OTP Morning Brief: The rebound continued on Monday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

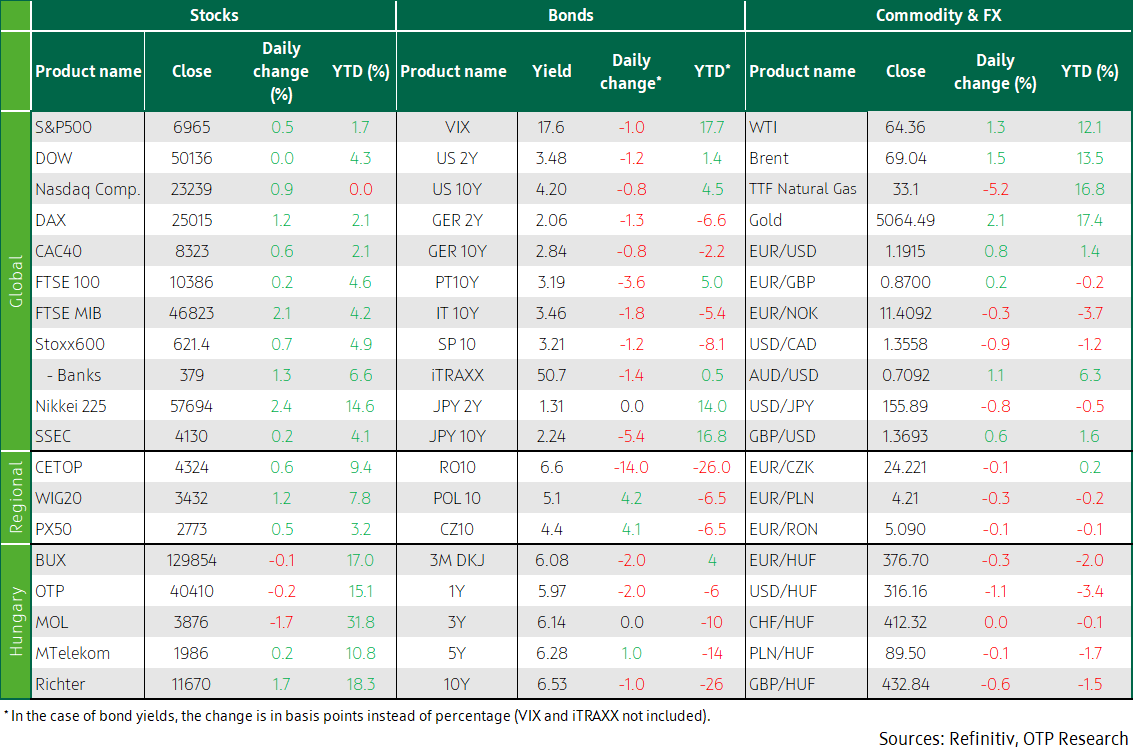

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Friday's rebound continued on the developed stock markets on Monday, the pressure on the tech sector has eased. The Stoxx600 closed at new high on Monday, as the strengthening banking sector and mining companies gave impetus. The BUX edged lower yesterday. The recovery continued in the USA as well, the Dow went to new high. Developed markets’ bond yields barely moved yesterday. The forint traded at its strongest in two years against the euro. Today, US retail sales and business inventory statistics will be in focus. The earnings season continues with reports from Coca-Cola, AstraZeneca, UniCredit, BP, and Kering.

Western Europe’s stock markets rallied as the pressure on the tech sector eased; mining and defence companies lifted indices

Ending last week's sell-off, Europe’s major stock indexes closed at new highs on Monday as concerns about the tech sector subsided. The Stoxx600 rose by 0.7%, propelled by STMicroelectronics’ nearly 10% jump after the French company announced it would expand its partnership with Amazon Web Services (AWS). Europe’s banking sector also posted strong gains, particularly UniCredit: the Italian bank shot up almost 7% after raising its profit forecast and holding on to stakes in its rivals. The Stoxx600 banking index rose by 1.3%, while the bank-heavy FTSE-MIB gained 2%. Novo Nordisk, which has been hit hard by fierce competition in the weight-loss drug market in the past week, bounced back 5% after Hims and Hers Health said it would stop selling an unapproved, cheap copycat of the original weight-loss drug after the US Food and Drug Administration (FDA) threatened to fine the US drugmaker.

