OTP Morning Brief: Alphabet’s report beats expectations

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

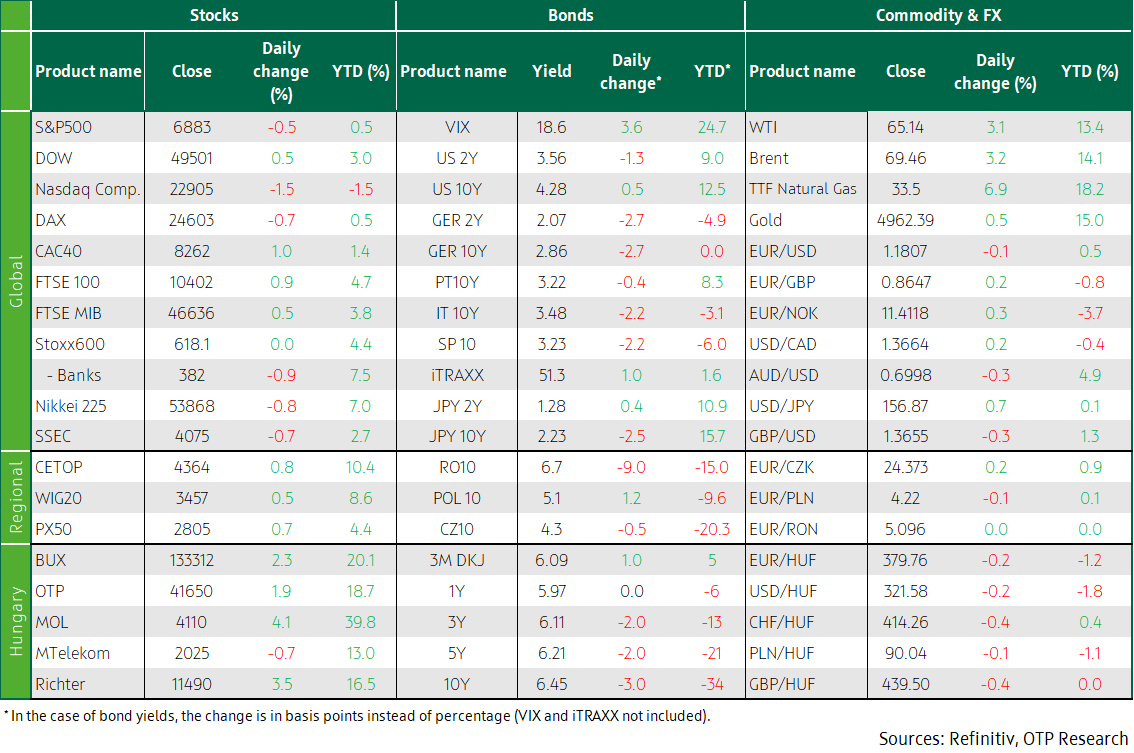

Europe’s stock markets closed mixed yesterday. In December EZ inflation slowed as expected but core CPI was lower than thought. The National Bank of Poland left its base rate on hold. The USA’s major indices closed mixed; AMD dived after its earnings report; Alphabet's figures surpassed expectations. US services sector PMI for January was flat; private sector employment grew slower than hoped, ADP survey shows. Developed markets’ bond yields dropped. The forint strengthened against the euro; Hungary’s bond yields sank. Today industrial and retail sales data will be published in Europe, and the ECB, the BoE and Czechia’s national bank make policy decisions. The USA releases weekly jobless claims figures.

