hike expectations. In the morning, the forint pricing implied that the base rate, which was reduced to 6.25% last week, could rise to 7% this year, of which 6.5% remained by the evening (+25 basis points). Hungary’s bond yields – hand in hand with the Czech and Polish markets – jumped by 30-40 basis points at one point. Hungary’s 10Y yield increased to around 7.35% (the highest since October 2023), before declining to 7.2% in the afternoon.

Today’s highlights

Asia’s stock markets rebounded this morning. WTI and Brent futures fell below USD 90, as global market sentiment was extremely volatile on Monday evening, following US President Donald Trump's announcement. Japan’s Nikkei soared 2.4%, China’s SSEC upped 0.4%, and the MSCI Asia-Pacific stock index (excluding Japan) surged 2.6%, reducing the losses accumulated since the start of the conflict. Europe’s index futures inched up a few decimal points after yesterday's slump, but US futures are slightly down after yesterday's rise. Today’s trading may be also shoppy, as Donald Trump's statements are in sharp contrast to the events in Iran - this morning the Revolutionary Guard (IRGC) declared that they “will determine the end of the war" and dismissed Donald Trump's statement as "nonsense".

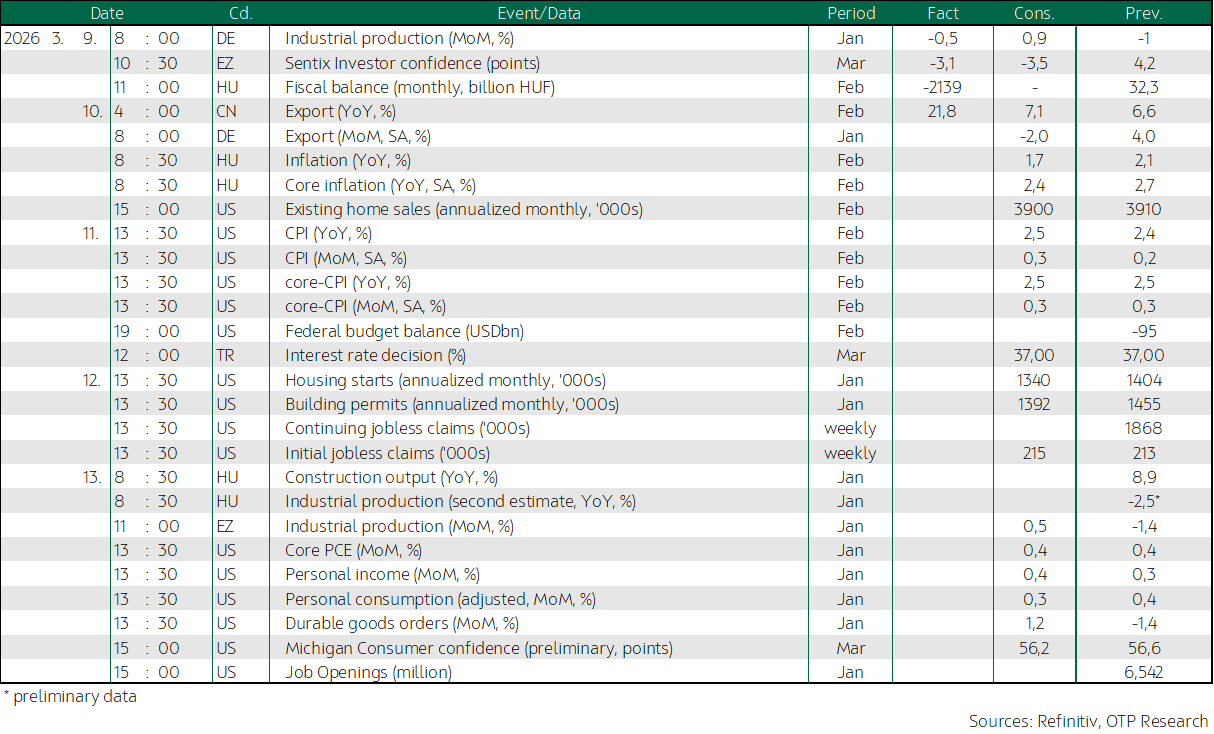

Today, Hungary publishes inflation data for February, our forecast is 1.8%. Today’s gauge is likely to be the lowest reading in 2026 – we expect a moderate acceleration from now on, and the process is likely to be further bolstered by the effects of the war in Iran. The developments in the Gulf region will primarily and most quickly affect Hungarian inflation through oil and fuel prices, although the fuel price cap announced yesterday will mitigate the impact. Although the rise in gas prices does not directly increase inflation due to regulated tariffs for household, it will also gradually trickle down to inflation indirectly, through the increase in companies’ energy costs.

Of today’s data releases elsewhere, Germany’s export statistics may be the most interesting one.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more