OTP Morning Brief: Europe’s stock markets hit record highs again

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

In Europe's leading economies inflation was lower than expected. US markets saw optimistic trading on Tuesday, Nvidia CEO's speech affected several industries. Yields fell in Europe. The EUR/HUF is drawing near 385 again. Asia’s markets traded mixed today. Investors await the eurozone’s inflation data today.

Europe’s stocks hit record highs, inflation in Europe's leading economies was lower than expected

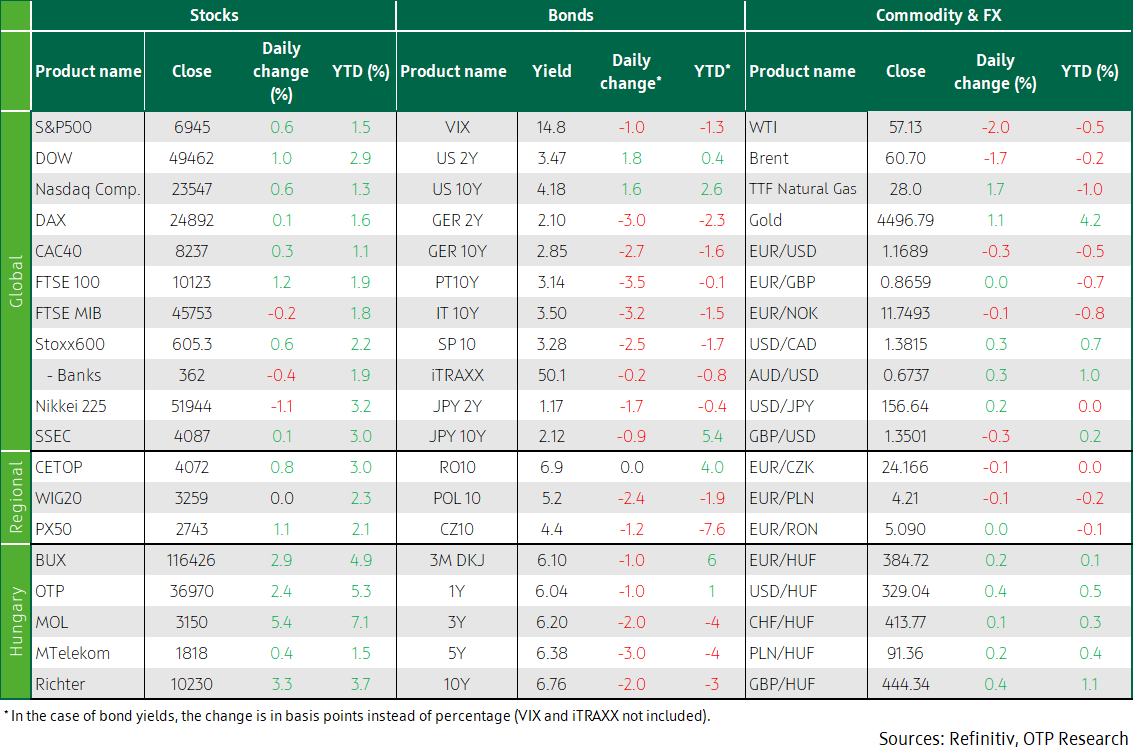

In Europe, stock markets closed on a strong note on Tuesday, with benchmark indices in Germany, the UK, and Spain hitting record highs. Seeing the upbeat economic data, investors ignored rising international tensions, but the European market also benefited from Goldman Sachs’ raising its twelve-month price target for the STOXX 600, which helped the index close 0.6% higher, at a new record. The healthcare index (+3%) was particularly strong, supported by a 5% rise in Novo Nordisk as the Danish drugmaker launched its Wegovy tablet in the USA on Monday. AstraZeneca and Novartis surged 4.9% and 2.8% respectively. InPost skyrocketed almost 30% after the parcel machine operator said it had received an offer to potentially buy all of its shares. Adidas shrank 3.6% as Bank of America downgraded the sportswear maker.

In the eurozone’s two largest economies, December’s inflation data came in better than expected: in Germany, prices increased by 2.0% YoY in December (versus expectations for 2.2%), down from 2.6% in November, while in France the annual CPI rate was 0.7%, whereas analysts had expected it to remain at the previous month’s level, 0.8%. The latest data suggest that inflation for the entire euro area is likely to be 1.8-1.9% instead of the previously expected 2.0%, thus it may fall below the ECB’s target range. The final HCOB composite purchasing managers’ index (PMI) for the eurozone slowed to 51.5 in December from a 30-month high of 52.8 in November, missing the preliminary estimate of 51.9. Yet the index has remained well above the 50-point mark in every month of 2025, for the first time since 2019.

The sentiment in the CEE region was clearly benign: Czechia’s PX50 gained 1.1%, and Hungary’s BUX soared 2.9%, while the Polish stock market was closed on Epiphany holiday. Of Hungary’s blue chips, MOL skyrocketed 5.4%, Richter shot up 3.3%, and OTP grew by 2.4%. Rába shares also rose sharply (+20.5%), after 4iG announced that the acquisition of a majority stake in the Hungarian automotive company had been completed.

