OTP Morning Brief: Stock markets fell widely after first week of war

Related content

OTP Morning Brief: Rebound in chip stocks led equity markets higher

Despite the deteriorating geopolitical environment and rising oil prices, equity markets in developed economies closed higher on Tuesday as optimism regarding the outlook for semiconductor manufacturers regained momentum. In bond markets, however, long-term yields edged higher, with both the US and German benchmark yields approaching the peaks reached in May. EUR/USD closed just below 1.14. In Hungary, the focus yesterday was on the MNB’s rate-setting meeting, where, in line with expectations, policymakers decided on a 25bp rate cut. At the post-meeting press conference, Governor Mihály Varga reiterated the forward guidance communicated earlier, signaling further easing over the summer. Yields with maturities of more than one year fell in the Hungarian bond market; the forint weakened following the interest rate decision, and the EUR/HUF exchange rate closed at 362. The Hungarian equity market advanced, with the BUX reaching a new intraday record high, driven by strong momentum in OTP shares. The focus of today’s trading session in international markets will be on corporate earnings releases, including results from Alphabet, Tesla, and Texas Instruments.

OTP Morning Brief: Markets remain on hold ahead of the MNB rate decision and Middle East tensions

European equities closed mixed on Monday, as investors remained cautious ahead of this week's ECB rate decision, while ongoing Middle East tensions encouraged a wait-and-see approach. US indices declined, while semiconductor stocks outperformed, supported by AI-related optimism and reports about Alphabet’s chip development efforts. Oil prices experienced significant volatility: Brent crude surged above $90 per barrel before partially retracing on reports of a possible US-Iran diplomatic rapprochement. In the Hungarian market, the BUX rose, while OTP announced the acquisition of Luminor Bank. Today's trading session is likely to focus on the MNB's rate decision and the ongoing earnings season.

