OTP Morning Brief: growing concerns over a protracted conflict in the Middle East

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Investors are increasingly concerned about a protracted standoff, which is hurting growth expectations and redrawing the previously expected interest rate path. Crude oil prices rose further. Benchmark stock markets fell on both sides of the Atlantic. The BUX and Hungary’s blue chips rose. Interest rate cut expectations eased in the USA, while in Europe the likelihood that the ECB might even be forced to raise interest rates this year has increased. Developed economies’ bond yields continued to rise. The dollar has strengthened against the euro. OTP Group has published its 2025 earnings report. Today, beyond the Middle East conflict, the focus will be on the US labour market report for February.

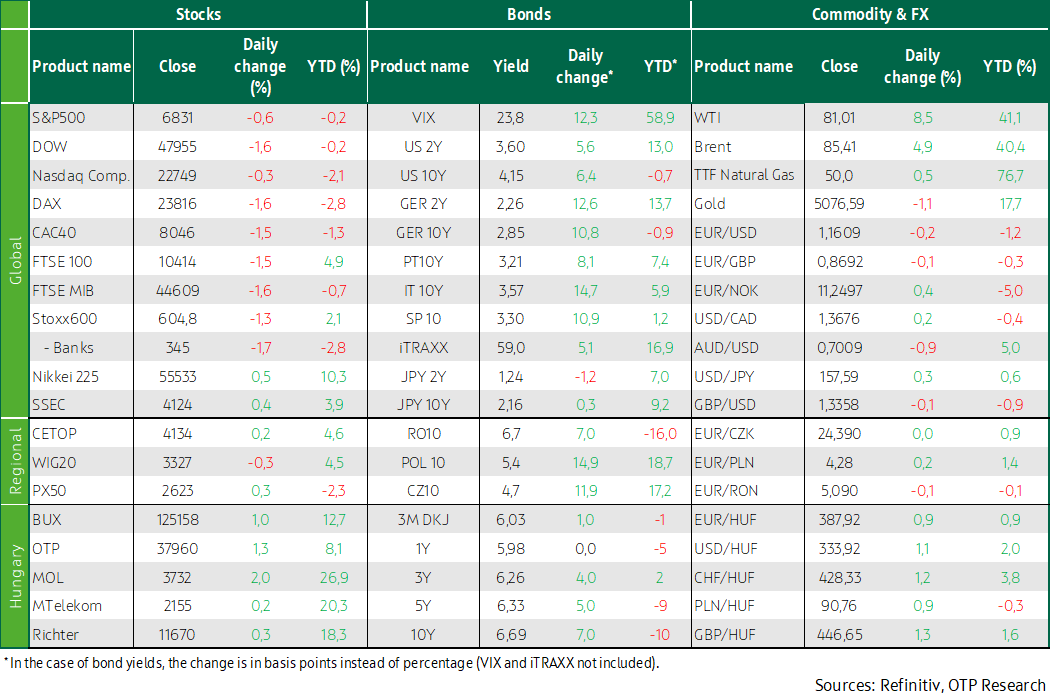

Concerns over a protracted conflict in the Middle East are growing; crude oil prices have risen further

A growing number of countries across the Middle East are becoming directly involved in the conflict that erupted last Saturday when the USA and Israel attacked Iran. Investors are increasingly concerned about a protracted confrontation, weighing the negative impact on growth and interest rates. In addition to the geographical spread of the fighting, the risks are also increased by the threat to shipping in the vital Strait of Hormuz, where missile and drone attacks have dramatically reduced tanker traffic. Yesterday, the price of WTI oil jumped by another 8.5%, to 81 USD/barrel, and Brent grew by 4.9%, to USD 85.4, bringing the weekly gains to 20% and 18%, respectively. The natural gas market is also under constant tension after a drone attack in Qatar, which accounts for 20% of the world's LNG production, caused state-owned QatarEnergy to suspend its liquefied natural gas (LNG) production and declare force majeure, thus releasing itself from its contractual obligations. After the sharp rise at the beginning of the week, the European natural gas market seemed to calm somewhat on Wednesday, and the TTF quotation did not move significantly from 50 EUR/MWh yesterday. However, the weekly increase still exceeds 50%. Meanwhile, the US domestic (Henry Hub) natural gas price remained low. US interest rate cut expectations have eased: the market is pricing in only one 25-basis-point cut this year instead of the previous 50bps. However, the market is already considering the possibility of an interest rate hike by the European Central Bank this year. In the USA, a vote that would have forced the Trump administration to seek congressional approval before proceeding with military action against Iran failed in the Senate and the House of Representatives. Iran’s Foreign Minister Abbas Araghchi said on Thursday that Iran “is not asking for a ceasefire” from the United States and Israel, adding that “we don’t see any reason why we should negotiate.”