US markets had buoyant trading on Tuesday, Nvidia CEO's speech affected several industries

In Tuesday's benign trading sentiment in the USA, the NASDAQ and S&P500 advanced 0.6% each, and the Dow increased by 1%, to a record high. This was also fuelled by the 3.4% gain of Amazon, which was the second-largest stock traded in the Dow index, after Nvidia (-0.5%). Nvidia CEO Jensen Huang spoke at the Consumer Electronics Show in Las Vegas about new-generation AI processors, which offer a new layer of data storage technology. As a result, shares of several memory and storage companies also excelled: SanDisk (+27%), Western Digital (+17%), Seagate Technology (+14%), and Micron Technology (+10%) each hit all-time highs. Nvidia's CEO also said that the company was about to embark on the development of driverless vehicles with a new series of open-source tools and models, which caused Tesla shares to slump 4.1%, as its competitive advantage in the field of self-driving cars was threatened. Most oil stocks reversed the previous day's strong gains: Exxon Mobil (-3.4%) and Chevron (-4.5%) both slid. According to data released on Tuesday, the final reading of the S&P Global composite PMI slipped to 52.7 in December, from 53.0 in the previous month, while the services PMI decreased to 52.5 points, from 52.9.

Oil prices fell on Tuesday as the market weighed potentially ample global supply this year in the context of uncertainty over Venezuela’s crude output after the USA captured the South American country’s leader, Nicolás Maduro, and announced that US companies would resume production in the country. Brent crude futures slipped 1.7%, to 60.70 USD/barrel, while WTI sank 2%, to 57.13 USD/barrel.

Yields sank in Europe, the EUR/HUF nears 385 again

Bond yields in Europe shed a few basis points after preliminary data showed that December’s inflation in France and Germany fell sharply stronger than thought, and the euro area’s confidence indices have weakened. Germany’s 10Y yield shed three basis points, to below 2.85%. In the USA, despite the weakening confidence indices, bond yields inched up; the 10Y one returned to near-4.2% levels. The dollar regained 0.3% from the euro, thus the EUR/USD dropped below 1.17.

While the zloty (PLN) and the Czech koruna (CZK) slightly appreciated versus the euro yesterday, the forint weakened by 0.2%, partly owing to the unexpectedly weak foreign trade data for November, as Hungary’s trade balance turned negative. The EUR/HUF is approaching the 385 mark once again. The slow decline in bond yields continued yesterday: benchmark yields eased by 2-3 basis points for most maturities; the 10Y benchmark yield was at 6.76%. Thanks to the healthy demand, the ÁKK sold HUF 40 billion worth of three-month discount Treasury Bills (more than the HUF 30 billion it had initially offered), at an average yield of 6.14%.

Today’s highlights

Asia’s stocks traded mixed today: Japan’s Nikkei lost 1.1% as China banned exports of dual-use goods (which can also be used for military purposes) to Japan. This is Beijing's latest move in response to Japanese Prime Minister Takaichi Sanae's statement on Taiwan. China's SSEC edged lower, while the Hang Seng came down 1.2%. However, South Korea's Kospi rose to a record high, driven by AI optimism.

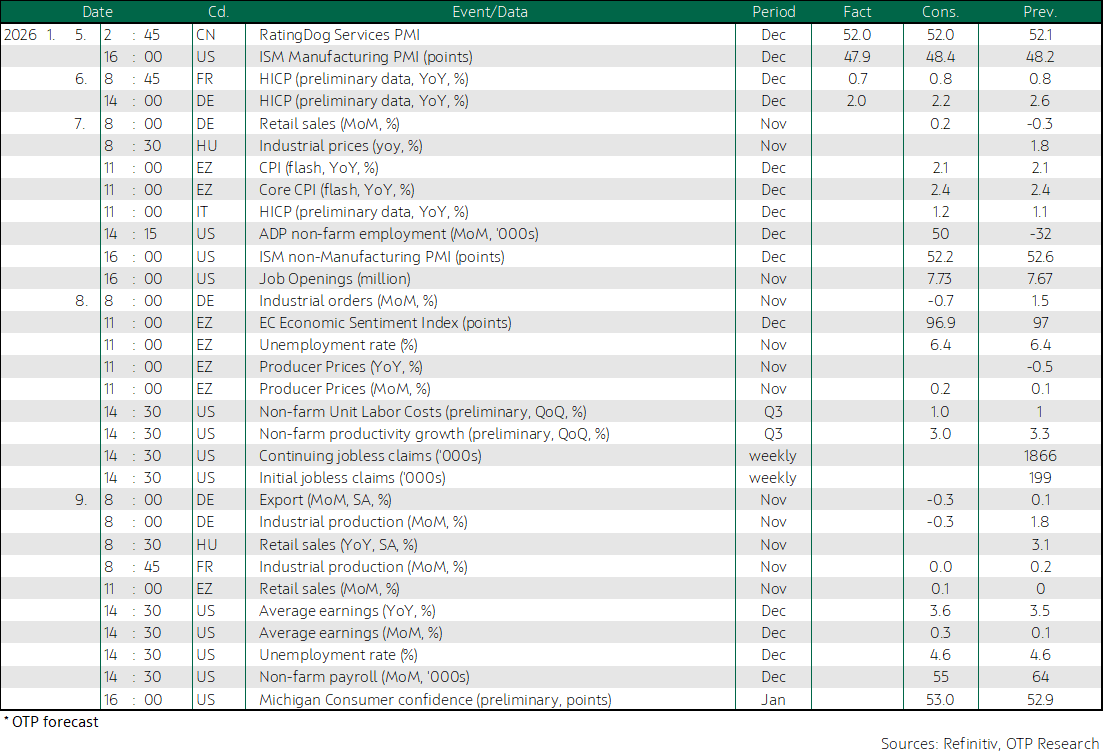

Today, the main focus will be on eurozone inflation data for December, which may help predict the ECB's interest rate path. Germany releases retail sales data and Hungary publishes industrial producer prices. On the other side of the Atlantic, the ADP employment survey for December and the ISM non-manufacturing purchasing managers' index are due out.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more