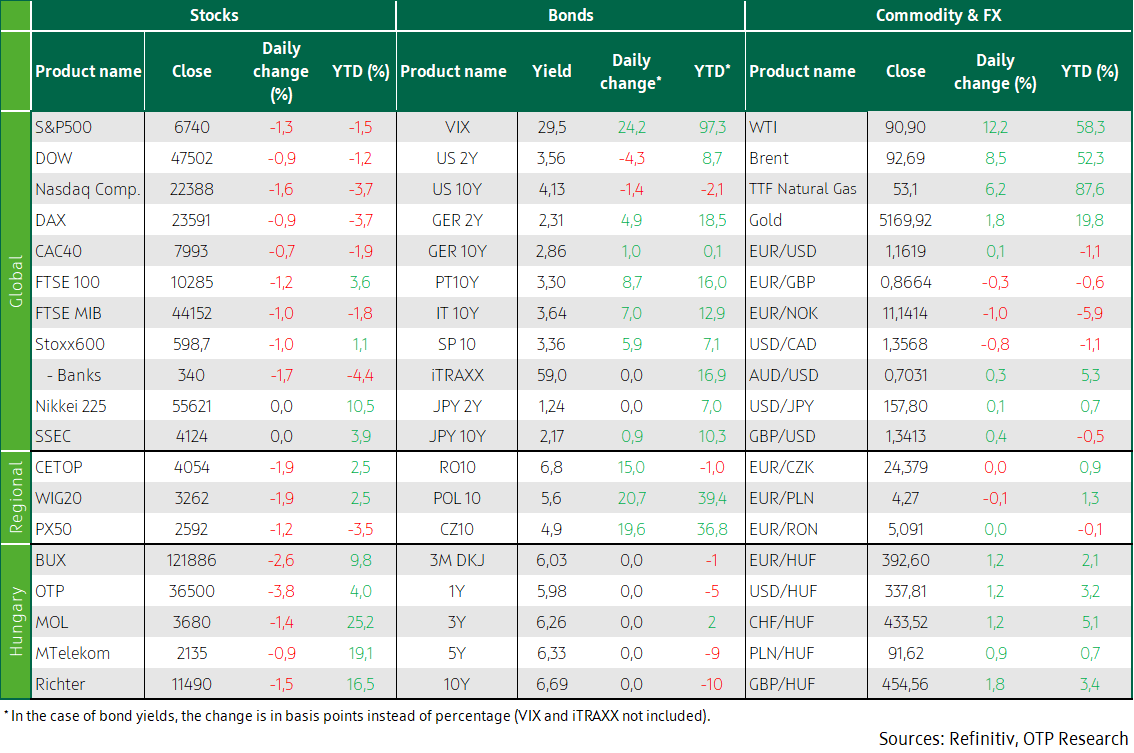

The war continued over the weekend, and Iran elected a new supreme leader. Europe’s indices closed one of their worst weeks in a long time, with shares falling in all segments except the energy sector. Germany’s industrial orders and Hungary’s industrial production rose. Stocks fell sharply on Wall Street, oil prices continued to rise. Bond yields rose due to geopolitical tensions, and the forint’s weakening led the EUR/HUF above 392. Asia’s stock markets fell today. A string of inflation data will be worth watching this week.

The war continued over the weekend, Iran elected new supreme leader

During the weekend, Iranian sources indicated that the succession process was in advanced stage. In a video message, religious leader Hosseinali Eshkevari suggested that Ayatollah Khamenei's son, Mojtaba, may be elected as successor – and this was officially confirmed this morning. Analysts opine that the election of Mojtaba - a deeply hardline cleric, whose wife, mother, and several family members were killed in US-Israeli air strikes - sends a clear message: for the survival of the regime, the Iranian leadership rejects any compromise, and sees no other way than confrontation, retaliation, and survival. However, Donald Trump says Washington should have a say in the succession. Meanwhile, Israel continued its targeted strikes against Iranian leaders, and Tehran was covered in black smoke after attacks on oil facilities. The conflict spread to several Arab countries during the week: Saudi Arabia, Kuwait, the United Arab Emirates and Bahrain reported Iranian drone and missile attacks, which caused deaths and infrastructure damage. In Lebanon, the Israeli army attacked Beirut, targeting Hezbollah leaders, while the Iranian-linked terrorist organization joined the conflict with strikes against Israel.

Europe’s stock markets had a harsh week; German industrial orders and Hungary’s industrial production rose

Having declined 1% on Friday, the STOXX 600 index posted its worst weekly loss (-5.5%) in nearly a year on Friday, on the back of the growing uncertainty in the Middle East and a nasty surprise in US employment data, which casts a shadow over the Fed's interest rate path. On Friday, Germany’s DAX (-0.9%), France’s CAC40 (-0.7%), and the UK’s FTSE 100 (-1.2%) all slid. The French index recorded the biggest weekly drop (-6.8%). Among the sectors, only energy rose (+0.8%), on the back of rapidly rising energy prices. The biggest drop was seen in the media sub-sector (-2.3%), but banks (-1.7%) also came under pressure again, sinking to almost a three-month low. HSBC (-2.6%) and Allianz (-1.6%) shares slumped, too. Healthcare companies slipped 1.6%, as Zealand Pharma shares nose-dived 36% and those of Roche slumped 2.9% as mid-stage trial results for its experimental obesity treatment fell short of investors’ expectations. Beyond the energy sector, defence companies had a good day, benefiting from a growing demand for weapons; Rheinmetall advanced 2.9% and Leonardo soared 3.4%.

In terms of macroeconomic data, Germany’s factory orders expanded by 7.8% month-on-month in December 2025, exceeding market expectations for a 2.2% decline by a large margin and accelerating from a slightly upwardly revised 5.7% increase in November. This was the fourth consecutive monthly increase and the strongest one since December 2023, driven mainly by large orders in the metal products (30.2%) and machinery (11.5%) sectors.

Risk aversion hit the CEE region particularly hard: Czechia’s PX 50 (-1.2%), Poland’s WIG20 (-1.9%), and Hungary’s BUX (-2.6%) all slid. In Budapest, OTP fell the most (-3.8%), but other blue chips also showed significant declines. Over the past week, the BUX dived 3.7%, and OTP lost 7.1%, while MOL grew by 4.3%.