Europe’s stock markets closed mixed on Wednesday; in December EZ inflation slowed as expected but core CPI was lower than thought; the National Bank of Poland left its base rate on hold

Europe’s stock markets closed mixed on Wednesday, the Stoxx 600 index practically stagnated. The sentiment was influenced by corporate earnings reports: shares in Santander plunged 3.5% after announcing the acquisition of Webster Bank for USD 12.2 billion, but the bank reported a fourth-quarter profit of EUR 3.76 billion, beating the consensus forecast of EUR 3.41 billion, and it announced a new EUR 5 billion share buyback programme. Novo Nordisk's share price nose-dived (-18%) at one point on Wednesday as the pharmaceutical company reported a weaker-than-expected sales and profit outlook for this year due to US price pressure and the loss of exclusivity for its key products, but later it pared losses. Shares in UBS slid 6.3%, even though the bank’s fourth-quarter profit of USD 1.2 billion exceeded analysts’ expectations of USD 919 million by a large margin.

In the euro area, January inflation slowed to 1.7%, its lowest level since September 2024, from 2.0% the previous month, in line with market expectations. The details pain a mixed picture: services inflation eased to 3.2%, while the drop in energy prices accelerated (to -4.1%, from -1.9% in December). In contrast, price increases in unprocessed food (4.4%) and non-energy industrial goods (0.4%) speeded up, while processed food, alcohol and tobacco inflation remained at 2.1%. Core inflation declined to 2.2%, slightly below expectations of 2.3%, and to the lowest level since October 2021. At country level, HICP (the harmonised index of consumer prices) slowed in France, Spain, and Italy, while it rose slightly in Germany. Meanwhile, industrial producer prices dropped by 0.3% month-on-month in December 2025, in line with forecasts, mainly driven by lower energy prices (-1.2%) and consumer durables prices; in y-o-y terms, prices declined by 2.1%, for the fourth consecutive month

The indices of the CEE region rose on Wednesday. Hungary’s BUX outperformed, as three of its blue chips grew, only MTelekom decreased. The National Bank of Poland left its base rate at 4%, in line with market expectations, even though some analysts had expected a 25-basis-point reduction. The next inflation forecast, in March, will provide a basis for assessing whether the disinflation process is sustainable. Inflation eased to 2.4% in December, nearing the middle of the central bank's 1.5-3.5% target range.

Major US indices closed mixed; AMD plunged after its earnings report; Alphabet's figures surpassed expectations; US services sector PMI was flat in January; private sector employment grew slower than hoped, the ADP survey showed

America’s stock markets closed mixed yesterday: while the Dow rose, the tech-heavy Nasdaq fell for the second day in arow. A selling wave that hit the technology sector has darkened the big picture: AMD's stock slumped 17.3% due to its weaker-than-expected first-quarter guidance, which triggered a further decline in the semiconductor industry - Broadcom and Micron's shares also slipped, while several software companies, including Oracle and CrowdStrike, continued their ailing. On the other hand, the Dow benefited from impressive corporate results such as the better-than-expected quarterly figures of Amgen (+8.2%), and Honeywell's nearly 2% gain, which was also supported by sector rotation towards value stocks. Investors awaited Alphabet's report on Wednesday and Amazon's figures, due on Thursday. In its flash report published after the close, the former beat market expectations on the profit and revenue lines, and indicated 2026 plans to almost double the amount spent on investment last year.

The ISM service sector index for the USA remained at 53.8 points in January, matching the December value, and exceeding the market expectation of 53.5 points, indicating that the sector continues to show strong expansion. Based on the sub-indices, business activity strengthened (57.4), while new orders (53.1), employment (50.3) and supplier deliveries (54.2) slowed, and price pressures continued to rise (66.6). Meanwhile, in the labour market, the private sector created only 22,000 new jobs, even though it was expected to grow by 48,000 and could add 37,000 jobs in December. Despite the pale big picture, the healthcare sector stood out with an increase of 74,000, while professional and business services hiring fell by 57,000 and manufacturing jobs shrank by 8,000 in January; the latter lost jobs every month since March 2024.

