OTP Morning Brief: Europe’s stock indices fell but their US peers pared losses

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The Middle East conflict shows signs of escalation. Iran has closed of the Strait of Hormuz. Europe’s stock indices turned red on the first trading day after the outbreak of war. Airlines, banking, insurance, and retail sectors fell in Europe, but energy rose. The Swiss National Bank intervened verbally, to counter the CHF’s strengthening. The price of TTF natural gas jumped 35%, oil prices grew by 6-8%. US indices worked off the morning's losses. In addition to energy, the defence and the tech sectors drove US markets higher. Intensified inflation fears pushed bond yields higher. The eurozone’s preliminary inflation data for February are due today. Hungary publishes the breakdown of Q4 GDP.

Europe’s stock markets fell in the aftermath of the Middle East war

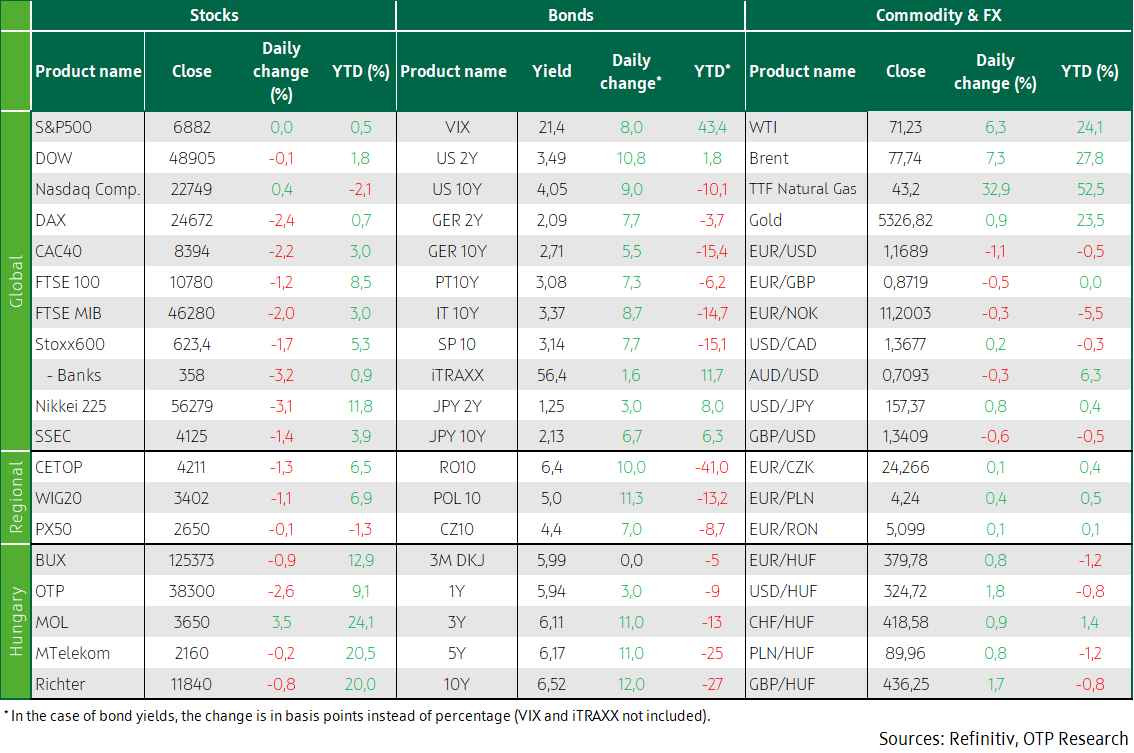

On Monday, the Middle East conflict showed signs of escalation in several respects: the Lebanon-based Hezbollah launched attacks on Israel; Israel and the USA are considering the possibility of ground action; Iran is unwilling to negotiate; the fighting is spreading to more than ten countries, and the Persian country has formally closed the Strait of Hormuz. On the first trading day after the outbreak of the war, Europe’s stock indices tumbled. The STOXX 600 (-1.7%), Germany’s DAX (-2.4%), France’s CAC40 (-2.2%), and the UK’s FTSE 100 (-1.2%) all closed in the red.