In January, Hungary’s industrial production expanded by 1.5% month-on-month, posting increase for the second consecutive month, slightly reversing the negative trend that has been going on for years, while it still shows a 2.5% year-on-year contraction.

Wall Street’s stocks fell sharply, oil prices rose further

Wall Street's three major indexes closed lower on Friday after a sharp deterioration in the US labour market and a sharp jump in US oil prices due to the escalation of the Middle East conflict. The Dow (-0.9%), the S&P500 (-1.3%), and the NASDAQ (-1.6%) closed in the red on Friday, which hurt their weekly performance: the Dow (-3%), the S&P (-2%) and the NASDAQ (-1.2%) all closed lower over the past week. The banking sector lost 2.0%, driven by BlackRock’s 7.1% slump as the asset manager had restricted cash withdrawals. Shares in Western Alliance dived 8.4% after suing Jefferies for failing to make a loan payment related to bankrupt auto parts supplier First Brands Group. Jefferies shares plunged 13.5%. Travel & leisure stocks also retreated, owing to rising fuel costs: the S&P Passenger Airlines sub-index, which tracks passenger airlines, descended 4.1%. On the other hand, the S&P’s energy stocks inched up 0.1%, as higher energy prices could boost their earnings.

The outlook was further dampened by labour market data released on Friday, which showed that the U.S. economy lost jobs in February, and the unemployment rate increased to 4.4%, pointing to a worsening labour market, and making it harder for the Fed to cut interest rates amid rising oil prices due to the Middle East war. Nonfarm payrolls fell by 92,000, partly due to healthcare workers’ strike and disruptions caused by a winter storm. The weak data may have been affected by a sudden surge in January growth, partly owing to a statistical bias. The trends indicate that employment has slowed significantly, undermining the Fed’s narrative that the labour market is stabilizing. The market currently expects the Federal Reserve to keep interest rates steady in March, and the chance of a rate cut in June has increased. US retail sales shrank by 0.2% month-on-month in January 2026, following a flat month in December, and slightly exceeding market expectations for a 0.3% decline.

Brent crude oil prices headed higher, towards 108 USD/barrel last night, up 16.5% from the previous day and up 41.95% in the past month. Precious metals rose in sync with the rising uncertainty: gold added 1.8% and silver soared 2.6% on Friday.

Bond yields rose on geopolitical tensions; the forint’s weakening sent the EUR/HUF above 392

The offensive by the United States and Israel against Iran, and Iran's retaliatory strikes – the closure of the Strait of Hormuz and attacks on the region’s energy infrastructure – brought about a significant shock in the commodity and stock markets, as well as in the bond and currency markets last weekend. Oil prices skyrocketed 10% on Friday and grew by 50% in a week. European gas prices shot up 4% on Friday, and jumped by 70% in a week, thus inflation fears ran high once again. Neither did it help that inflation and all major sub-indices in the eurozone came in higher than expected. Although the number of US jobs fell in February, wage dynamics accelerated again. US interest rate cut expectations have weakened: now the most likely scenario is that there will be only one rate cut this year. In the eurozone, previous expectations of holding (or possibly reducing) interest rates were replaced by the anticipation of an interest rate hike: the market is pricing in the possibility of the ECB raising rates once (or even twice) in 2026. Although US long-term yields barely moved on Friday, they have risen materially last week: the ten-year yield rose by 20 basis points from last week's below-4% levels, reaching 4.15%. Germany’s ten-year yield rose comparably, to 2.85%. France’s and Italy’s long-term yields jumped even stronger, by 30-35 basis points. In this environment, it is no wonder that the dollar appreciated substantially: the EUR/USD decreased by almost 3%. Having started last week at 1.18-1.185, the cross ended around 1.16 on Friday.

The CEE region’s currencies also weakened against the euro. The Czech koruna (CZK) weakened by almost 1% in a week, the zloty (PLN) lost nearly 1.5%, while the forint depreciated by 4% in a week, driving the EUR/HUF from 376 to nearly 393. The sentiment on the CEE region’s government bond markets was likewise gloomy: the 10Y bond yields of Czechia, Poland, and Hungary rose by 50-60 basis points (half of that on Friday); the Hungarian one bounced back to around 7%. Previous interest rate cut expectations have weakened significantly: a week ago, prices implied around 5.5% base rate by the end of the year – but on Friday the yield curve was consistent with only one further cut and a 6% year-end rate.