Developed markets’ yields fell; the forint strengthened against the euro; Hungary’s yields also sank

In the eurozone, annual inflation cooled to 1.7%, as expected, while headline inflation unexpectedly declined to 2.2% on the back of slowing services inflation. As a result, bond yields edged a few basis points lower, with German, Italian and French 10Y bond yields sinking by 2-3 basis points; the German yield is close to 2.85%. In the USA, long-term yields tended to nudge higher, the ten-year one drew near 4.3%. A slight dollar strengthening pushed the EUR/USD towards 1.18.

In Hungary, the persistently benign sentiment allowed the EUR/HUF to drop below 380, and benchmark bond yields fell. Investors preferred buying long-dated securities, thus the 3Y-10Y segment of the yield curve sank by 2-3 basis points, and the longer end dropped by 5-10 basis points.

Today’s highlights

Asia’s stock markets were heading down today. South Korea's index fell sharply after chipmakers Samsung and SK Hynix decreased, echoing the trends in America. In Japan, Softbank shares plunged as one of its major investments, Arm, reported weaker-than-expected sales.

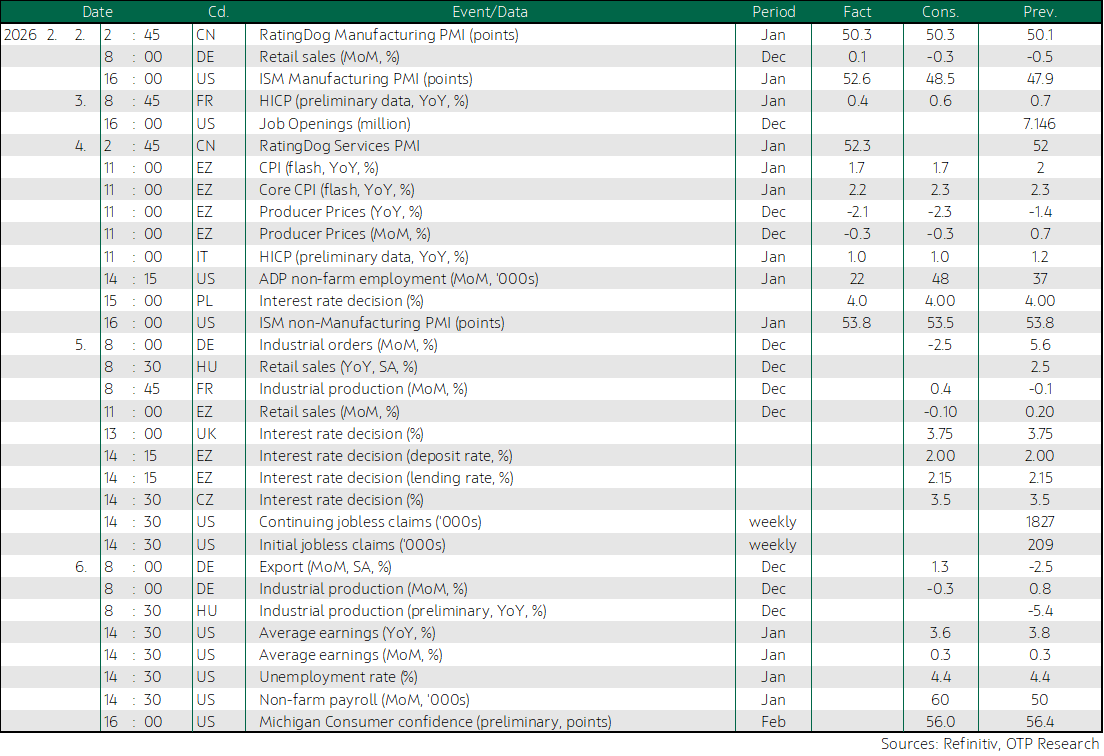

Today, Europe publishes industrial and retail sales data. The European Central Bank, the Bank of England, and the Czech National Bank hold interest-rate-setting meetings. The USA releases the weekly jobless claims data.

In Hungary, the ÁKK auctions 3Y, 5Y, and 10Y bonds, offering HUF 20bn, 25bn, and 25 bn, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more