Western Europe’s key stock markets declined; Hungary’s BUX rose

In the shadow of increasing geopolitical tension, Europe’s major stock markets fell yesterday. The Stoxx600, which opened the day higher, fell by 1.3% at the close, with all sectors except media turning red; industrial, aerospace and defence stocks posted the biggest losses. Following Wednesday's rise, the Spain’s IBEX slipped 1.4% on Thursday as Madrid continued to refuse to allow US forces to use its bases to strike Iran, while the White House, which had previously threatened Spain with a complete break in trade relations, said on Wednesday evening that Spain agreed to cooperate. In the corporate world, the German tank manufacturer Renk reported a 19.8% YoY surge in revenue in the 2025 financial year, in line with the strengthening of the role of the defence sector in Europe. Yet this did not help it avoid the selling wave that hit the sector yesterday.

On the macro front, the eurozone's January retail sales data surprisingly edged 0.1% lower month-on-month, marking a weak start to the year. At the member state level, Germany declined notably, while France, Italy, and Spain recorded slight growth. By themselves, these data do not undermine this year’s growth expectations, but together with the conflict in the Middle East, they pose a growing downside risk.

The sentiment in the CEE region was less gloomy than in Western Europe: Hungary’s BUX (+1%) and Czechia’s PX (+0.3%) grew, while Poland’s WIG20 slipped 0.3%. All Hungarian blue chips closed higher. In Hungary, retail sales expanded by 3.0% YoY in January and 0.5% MoM (in seasonally adjusted terms), the KSH Statistical Office said.

Wall Street’s stock indices also turned red on Thursday

Wall Street also traded in a gloomy sentiment yesterday. The biggest losers were the industrials, raw materials, and healthcare sectors, and airlines nosedived. The losses were somewhat mitigated by Broadcom’s (+4.8%) optimistic forecast, it expects AI chip revenue to exceed USD 100 billion next year.

The data released yesterday showed that productivity growth was stronger in the first three quarters of last year than previously estimated, owing to large negative wage revisions for 2025. The growth rate was 2.8% year-on-year in the fourth quarter, and 2.2% in full year 2025. Hourly wages rose more than expected in the fourth quarter (+1.3% YoY) while unit labour costs rose by just 1.9% last year. Layoffs fell significantly in February, while initial jobless claims remained low, suggesting a stable labour market.

The VIX, also known as the fear index, which measures the volatility priced into S&P500 options, continued to rise yesterday, bringing this week’s gain to 20%.

Donald Trump said yesterday that he was firing Kristi Noem, the secretary of homeland security, and will replace her with Oklahoma Senator Markwayne Mullin, who will take office on 31 March.

Adding to America’s domestic political turmoil and uncertainty caused by the trade war, New York Attorney General Letitia James and 23 other state attorneys general have filed a new lawsuit challenging Donald Trump’s global tariffs, after the U.S. Court of International Trade ruled on Thursday that companies are entitled to refunds on tariffs that the Supreme Court had struck down. The Trump administration’s new temporary global tariff increase, from 10% to 15%, could take effect this week, Treasury Secretary Scott Bessent said.

Interest rate cut expectations eased; advanced markets’ yields rose; the USD strengthened

Owing to increasing expectations that the conflict in the Middle East will not end quickly, concerns have increased that an attack on Iran could raise energy prices and inflation in the longer run. In addition, favourable labour market data came from the United States. Due to the above, US interest rate cut expectations have weakened further: the chance that the Fed will cut interest rates by no more than 25 basis points this year has increased to above 50%, and the probability that there will be no easing at all has now reached 16%. Meanwhile, in Europe, the likelihood that the ECB may be forced to raise interest rates this year has increased – owing to soaring energy prices, and because all major components of the February eurozone inflation data published on Tuesday (including headline, core and services inflation) were higher than expected. As a result, advanced economies’ yields continued to rise; the 10-year US yield increased by 4 basis points to around 4.15%, the German yield by 10 basis points to 2.85%, and Italy’s and France’s 10Y yields by almost 15 basis points. In this environment, it is no wonder that the dollar strengthened against the euro by another 0.25% to around 1.16.

The CEE region’s currencies weakened against the euro, the Czech koruna lost 0.1%, the zloty 0.25%, and the forint depreciated by 1%, sending the EUR/HUF above 388.5. Hungary’s bond yields rose by 4-7 basis points until the benchmark fixing in the early afternoon, and then by another 5-10 basis points until the evening; the 10Y closed near 6.75%. At yesterday's auction of 3Y, 5Y, and 10Y bonds the ÁKK sold the amount on offer, HUF 20 billion, despite the subdued demand; the average yield was a few basis points above Wednesday's reference yields (6.24% and 6.3%, respectively). However, there was strong demand for the 10Y bond: bids were nearing HUF 140 billion, and the agency sold HUF 40 billion worth of bonds in the competitive phase, and HUF 4 billion in the non-competitive one, at an average yield of 6.67%.