Airline shares nosedived on Monday as the escalating conflict between the USA, Israel, and Iran disrupted air travel worldwide and closed key airports in the Middle East, while oil prices soared. Lufthansa (-5.2%), British Airways' parent company (-5.4%), and Air France-KLM (-9.4%) all descended. Wizz Air (-7.6%) was hit particularly hard, owing to its presence in Israel. Banking shares also booked hefty losses. British lenders suffered from their exposure to the Middle East; HSBC, Barclays, and Standard Chartered all slumped 5%–6%. The broader banking sector index lost 3.3%, while insurance shares slid 1.7%. Consumer staples also weakened. Luxury brands such as LVMH and Kering fell more than 4%, while the broader retail sector shrank 3.5%. In contrast, energy stocks jumped as oil prices skyrocketed as much as 13% at one point on Monday. Shell, BP, and TotalEnergies surged 2%—4%, buoying the energy sector (+2%).

The Swiss National Bank said on Monday it was ready to step up its FX intervention in response to the Swiss franc’s strengthening owing to the Middle East conflict. Given the 0.1% year-on-year inflation rate in January, a too-strong CHF would pose a risk of deflation and could hurt the competitiveness of Swiss exporters. In the eurozone, the HCOB manufacturing PMI jumped to 50.8 in February, in line with preliminary data; this the best figure since June 2020 and the first reading above 50 (indicating growth) since August 2025.

The price of TTF natural gas in Europe jumped by 35%. While Gulf countries have some options for oil deliveries (using the East-West pipeline to the Red Sea), alternative transport routes for LNG are even less available.

Hungary’s BUX index slipped by 0.9% on Monday. While OTP fell by 2.6% (producing the largest turnover), rising energy prices sent MOL soaring (+3.5%). An important question in the CEE region will be how rising energy prices and their inflationary effects will affect monetary policy decisions. The National Bank of Poland, which concludes its interest rate decision meeting on Wednesday, was expected to trim interest rates by 25 basis points – before the Middle East conflict began. Czechia’s central bank will next decide on interest rates on 19 March, and Hungary’s MNB on 24 March.

US indices recovered from the morning’s losses

The S&P 500 closed just above zero on Monday, recovering from the losses made earlier in the day. The Dow Jones shed 0.15%, while the Nasdaq Composite gained 0.4%. Several factors helped the indices rebound from their declines: oil prices turned back from intraday highs, the energy sector fared well in the USA too, and among the technology giants, Nvidia (+2.9%) and Microsoft (+1.5%) share prices grew reassuringly. Not surprisingly, the defence industry did well. Northrop Grumman shot up 6% and Lockheed Martin advanced 3.3%.

The ISM Manufacturing PMI index was virtually flat at 52.4 in February, following a significant jump the previous month, suggesting that the US manufacturing sector is benefiting from the strengthening global investment cycle related to artificial intelligence. The most striking change was the 11.5-point jump in the Paid prices sub-index to 70.5, which could further heighten concerns about inflation risks.

Energy prices grew steeply on Monday, due to the conflict in the Middle East. WTI and Brent jumped by 6-8%. One of the most important direct causes of the energy price shock is that tanker shipments have practically stopped in the Strait of Hormuz, an exit from the Persian Gulf. The strait is important because about a quarter of global seaborne oil shipments and 20% of LNG shipments pass through it, a large share of which flows to Asia (mainly China). Shipping companies are waiting, especially because major shipping insurance companies have announced the suspension of war damage insurance for shipments in the region, but a significant increase in insurance premiums is more than likely. Iran’s attacks on the region’s oil infrastructure may also push up prices on the supply side. A drone has hit Saudi Arabia’s largest refinery Ras Tanura.