The DAX grew by 1.2%, to a three-week high, driven by banks and industrials, particularly defence companies such as Rheinmetall. Commerzbank (+3.7%) was the top performer, boosted by strong results and profit forecasts from Italian banking giant UniCredit, which has a 26% stake in the German bank. SAP (+2.2), and Dutch fintech platform Adyen (+4.6%) rebounded from last week’s sector-wide sell-off, triggered by the performance of Anthropic’s automation tools. TotalEnergies, Siemens, EssilorLuxottica, and Siemens Energy all closed higher ahead of their earnings reports this week. In the UK, the FTSE100 ended slightly above Friday’s close on Monday, as mining shares helped pare the morning’s losses. Antofagasta soared 6.6%, tracking a rise in copper prices, followed by precious metals operators Fresnillo (+5.9%), and Endeavour Mining (+5.5%). Diversified miners such as Glencore, Rio Tinto and Anglo American also posted strong gains of between 3% and 5%. The UK’s defence manufacturers fared well, too: Rolls-Royce revved up nearly 4%, BAE Systems and Babcock advanced roughly 3% each.

M&A news also drove Europe’s stock markets on Monday. A consortium led by Advent and FedEx agreed to buy InPost for USD 9.2 billion, sending the Polish courier company's share price 13.5% higher. NatWest lost 5.6% after agreeing to buy asset management firm Evelyn Partners for GBP 2.7 billion.

The TTF natural gas price fell 6%, to less than 34 EUR/MWh on Monday, as the cold wave affecting northern and eastern European countries in the second half of February may be milder than previously thought, reversing earlier increases in gas transmission prices.

In the CEE region, Hungary’s BUX (-0.1%) underperformed on Monday, as its peers PX (+0.5%) and WIG20 (+1.2%) closed higher. Of Budapest’s blue chips, MOL fell 1.7%, Richter gained that much, and OTP shed 0.2% but MTelekom rose comparably.

The rebound continued in America, technology led the rise

After an uncertain beginning, US stock indices continued to climb higher on Monday. The Dow’s tiny uptick was enough to reach a new high, the S&P500 gained 0.5%, and the Nasdaq Composite grew by 0.9%. Following last week’s sell-off on AI concerns, Friday’s bounce back continued yesterday, with technology leading the S&P500 sector gains, followed by the materials sector. The biggest losers were consumer discretionary and healthcare. The S&P500 Software Services index surged nearly 3%, ending a multi-day decline last week on concerns about the competitive nature of artificial intelligence. Among software developers, Oracle was the biggest gainer of the day, jumping nearly 10% after D.A. Davidson upgraded its Neutral rating to Buy. The Philadelphia’s SE Semiconductor index rose 1.4%; of its stocks, Nvidia (+2.5%) posted the biggest gain, which was also the largest in the S&P 500 on Monday, but market participants will have to wait until the end of the month to see the latest figures from the AI chip leader.

In individual stocks, Hims & Hers Health fell 16%, recording its seventh consecutive daily loss. Novo Nordisk sued the telehealth company for patent infringement after the U.S. company launched a USD 49 copycat of the Danish drugmaker’s diet pill Wegovy, and then withdrew it on the back of negative reviews from FDA. Workday shares fell 5% after the human resources software provider said its co-founder Aneel Bhusri would return as CEO. Kyndryl shares plunged 55% after the IT service provider delayed its quarterly report, warning of ‘material weaknesses’ in its financial statements. The stock price of Kroger jumped by 4% after the grocery giant named former Walmart executive Greg Foran as CEO.

Crude oil prices nudged higher on Monday, as tensions between the United States and Iran failed to ease significantly, despite progress in recent talks. On Monday, the USA issued a warning to all US-flagged ships to avoid Iranian waters when passing through the Strait of Hormuz. The warning came as talks between the two countries appeared to be continuing, as Friday’s talks in Oman were described as positive. However, uncertainty remains over a deal, as Iran insists on uranium enrichment, the stopping of which is a key issue for the USA.

The rebound in the price of gold and silver continued on Monday: gold added 2% and silver marched 7% higher, even though risk aversion has slightly eased. However, China's purchases of precious metals continue to heat the market, further strengthening volatility, market experts opine.