OTP Group Full-Year 2025 Results:

The OTP Groupachieved outstanding performance in 2025: its profit after tax amounted to HUF 1,146 billion, corresponding to a full-year ROE of 21.6%. Foreign subsidiaries contributed 71% of the after-tax profit.

Consolidated net interest income improved by 9% y-o-y, driven mainly by the expansion of business volumes, while the net interest margin also increased by 7 bps y-o-y to 4.34%. The risk profile remained favourable: the ratio of Stage 3 loans was broadly unchanged q-o-q at 3.5%.

FX-adjusted performing (Stage 1+2) loan volumes grew by 5% in the fourth quarter, bringing full-year growth to 15%. Retail portfolios remained the main growth driver: mortgage loans rose by 19% y-o-y and consumer loans by 18%. The government-supported “Home Start” mortgage scheme, launched in September, generated an 11% q-o-q increase in mortgage volumes in Hungary in the fourth quarter. Consolidated corporate (including MSE) loan volumes rose by 5% q-o-q and 11% for the full year. With the exception of Slovenia and Croatia, all Group members recorded loan growth exceeding 10% y-o-y. Consolidated deposits grew by 11% y-o-y on an FX-adjusted basis, with Hungarian retail deposits up 10% over the past 12 months. The OTP Group’s net loan-to-deposit ratio stood at 77% at the end of 4Q 2025.

The stock of issued securities decreased by 3% y-o-y. In addition to several successful issuances, nearly EUR 1.8 billion of securities were redeemed during the year.

The OTP Group’s IFRS consolidated CET1 ratio declined by 0.3 pps q-o-q and stood at 18.1% at the end of December, matching the Tier 1 ratio. The Bank safely meets the MREL requirement applicable to the OTP resolution group: compared with the 24.1% minimum requirement effective at the end of 4Q 2025, the ratio stood at 25.3% at the end of December.

For 2025, management successfully achieved all major targets.

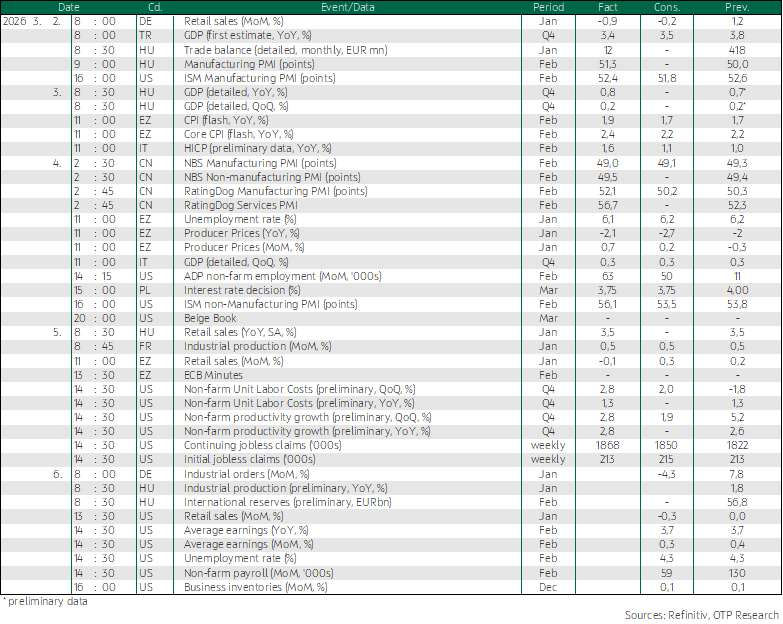

Today’s highlights

The Asia-Pacific region’s major stock markets moved mixed this morning. Crude oil prices eased slightly this morning. A defence giant, LIG Nex1 shot up more than 6% after South Korean media reported that its air defence systems were successfully used to intercept Iranian missiles launched towards the United Arab Emirates.

Index futures point to mixed opening in Europe and America today.

The focus today will be on the US labour market report for February. January data turned out to be much stronger than expected: nonfarm payrolls increased by 130,000, while the previous month's data was revised downward; the unemployment rate fell to 4.3%, and wage dynamics strengthened. The market's median expectation is for employment growth of around 60,000, an unemployment rate of 4.3%, and a slightly slower month-on-month wage growth in February than in January, which would mean stagnation for the year-on-year data. Data in line with expectations would not fundamentally change the picture that the US labour market seems to be stabilizing after the rapid decline.

The development of the Middle East conflict will certainly continue to play a major role in shaping market sentiment today.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more