OTP Morning Brief: The US and Israel attacked Iran, oil and gas prices are soaring

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The USA and Israel attacked Iran over theweekend, aiming to topple the regime. This morning Israel launched new attackson Iranian targets, while Iran retaliated with strikes in neighbouringcountries, and closed the Strait of Hormuz. Crude oil prices jumped 8-10% today,while TTF natural gas prices surged 22%. Precious metal prices also increased, indexfutures point to opening in the red, and developed markets’ bond yields are likelyto decline. Advanced economies’ stock exchanges were risk-averse last week, amidAI concerns, the resurgence of the tariff war, and geopolitical fears; investorssought bonds instead. Developed markets’ long-term bond yields sank, US stockindices fell, while earnings reports offset the gloomy sentiment in Europe. However,on Friday, the collapse of the British Market Financial Solutions put banksunder significant pressure on both sides of the Atlantic. In Hungary, rate cutexpectations strengthened, yields sank, and the forint appreciated to a nearly-three-yearhigh. Today, investors will watch the events in the Middle East, Hungary’sforeign trade data, PMIs, and the US ISM index.

Corporate reports alleviated AI concerns and the collapse of a British mortgage lender; the Stoxx600 Europe and FTSE100 closed at record levels on Friday

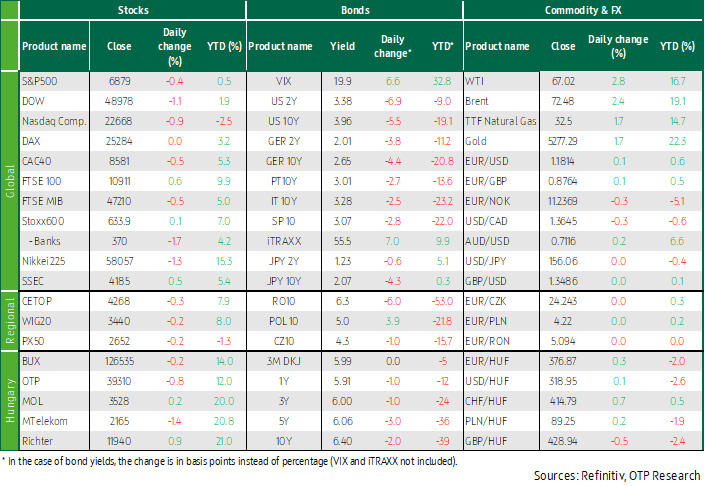

The Stoxx600 and FTSE100 closed at new highs on Friday; the European index ended its eighth consecutive month of gains for the first time since 2013. The Stoxx600 inched up 0.1% and rose by 0.5% last week. Reassuring corporate earnings reports fuelled Friday's upbeat stock market sentiment, while concerns about loans and artificial intelligence dragged down European banks. The Stoxx600 banking index fell 1.7% and Barclays lost more than 4% after reports that the bank would suffer significant losses owing to the collapse of British mortgage servicer Market Financial Solutions (MFS). Santander slumped nearly 3%, as its subsidiary Atlas SP Partners is among the lenders to MFS. Spain's IBEX benchmark index, which is dominated by local banks, lost 0.7%, thus it was one of the weakest performers on Friday. Elsewhere, France’s CAC40 shed 0.5% and the DAX edged a few points lower. Among the Stoxx600 sector indices, the travel & leisure sector suffered the biggest loss on Friday, followed by the banking index. Last week, the utilities, oil & gas, and real estate were the strongest sectors, while healthcare and consumer discretionary suffered the biggest declines.

Corporate earnings reports eased market concerns on Friday, when Nestlé upped 1.5% and Capgemini gained 2%. Quarterly reports caused wilder moves in some companies’ share prices: Melrose, the owner of GKN Aerospace, nose-dived nearly 12% after giving a weaker-than-expected revenue forecast for 2026, citing continued supply chain restrictions across the sector. British Airways owner IAG beat annual profit expectations, yet its shares descended 7%, along with the broader travel & leisure sector, the biggest loser in the Stoxx600, as crude oil prices surged more than 3% on Friday. Germany’s Delivery Hero retreated more than 4% as the online food delivery company’s gross sales slightly missed market expectations, reflecting strong competition and a challenging economic environment. Swiss Re jumped 4% higher after the reinsurance firm reported a stunning 47% growth in net profit and announced an additional USD 1 billion share buyback programme.

According to the latest LSEG survey, the aggregate profit of European listed companies may have contracted by 0.6% year-on-year in the previous quarter, whereas analysts had expected a 4% plunge.

