OTP Morning Brief: commodity-linked shares offset the tech sector’s losses

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Europe’s markets moved sideways yesterday, when commodity-linked shares offset the tech sector’s losses. US stock markets fell on Tuesday. The government shutdown in the USA ended again. Oil prices rose amid Middle East tensions. The EUR/USD is once again above 1.18. Hungary’s long-term bond yields dropped. Services sector activity increased in China. The euro area’s inflation data and Alphabet's earnings will be in focus today.

Europe’s stock markets moved sideways, commodity-linked shares offset the tech sector’s drop

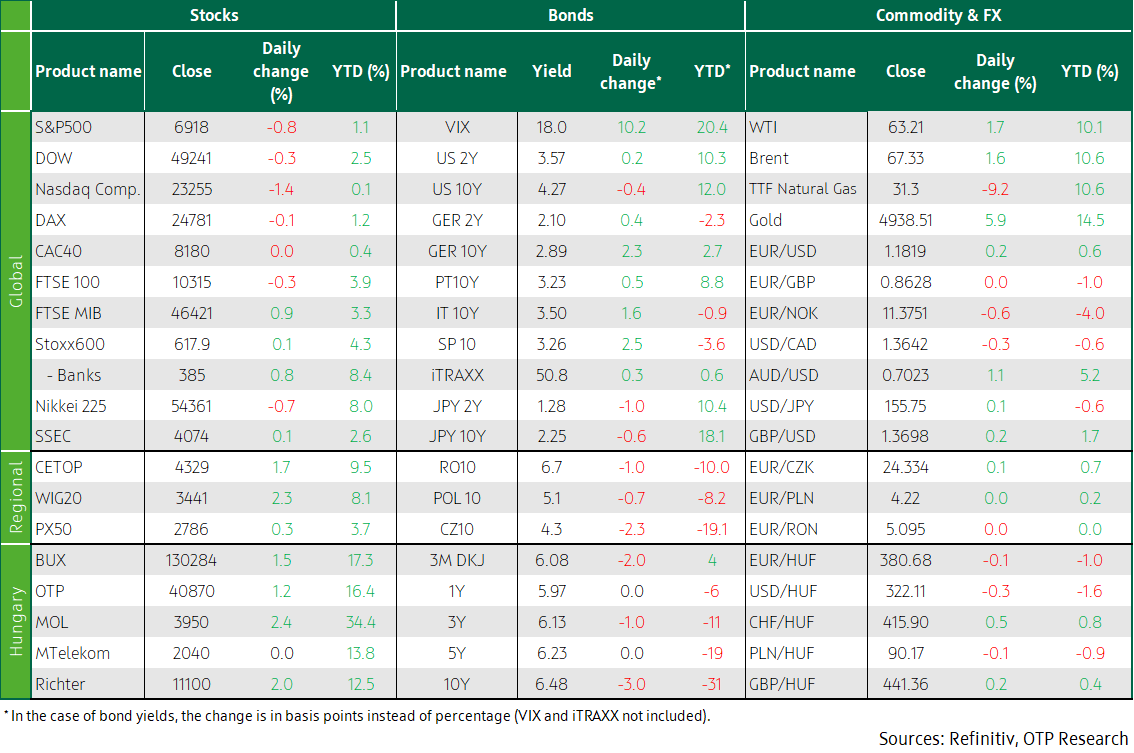

European markets made subtle movements on Tuesday, thus the Stoxx 600 index inched up 0.1%. Of the major indices, the UK's FTSE 100 (-0.3%), France’s CAC40 (-0.1%) edged lower, while Germany’s DAX closed flat – all of this was offset by the 0.9% increase in Italy’s FTSE MIB, which drew near a peak last seen in 2000. Of the various sectors, basic resources (+4.2%) excelled, benefiting form a rebound in precious metal prices: reversing Tuesday's decline, gold bounced back 5.2%, and silver grew by 5.3%. The media (-5.9%) and the tech (-4.2%) sectors had a less lucrative day; the latter was dragged down by stocks such as Infineon (-1.9%) and SAP (-4.6%). Europe’s largest asset manager, Amundi, gained 1.7% after reporting higher-than-expected net capital inflows in the fourth quarter. Novo Nordisk said it expects its profit and revenue to shrink by up to 13% this year due to US price pressure, strong competition, and the expiry of semaglutide patents. Accordingly, its shares listed in New York plunged 14.6%.

The sentiment was noticeably better in the CEE region, where the PX50 (+0.3%), the BUX (+1.5%), and the WIG20 (+2.3%) all posted gains. Hungary’s blue chips made nice gains, particularly MOL (+2.4%).

European natural gas futures continued Monday’s decline on Tuesday, sinking by 3.7%, to 34.2 EUR/MWh, indicating that concerns about LNG supply have eased.

America’s stock markets declined on Tuesday, the US government shutdown has ended, Middle East tensions drove oil prices higher

US indices slipped yesterday as investors worried about shrinking margins owing to overinvestment in AI and intensifying competition. Accordingly, the Nasdaq fell the most (-1.4%), followed by the S&P500 (-0.8%), and the Dow (-0.3%). AI giants Nvidia and Microsoft both fell 2.8%. Alphabet sagged ahead of its flash report today. Accordingly, the biggest loser in the S&P was technology (-2.4%). The exception within the sector was Palantir’s 6.9% rally, on the back of its positive earnings report. Soaring 3.4%, the materials sector outperformed in America too. In individual stocks, Walt Disney dropped slightly after appointing theme park chief Josh D’Amaro as the next CEO, thus ending uncertainty over succession. PayPal shares dived 20.3% as its 2026 profit forecast missed analysts’ estimates.