Today’s highlights

This morning, Asia’s indices slipped broadly, owing to the war. The Hong Kong index hit a six-month low on today, while China’s markets erased their year-to-date gains as the escalation of the Middle East war sent oil prices soaring, and sharply dampened appetite to buy Asian stocks. The Hang Seng decreased by 1.8%, the SSEC lost half a percent, while Japan's Nikkei plunged 4.9%. South Korea's Kospi index, which had outperformed so far this year, slumped 6%.

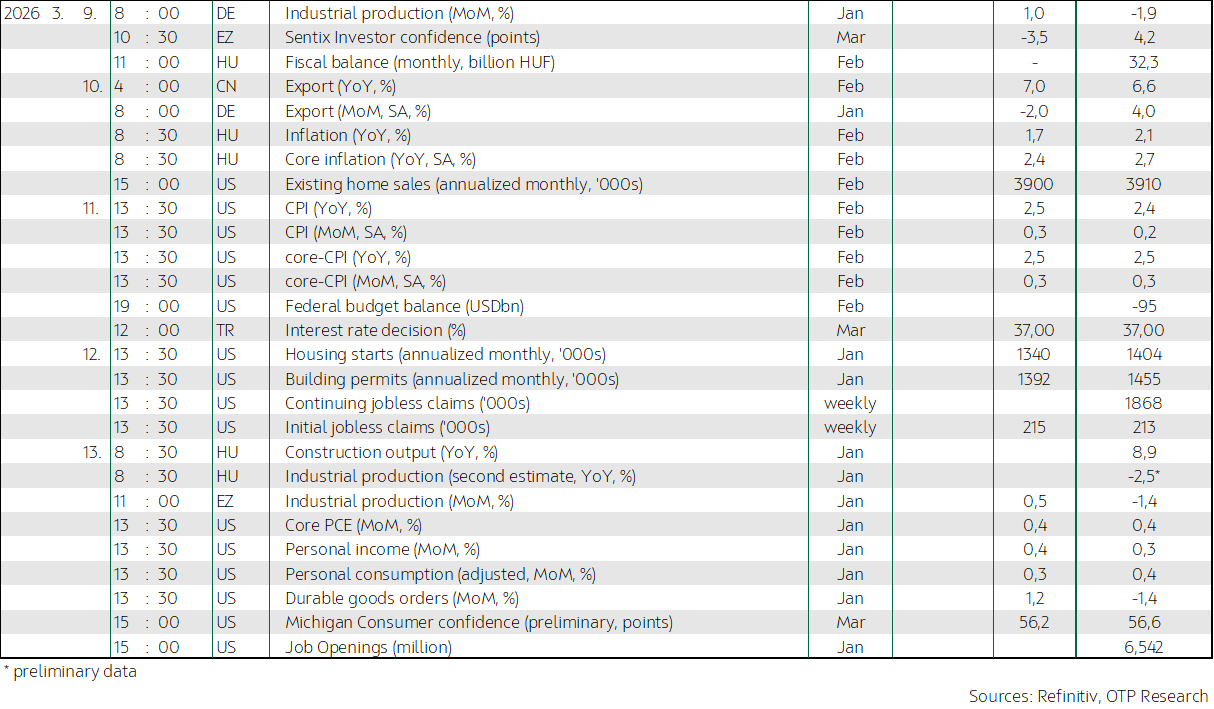

Today, Germany’s industrial production data and the eurozone’s Sentix sentiment index are due. Hungary publishes February inflation data on Tuesday; the market expects inflation to have fallen to 1.7% in February, and our in-house forecast is 1.8%, down from 2.1% in January. The main driving force of disinflation in February may have been food prices, but to a lesser extent, alcohol and tobacco products, as well as administered prices, may have also contributed to the tamed inflation. The USA releases inflation data on Wednesday; the median market expectation for headline and core inflation rates is +0.3% month-on-month. However, the inclement weather and the uptick in oil and service prices in February may cause a negative surprise.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more