Long-term yields barely moved in developed economies’ bond markets and in Hungary; the USD wobbled, the forint went to its strongest in two years against the euro

Although Japan’s Liberal Democratic Party achieved a historic two-thirds victory, after which Japan’s bond yields rose markedly (the 10Y yield increased by six basis points, to 2.3%), yields in other markets did not budge. The 10Y dollar yield remained at 4.2% after a trivial dip, and the 10Y German Bund yield traded around 2.85%. The dollar lost almost 1% ground from the euro, trading at 1.19.

The forint’s appreciation sent the EUR/HUF to a two-year low of less than 377. Bond yields have barely changed after the substantial fall in previous weeks and the correction at the end of last week. The ten-year yield is still hovering at the bottom of its trading range of the past year, around 6.5%. The ÁKK’s switch auction of discount Treasury Bills failed yesterday, due to lack of interest.

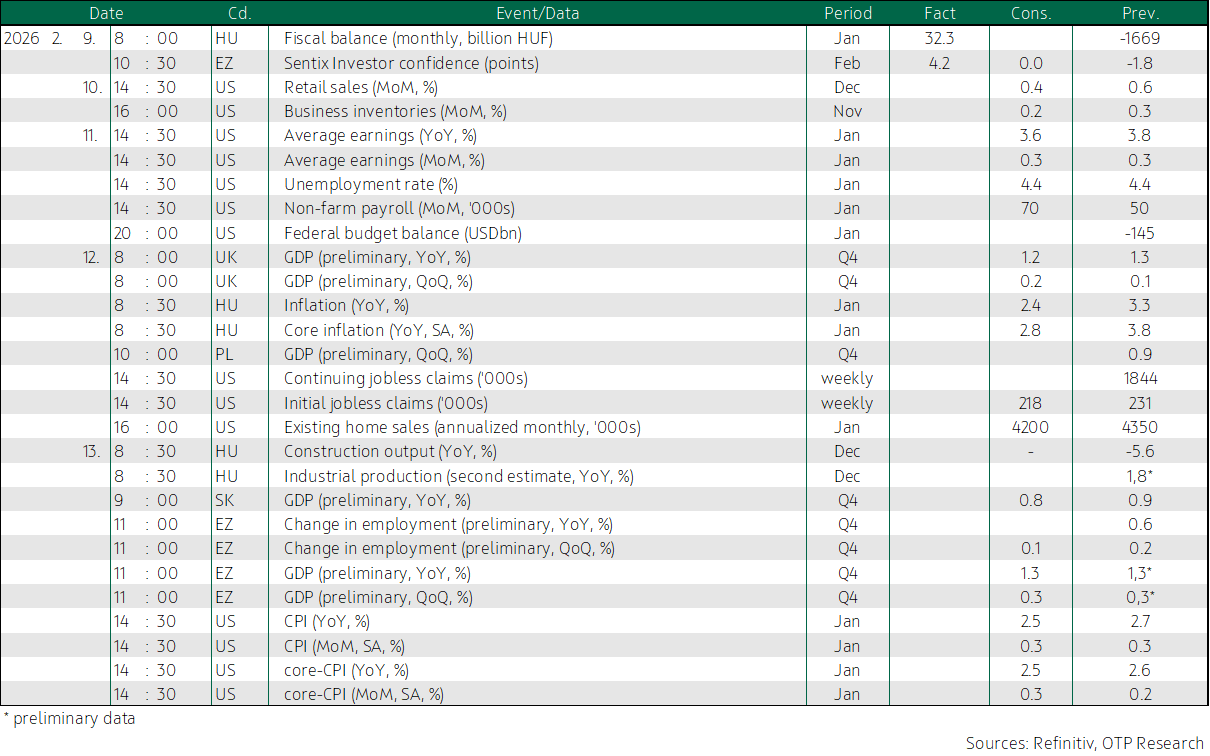

Today’s highlights

The sentiment in Japan’s stock markets remained benign, following the weekend elections and Monday's 4% rally. Heading into today’s close, the Nikkei was seen gaining more than 2%. Elsewhere in Asia, stock markets painted a mixed picture: China’s Shanghai Composite and Hong Kong’s Hang Seng nudged higher, but Korea’s benchmarks were mostly in the red.

Futures pointed to mixed opening on both sides of the Atlantic. Today, the quarterly earnings figures of Coca-Cola, AstraZeneca, UniCredit, BP, Kering, Barclay’s, Spotify, Ferrari and Ford Motor will see the light of day.

On the macro front, US retail sales statistics and business inventory data could make an interesting reading.

In Hungary, the ÁKK auctions three-month discount Treasury Bills, offering HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more