Donald Trump signed a budget deal that ended the partial government shutdown, restored funding for several agencies and gives lawmakers until 13 February to negotiate easing immigration restrictions; then, funding for the Department of Homeland Security (DHS) will be suspended again. The deal passed with broad, bipartisan support in Senate and narrowly in the House, as Democrats push for further restrictions on Donald Trump’s immigration policies in the wake of recent deadly incidents.

Brent crude oil futures rose by 1.6%, to 67.3 USD/barrel, while US WTI increased by 1.7%, to USD 63.21, as recent events have raised concerns that negotiations aimed at easing tensions between the United States and Iran could come to a halt. The US military said on Tuesday that it had shot down an Iranian drone that had "aggressively" approached the aircraft carrier Abraham Lincoln in the Arabian Sea. According to maritime sources and a security consulting firm, a group of Iranian motorboats also approached a US-flagged tanker in the Strait of Hormuz, north of Oman.

The EUR/USD went back above 1.18, Hungary’s long-term bond yields sank

Advanced economies’ bond markets opened with gains on Tuesday, even as France’s inflation data came in much lower than expected, but the trend reversed in the afternoon. European bond yields upped by 2-3 basis points; Germany’s 2.9% yield closed near the upper edge of its post-pandemic trading range. Yields on the US bonds edged lower by the end of the day; the 10Y one sank to 4.27%. The dollar’s weakening sent the EUR/USD above 1.18 once again.

The EUR/HUF did not budge, it hugged the 381 mark. In Hungary’s bond market, however, the rapid decline in yields on long-term maturities continued yesterday: the 10Y yield shed 3 basis points, below 6.5%, and the 20Y sank by nine basis points, to the vicinity of 7%. In yesterday’s auction, the ÁKK offered HUF 30 billion debt in three-month discount Treasury Bills, and despite the subdued demand, it could raise the allotted amount by a third.

Today’s highlights

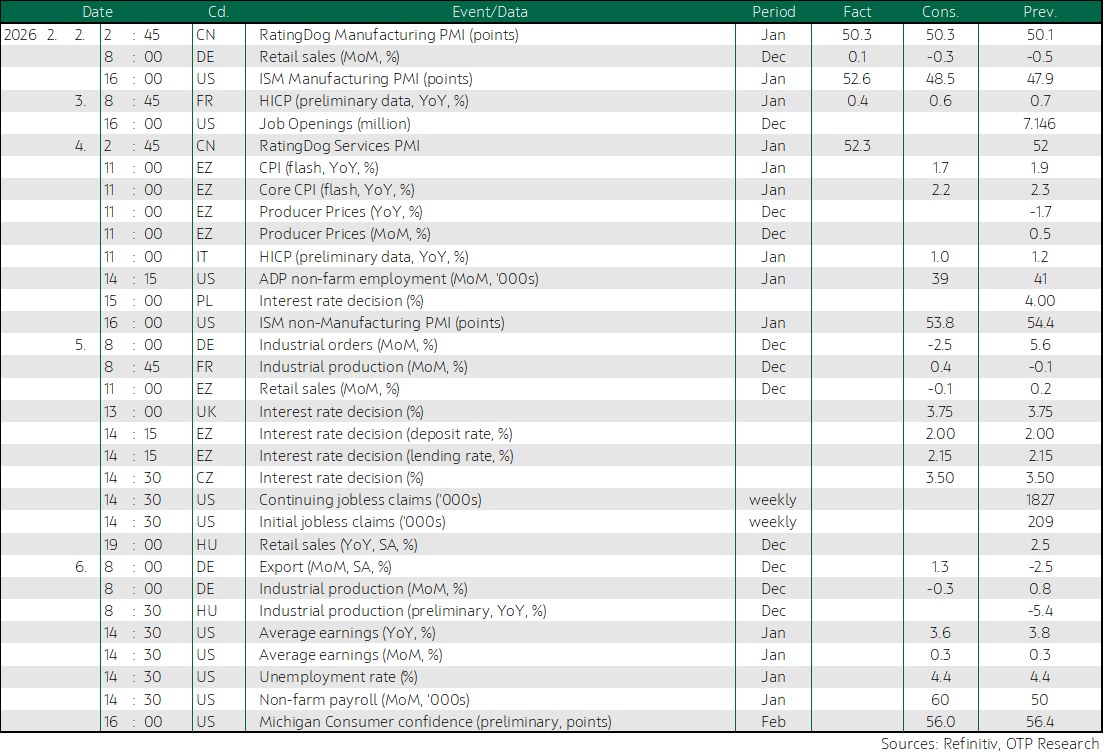

The RatingDog China General Services purchasing managers’ index rose to 52.3 points in January, from 52.0 points in the previous month. In January, activity in China’s service sector expanded at its fastest pace in three months, supported by stronger new orders, and employment also rose to its highest level since July. In sync with the manufacturing survey, these data may point to a slight improvement at the beginning of the year. China's SSEC stock index inched up 0.1% and Hong Kong's Hang Seng advanced 0.4%, while Japan's Nikkei lost 0.7%.

In Europe, the eurozone’s inflation data release and National Bank of Poland’s rate decision are in focus today. In America, ADP employment data and the ISM non-manufacturing PMI are scheduled for release. As the earnings season continues, investors await reports from Google's parent company Alphabet, as well as from Novo Nordisk's rival Eli Lilly.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more