Rising inflation fears pushed bond yields higher

Energy prices have risen sharply as the attack on Iran is escalating, involving several countries, the Strait of Hormuz was closed, and there could be strikes on oil & gas fields in the Middle East. Oil prices jumped by roughly 10% in the morning but were still 7% higher at the close than the previous Friday, while the price of liquefied gas (LNG) skyrocketed 35%, heading for EUR 45/MWh. Global inflation fears have intensified, reversing the decline seen in developed countries' bond yields last week. The 10-year dollar yield jumped 10 basis points, to 4.05%, while the German one rose by 7 basis points, to above 2.7%. The dollar's rapid appreciation continued due to the strengthening of risk appetite; the EUR/USD fell below 1.17.

The CEE region’s currencies – the Czech koruna (-0.1%), the zloty (-0.4%), and the forint (-0.7%) – have weakened against the euro. The EUR/HUF drew near 380. Yields also rose by about 10 basis points on Hungary’s bond market; the 10Y yield returned above 6.5%. At Tuesday’s switch auctions, discount treasury bills worth nearly HUF 50 billion changed hands amid healthy demand.

Today, the ÁKK auctions 3M T-Bills, offering HUF 30 billion debt.

Today’s highlights

Heading into the close, Asia saw sharp falls today, particularly in Japan’s and Korea’s stock markets. The Nikkei slid 2.9%, the KOSPI plunged 5.5%, while the Hang Seng dropped 0.8%, and the SSEC declined by 0.6%.

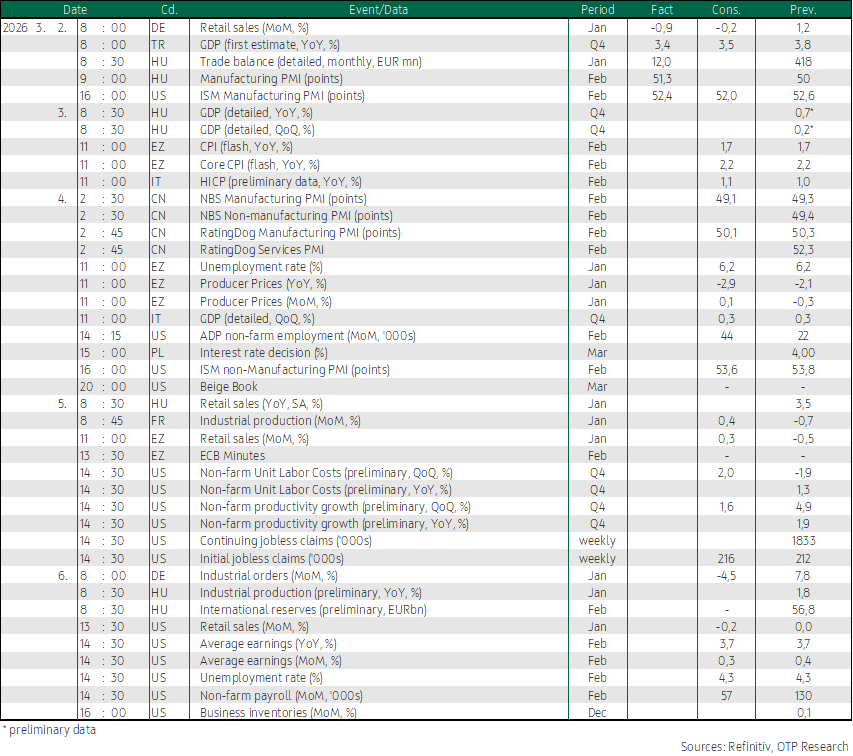

Today, the eurozone’s preliminary inflation data for February will be published. The market consensus expects stagnation, but some analysts anticipate increase, others decrease. Based on data released last week by major member states, we believe that the rate of inflation may have accelerated to 1.8-1.9%, from the 1.7% annual index in January. That would weaken the position of those expecting an interest rate cut. Elsewhere, Hungary publishes a breakdown of Q4 GDP data.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more