The CEE region’s indices were slightly lagging behind on Friday: Hungary’s BUX, Czechia’s PX50, and Poland’s WIG20 all slipped by 0.2%. Among Hungarian blue chips, Richter rose by almost 1% thus closed at a historic high on Friday, when it published its quarterly report, while Mol advanced 0.3%.

The collapse of the British mortgage bank MFS also shook American banks; US indices closed Friday's trading and last week with significant losses

All major US stock indexes closed materially lower on Friday: the S&P500 (-0.4%), the Dow (-1%), the Nasdaq Composite (-0.9%), and the Russell2000 (-1.7%) all fell. This pushed their weekly and monthly performances into the red: the Nasdaq (-4%) and the S&P (-1.4%) both dropped in February. The sell-off in recent weeks has been driven by artificial intelligence-related costs and disruptions, the resurfacing angst over tariffs, and rising geopolitical tensions. Of the S&P’s sector indices, IT and financial sectors weighed on the index's performance on Friday. The financial sector's weakness was triggered by the collapse of the British mortgage lender Market Financial Solutions. Reportedly, Barclays, Jefferies, Wells Fargo, and other banks affiliated with it may face potential losses, while general concerns surround the management of lending conditions. Reportedly, the multiple use of loan collateral also played a role in the collapse of MFS. Wells Fargo, Jefferies, and Barclays slumped 4-9% on Friday. Investors preferred defensive sectors, thus healthcare, utilities, and non-cyclical consumer discretionary helped hold back the decline, while the rise in crude oil prices underpinned the strengthening of the energy sector. The released industrial producer price data came in higher than expected, reinforcing the market expectation that no interest rate cut seems likely in the short term. FRAs suggest that there is more than 90% chance that the Fed will not cut interest rates at its March meeting.

In individual names, Nvidia extended the previous day’s 5.5% loss by another 4% drop, despite solid quarterly results. Netflix jumped almost 14% higher on news that it had pulled out of the battle to buy Warner Bros Discovery, while Paramount, which is expected to buy the company, sky-rocketed 20%. Payment solutions company Block shot up 17% as it had announced the cutting of 4,000 jobs (nearly half of its workforce), owing to a shift toward using AI. Dell skyrocketed 22% after announcing that it expects revenue growth from its core AI-optimized server business in fiscal 2027, and owing to plans to return more cash dividend to shareholders.

Over the past week, technology was the weakest link, while utilities, telecommunications, and consumer discretionary sectors gained the most.

Crude oil prices rose further on Friday as talks between US and Iranian delegates did not bear fruit on Thursday. Although Iran was optimistic about the negotiations and their continuation, leaked information indicated that the US side was disappointed because there had been no progress on the nuclear deal. Crude oil prices climbed 2-3% on Friday, to an eight-month high. The weekly price increase was around 1%, despite escalating tensions. Precious metals prices more closely reflected the increasing risk-aversion: gold (+2%) and silver (6%) surged on Friday, bringing weekly price increases to 3% and 11%, respectively.

Rising tensions increased bonds’ appeal last week; the sentiment was positive in Hungary’s FI and FX markets

Last week, rising tensions over the Middle East, as well as US tariff policies, and the selling pressure on tech stocks drove investors towards advanced economies’ bonds. On Friday, US and European 10Y bond yields declined by 5-6 basis points; they sank 10-12 basis points last week, the 10Y US yield ended at 3.95%, and the German Bund yield near 2.65%, both marking four-month lows. The market is still pricing in two interest rate cuts this year and one more next year in the USA, but the timing of the interest rate cuts has changed: now the market is pricing in faster reductions. The market still does not expect the ECB to take any action this year. However, the incoming macroeconomic data did not really point to sinking yields. In the USA, the consumer confidence and the Chicago Purchasing Managers' Index both improved in February, all relevant indicators suggested that the producer price index unexpectedly rose, while the number of initial jobless claims remained relatively low. In the eurozone, Germany’s IFO index improved, while data from major member states pointed to a slight, stronger-than-expected increase in inflation.

The EUR/USD started last week above 1.18 and, although it closed most of the week below 1.18, the cross closed last week almost flat.

The sentiment in Hungary’s FX and bond markets was benign on Friday, fuelled by the fact that the MNB reduced the key interest rate by 25 basis points, to 6.25%, for the first time in almost a year and a half. The EUR/HUF dropped from 380 to 375 by mid-week and, although the forint closed the week nearly half a percent weaker, it is still at levels last seen in mid-2023. Interest rate cut expectations have strengthened in the bond market and yields have fallen. The market is pricing in three more 25-basis-point interest rate cuts by the end of this year, and at least one more next year. Last week, 3Y and 5Y yields sank by 5-10 bps, longer ones by 10-12 basis points; the 10Y benchmark yield declined to 6.4%.

Today’s highlights

Over the weekend, the USA and Israel attacked Iran with the aim of overthrowing the regime, and religious leader Ali Khomeini was killed in the attacks carried out in several waves. Iran also confirmed the information. Iran has vowed to retaliate; the Islamic Revolutionary Guard Corps bombed neighbouring countries, including Israel, Iraq, Jordan, the United Arab Emirates, Qatar, Kuwait and Bahrain, over the weekend. Israel has launched fresh airstrikes against Tehran, and on Monday expanded its military action to include attacks on Iran-backed Lebanese Hezbollah militants, as US President Donald Trump signalled that the US-Israeli military offensive against Iranian targets could continue for weeks. Iranian state media reported explosions in various parts of the Iranian capital, Tehran, on Monday morning, while Reuters sources reported loud explosions in Dubai and the Qatari capital, Doha. Kuwait said its air defences had shot down hostile drones, marking a third day of Iranian retaliatory strikes against neighbouring Gulf states. A suspected drone strike hit a British Royal Air Force base in Cyprus overnight, but there was no significant damage or casualties, Cypriot authorities and the UK Ministry of Defence said on Monday.

Iran closed the Strait of Hormuz over the weekend, and commodity markets were closed over the weekend, but this morning Brent and WTI quotes rebounded 9-10%. Crude oil prices jumped by 2-2.5%, to January 2025 levels. This morning, index futures pointed to a significant decline, and advanced economies’ bond yields were expected to fall. This morning, the price of TTF European-listed natural gas jumped by 22%, to 39 EUR/MWh, a one-month high.

The picture in Asia looked mixed in the last hour of trading. Benchmarks in Japan, Hong Kong, and South Korea came down 1-2%, while the Shanghai Composite was up 0.5%.

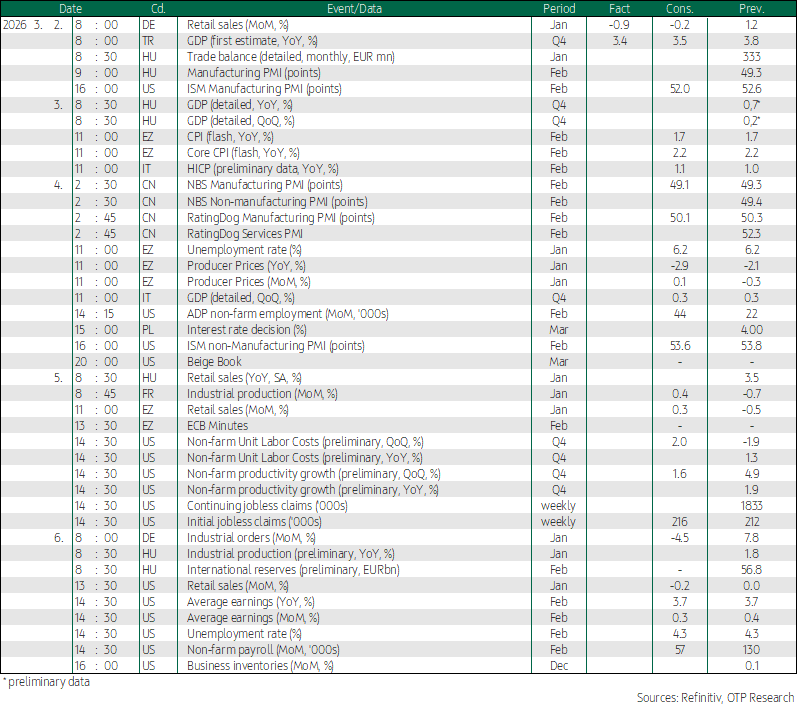

Germany’s retail sales shrank by a larger-than-expected 0.9% month-on-month in January, while December figures were sharply revised up. Turkey’s fourth-quarter GDP expanded by 3.4% year-on-year, slightly missing expectations, while the Q3 figure was revised up slightly.

Today the USA releases the ISM index. Hungary publishes detailed retail sales data, and manufacturing PMI. Later in the week, Hungary releases detailed GDP (on Tuesday), retail sales (Thursday), and preliminary industrial production statistics (on Friday).

On the international stage, the US labour market report (on Friday), as well as the February reading of the eurozone inflation data (on Tuesday) will be in the spotlight, as the inflation data from member states painted a mixed picture last Friday. The eurozone’s January retail sales data is due on Thursday.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more